2 Statutory Merger Structures and Key Synergies

How a Statutory Merger Turns Legal Combination into Operating Value

A statutory merger is easy to describe in one sentence.

Two companies combine into one legal entity, and one company survives while the other disappears.

In practice, a statutory merger is much more than a filing exercise.

It is one of the most demanding merger structure choices in M&A because the legal combination forces operational combination.

That is the point many early practitioners miss.

A statutory merger does not only transfer ownership.

It transfers assets, liabilities, contracts, employees, reporting lines, systems, and decision rights into one surviving company.

In the United States, the process typically starts with a merger agreement approved by the boards, followed by shareholder approval under applicable corporate law, and then formal filing with the relevant state authority so the merger becomes legally effective.

Once effective, the non surviving company’s assets and obligations pass to the surviving entity by operation of law. (Delaware Code)

This is why a statutory merger sits at the center of so many discussions about merger synergies.

If management wants to remove duplicate cost, unify go to market teams, consolidate procurement, or combine technology platforms under one command structure, a statutory merger can create the legal foundation to do that quickly.

That does not mean every statutory merger creates value.

It means this merger structure gives management a direct path to capture value if the operating model, governance model, and integration plan are designed properly.

A good way to understand a statutory merger is to think about two apartment buildings owned by separate landlords.

If one landlord simply buys shares in the other landlord, both buildings may still be run separately.

If the two property companies are combined into one legal entity, the owner can use one finance team, one maintenance contract, one insurance policy, one procurement process, and one tenant service model.

The legal combination makes operating consolidation much easier.

That is why sophisticated buyers do not ask only whether a statutory merger is legally feasible.

They ask whether the statutory merger supports the exact merger synergies they intend to capture.

If the answer is yes, the merger structure becomes part of the value creation plan rather than a technical afterthought.

How Statutory Mergers Work in Real Corporate Practice

A statutory merger follows a formal sequence.

Each step matters because the legal structure determines what can happen operationally after closing.

The legal sequence

- The boards negotiate and approve a merger agreement.

- The merger agreement identifies the surviving company and the share exchange terms.

- The companies seek the shareholder approvals required by the governing law and corporate documents.

- The parties file the merger documents with the relevant state authority.

- The merger becomes effective on filing or on the specified effective time.

- The surviving entity automatically succeeds to the dissolved company’s assets, liabilities, contracts, and obligations. (Delaware Code)

This looks procedural.

But the business implications are large.

Once the statutory merger becomes effective, the surviving company is no longer dealing with a partner across the table.

It is managing one combined enterprise.

That changes how integration teams work on finance, tax, treasury, HR, IT, procurement, sales coverage, compliance, and management reporting.

This is also why a statutory merger often creates pressure for earlier integration planning than looser deal structures do.

If legal combination is coming, the business cannot wait until after signing to decide how payroll will run, which ERP instance will survive, how purchase orders will be approved, or which legal entity will invoice customers.

For readers building practical M&A skill from the beginning, the best way to understand this logic is through a full process lens.

The Mergers and Acquisitions Online Course explains how merger structure connects to diligence, financing, negotiation, closing, and post close execution in one end to end framework.

Two Types of Merger Structures

A useful starting point is to separate the two core forms of merger structure.

This is where the comparison between absorption merger vs consolidation merger becomes commercially important.

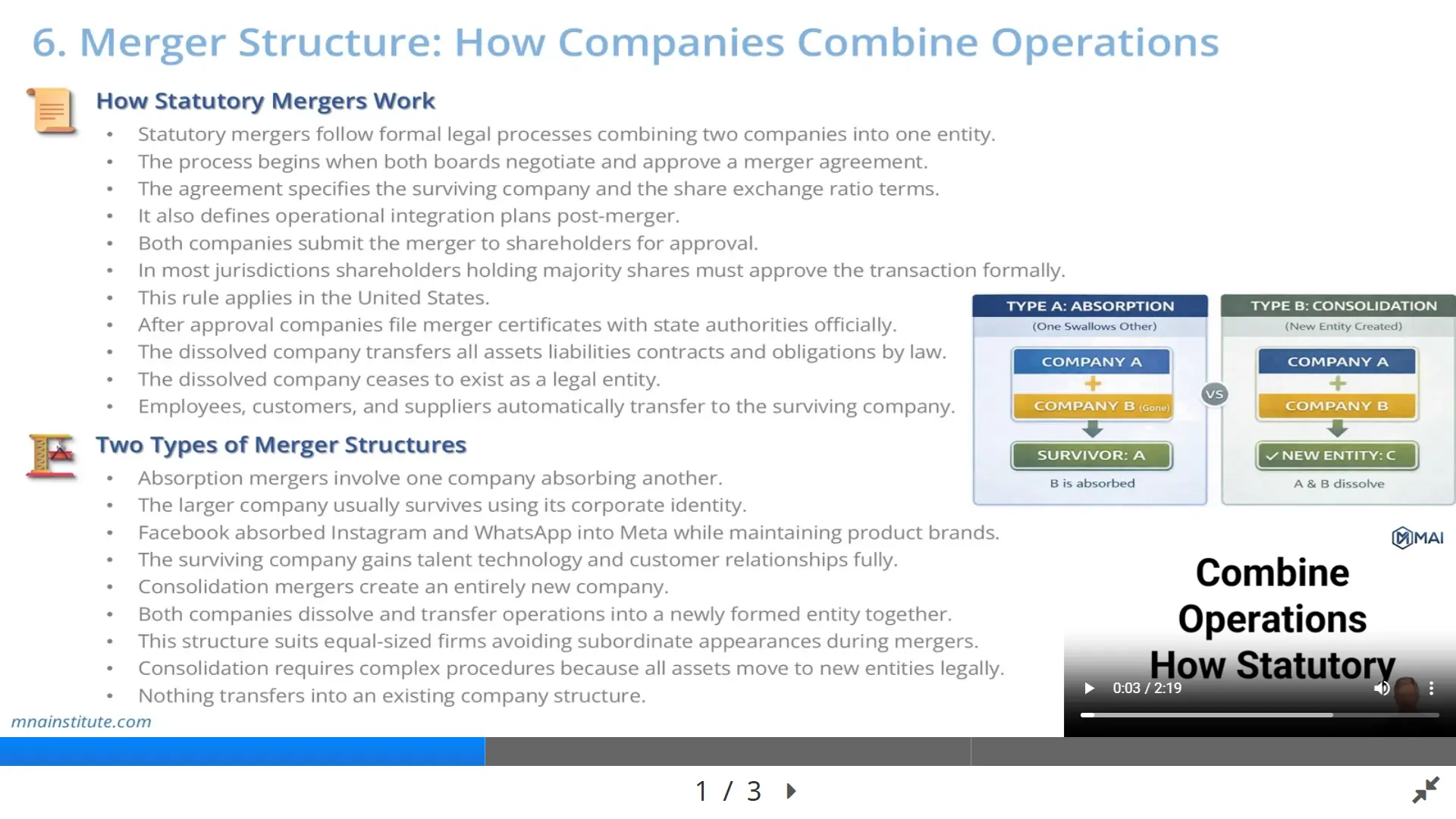

Absorption merger

An absorption merger occurs when one company absorbs another into its existing legal structure.

One company survives.

The other company dissolves.

This is the more common version of a statutory merger in practice.

It suits deals where one buyer is clearly larger, already has the stronger corporate platform, or wants to preserve one legal identity for financing, governance, tax, branding, or regulatory reasons.

The logic is simple.

If Company A already has the treasury systems, bank relationships, debt facilities, ERP platform, procurement contracts, and public market identity, Company A often becomes the surviving company.

Company B disappears as a separate legal entity, and its business is folded into Company A.

This version of merger structure usually supports faster cost capture because the surviving company can impose one reporting architecture, one set of policies, and one management hierarchy more quickly.

It is often the cleaner route if the main merger synergies are back office consolidation, procurement leverage, and corporate overhead reduction.

Consolidation merger

A consolidation merger dissolves both original companies and transfers both businesses into a newly formed legal entity.

Neither legacy company survives.

A new company becomes the resulting entity.

This version is less common because it is more administratively demanding.

A new corporate identity, new governance package, new documentation, and often a broader set of transition decisions are required.

Even so, consolidation can make sense in specific circumstances.

It fits situations where both companies are similar in scale, both brands matter politically, or neither side wants to appear subordinate.

It may also fit transactions designed as mergers of equals, even though true equality often proves difficult in practice.

Why absorption merger vs consolidation merger matters

The question is not which structure is theoretically elegant.

The question is which merger structure best supports the operating model after close.

If one platform is clearly stronger, an absorption merger often creates cleaner accountability.

If both sides need symbolic equality, consolidation may help secure support from boards, shareholders, regulators, or management teams.

For example, imagine two regional distributors.

One has a mature ERP system, stronger working capital controls, and better procurement discipline.

The other has better local customer coverage in a new geography.

If the economic case depends on rapidly consolidating finance, supply chain, and vendor management, an absorption merger will often be the better merger structure because it allows management to move both businesses onto the stronger platform faster.

Now imagine two firms of similar size combining to create a national champion in a regulated market.

If both boards insist that neither legacy company should dominate the optics of the transaction, a consolidation merger may be the more workable structure even if it adds complexity.

This is why absorption merger vs consolidation merger is not just a legal distinction.

It is a decision about speed, politics, culture, governance, and synergy design.

Why Companies Choose to Merge

Where Merger Synergies Actually Come From

Companies rarely pursue a statutory merger simply because the legal mechanics are neat.

They pursue it because they expect merger synergies.

Merger synergies exist when the combined company can produce better financial outcomes than the two companies could produce separately.

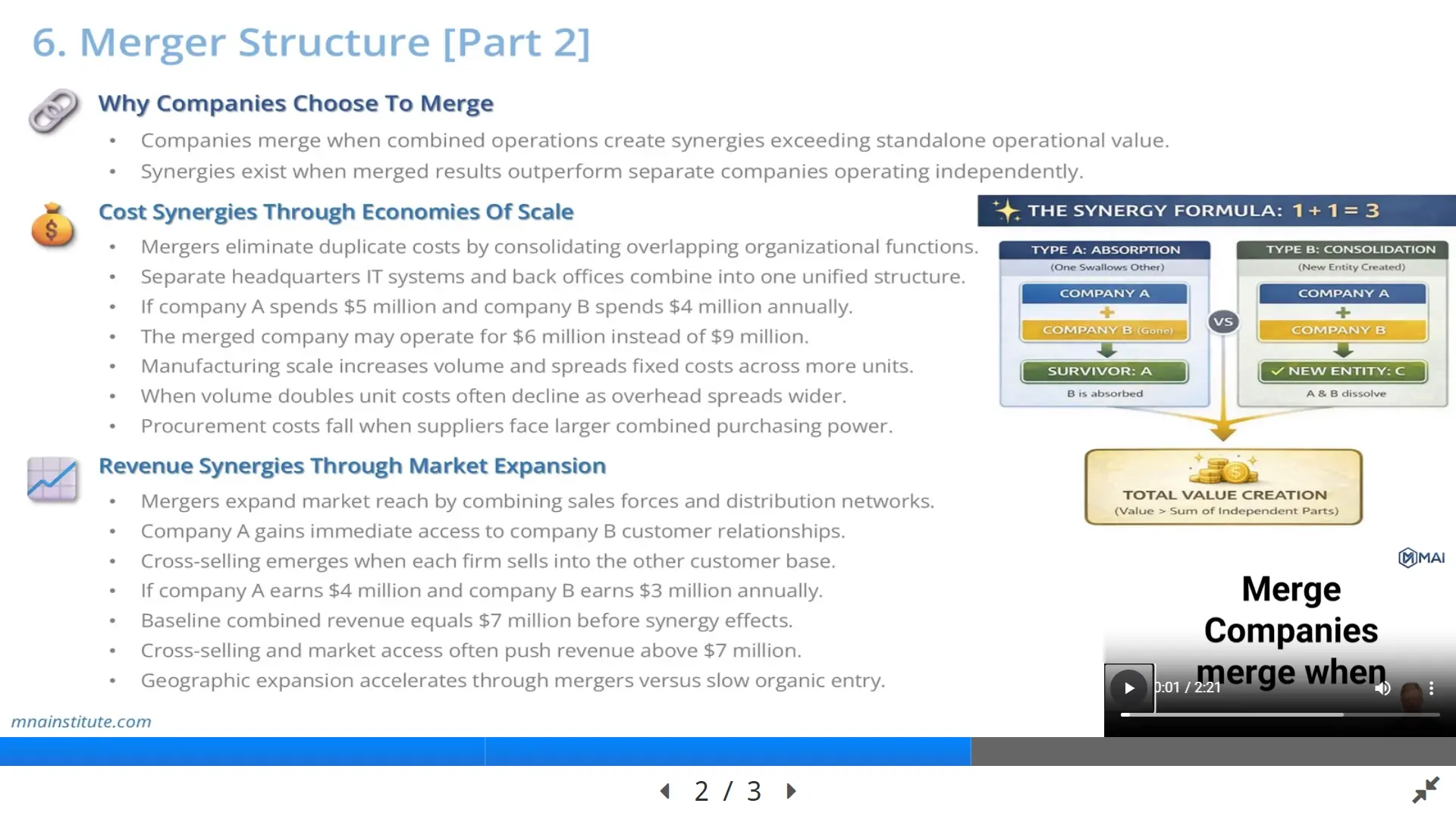

The classic shorthand is that one plus one becomes more than two.

In practice, management still has to show exactly where that extra value will come from.

The two categories that matter most in operating analysis are cost synergies and revenue synergies.

Cost synergies through economies of scale

Cost synergies and revenue synergies do not behave the same way.

Cost synergies are usually easier to identify, model, assign to owners, and track after close.

Consulting and finance training sources consistently note that cost synergies are more straightforward to quantify than revenue synergies.

A statutory merger supports cost synergies because one legal entity can remove duplication across the two legacy businesses.

Typical sources include:

- headquarters functions

- finance and accounting teams

- HR administration

- legal and compliance support

- procurement

- IT infrastructure

- manufacturing overhead

- logistics contracts

- external audit and advisory spend

- public company costs if one listing disappears

Consider a simple example.

Company A spends $5 million a year on corporate overhead.

Company B spends $4 million a year.

If the surviving company can run the combined group for $6 million, the statutory merger has created $3 million of annual run rate cost synergy.

That $3 million does not come from magic.

It comes from concrete operating actions.

- one chief financial officer instead of two

- one payroll platform instead of two

- one general counsel instead of two

- one enterprise software license set instead of two

- one headquarters lease or one reduced office footprint

- combined procurement volume with fewer vendors

This is where merger structure matters.

A statutory merger often makes these actions easier because the surviving company can standardize policies and systems under one legal chain of command.

Manufacturing businesses offer another clear example.

Suppose two factories each produce 100,000 units and each bears $2 million of fixed overhead.

If the merged company can shift production so that one optimized network produces 200,000 units with only $3 million of combined fixed overhead, per unit fixed cost falls materially.

That is a textbook cost synergy through scale.

Procurement synergy follows the same logic.

A combined business buying $50 million of raw materials negotiates differently from two separate businesses buying $30 million and $20 million.

The statutory merger creates one buyer with one contract structure and one spend baseline.

That helps management pursue lower prices, better payment terms, and better supplier service levels.

Revenue synergies through market expansion and cross selling

Revenue synergies are more attractive in presentations and harder in execution.

McKinsey and BCG both note that revenue synergies take longer to capture and are more difficult to estimate and deliver than cost synergies. (McKinsey & Company)

Even so, revenue synergies are often what make the strategic case compelling.

A statutory merger may create revenue upside in several ways.

- cross selling into the other company’s customer base

- geographic expansion through inherited sales coverage

- broader product bundles

- stronger channel access

- improved pricing power in some market structures

- better conversion because the combined company can deliver a fuller solution

Here is a simple example.

Company A sells compliance software to 500 corporate customers and earns $4 million of annual revenue.

Company B sells cybersecurity services to 300 corporate customers and earns $3 million.

If 100 of Company A’s customers also buy Company B’s services after the merger, and each adds $20,000 of spend, the combined business adds $2 million of revenue without building a new customer base from scratch.

This is how statutory merger and merger synergies connect.

The legal combination creates the platform.

The commercial integration creates the revenue.

But revenue synergy is not automatic.

Sales teams need new incentives.

Product teams need integrated packaging.

Pricing teams need new discount logic.

Customer success teams need new service scripts.

Management reporting needs a way to isolate which new revenue came from merger driven cross selling and which would have happened anyway.

That is why many executives overpromise revenue synergies in deal announcements and underdeliver later.

The source of value is real.

The difficulty of capture is real too.

Why companies still choose a statutory merger

If merger synergies are so difficult, why choose a statutory merger at all.

Because for many operating combinations, legal unity is the fastest path to managerial unity.

A statutory merger can accelerate:

- decision making

- capital allocation

- vendor rationalization

- customer contract management

- workforce redesign

- system standardization

- synergy accountability

In other words, the merger structure does not create value by itself.

It creates the conditions under which disciplined managers can create value.

Readers who want a practical framework for assessing synergy before the deal closes should study both diligence and post close planning together.

That is exactly why the Desktop Due Diligence & Quick Valuation course and the Post-Merger Intergration and Value-Up Strategy course are useful as a pair.

One helps you test whether the value case is real.

The other helps you convert the value case into execution.

Post-Merger Governance Structure

Why Governance Decides Whether Synergies Are Captured or Lost

Many merger models assume synergies appear because the spreadsheet says they should.

Real organizations do not work that way.

Synergies are captured through decisions, and decisions require governance.

In a statutory merger, the merger agreement typically outlines the governance structure of the combined company.

That structure often determines who sits on the board, who becomes chief executive, how the executive committee is formed, how budget authority works, and who signs off on integration milestones.

Board design

The board of the surviving company may expand to include directors from the dissolved company.

This can preserve institutional knowledge, maintain relationships with key stakeholders, and reduce the perception that one side has been erased too quickly.

The design choice is practical as well as political.

If the acquired business brings specialized regulatory, geographic, or technical knowledge, the surviving company benefits from keeping that expertise in the governance room.

Executive leadership

Most statutory mergers do not tolerate fuzzy hierarchy for long.

One chief executive has to lead.

One chief financial officer has to own the numbers.

One operations leader has to define the operating model.

This sounds obvious.

It often becomes contentious.

If the statutory merger is positioned as a partnership but the operating model requires one clear chain of command, confusion spreads quickly.

People wait for decisions.

Projects stall.

Customers feel the delay.

Synergies slip into the future.

The Day One problem

Integration planning should begin during diligence, not after celebration.

McKinsey’s work on merger integration repeatedly emphasizes the importance of early integration planning, disciplined synergy ownership, and clarity on the few choices that matter most at the outset. (McKinsey & Company)

The surviving company should know before legal close:

- which legal entities remain

- who approves spending

- which finance calendar applies

- who manages top customers

- which HR policies take effect first

- which ERP and CRM systems will survive in the first phase

- which synergy targets belong to which executives

Good governance does not make the merger feel slower.

It makes execution faster because it removes ambiguity.

This is why serious M&A teams link governance design to integration design.

If the business needs one procurement platform within six months, procurement leadership and systems decision rights must be defined before close.

If the thesis depends on cross selling, sales leadership, account ownership, and compensation mechanics cannot wait until quarter two.

For practitioners focused on the real execution side of M&A rather than only headline deal logic, the M&A Due Diligence: CDD, FDD, LDD, & HRDD course and the M&A Deal Negotiation Mastery course help explain how operating decisions are shaped long before the closing date.

Common Integration Failure Points

Why a Good Statutory Merger Still Fails

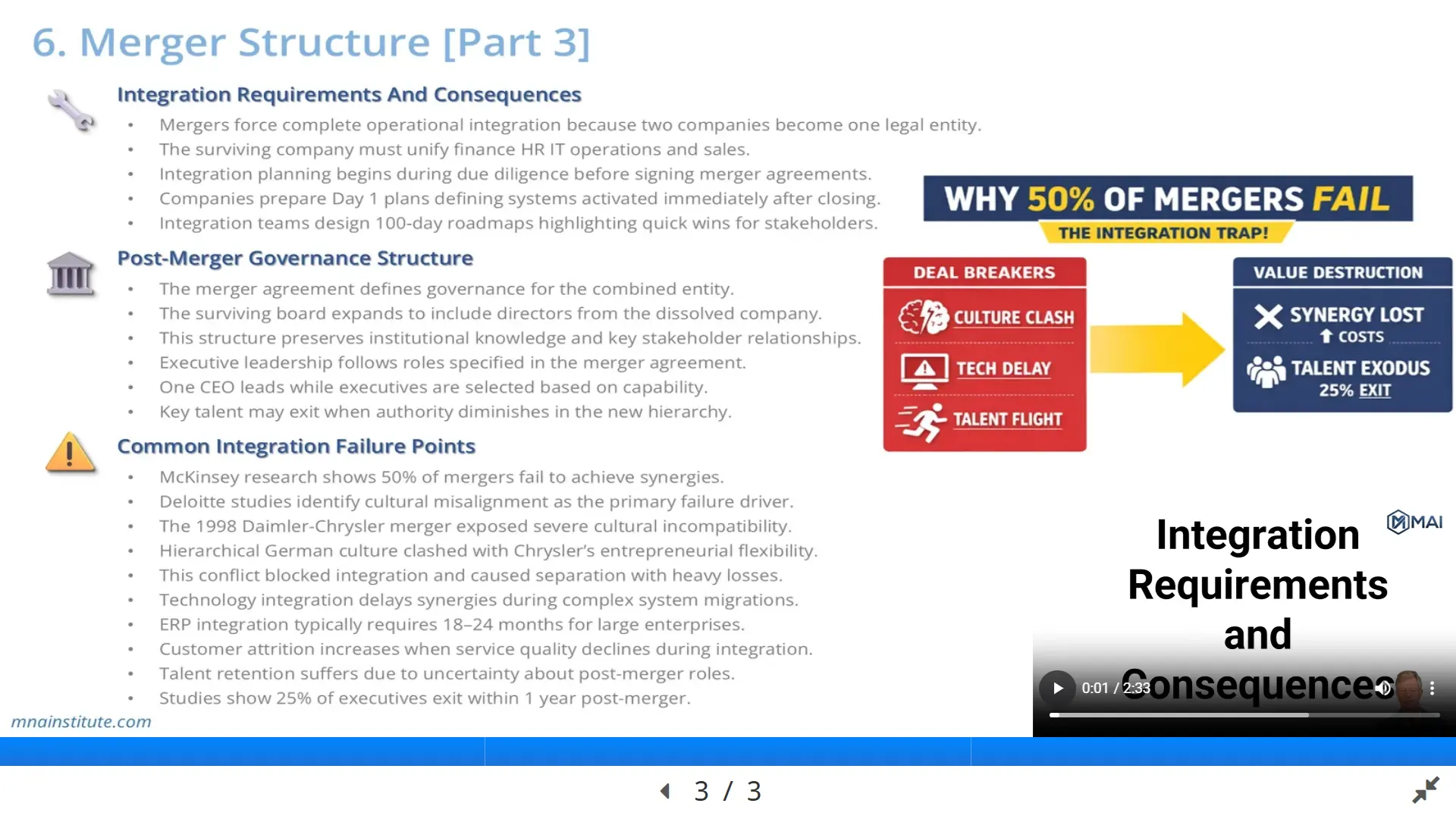

A statutory merger can be legally clean and still fail economically.

That is the uncomfortable truth behind many disappointing transactions.

McKinsey has long noted that a large share of mergers do not deliver the value expected, and Deloitte’s M&A work continues to show that culture and people factors are major causes of failure or underperformance. (McKinsey & Company)

Below are the failure points that matter most in practice.

1. Cultural misalignment

Culture problems rarely show up as a line item in the deal model.

They show up as slow decisions, mistrust, political behavior, executive exits, and missed commercial coordination.

Deloitte notes that cultural integration issues are a meaningful root cause of failed M&A outcomes, and its culture in M&A analysis argues that leaders often underweight culture even when financial logic appears sound. (Deloitte)

The Daimler Chrysler combination remains a well known cautionary example.

The strategic rationale looked powerful on paper.

The human operating model did not hold together.

When one side expects hierarchical decision making and the other side works through speed and entrepreneurial flexibility, the combined company does not become more efficient simply because the legal structure says it is one entity.

2. Technology integration bottlenecks

Technology integration is where many statutory merger ambitions hit reality.

It is easy to announce one company.

It is much harder to run one company across ERP, CRM, procurement, treasury, payroll, HRIS, and reporting systems.

A combined company can survive with temporary interfaces.

It cannot capture full merger synergies for long if core systems remain fragmented.

When finance closes on different ledgers, inventory definitions differ, customer hierarchies conflict, and procurement approval routes remain inconsistent, management loses visibility and speed.

That delays both cost and revenue synergy capture.

3. Customer attrition during transition

Customers are not required to admire your integration logic.

They care about service levels, response times, pricing clarity, and continuity of contact.

A statutory merger can interrupt all four if the commercial integration plan is weak.

Invoices may change.

Support contacts may change.

Product bundles may change.

Account managers may leave.

If the customer experience deteriorates while the companies are busy integrating internally, revenue synergy can quickly become revenue leakage.

4. Talent retention failure

Many mergers underestimate how quickly uncertainty pushes high performers to consider other options.

PwC’s integration survey highlights the importance of early change management, culture assessment, and retention planning because human capital risk sits near the center of post close execution. (PwC)

This matters even more in a statutory merger because the dissolved company’s managers often face a direct loss of title, span, or autonomy.

If the surviving company waits too long to define roles, competitors recruit the very people who understand the customer base, the product architecture, and the local market relationships.

5. Synergy optimism without accountability

The final failure point is the most common.

Teams announce large synergy numbers without linking them to named owners, timing assumptions, system dependencies, and measurement rules.

Cost synergies and revenue synergies sound impressive in board materials.

They create value only when each target has:

- a baseline

- an owner

- a timing schedule

- a dependency map

- a reporting method

- a governance escalation path

If none of those exists, the statutory merger may still close successfully in a legal sense.

But the merger synergies will remain hypothetical.

A Statutory Merger Is a Legal Form Only if Management Lets It Be

A statutory merger is often described as a legal mechanism.

That description is correct and incomplete.

The more useful practical view is this.

A statutory merger is a merger structure that can make deep operating integration easier, faster, and more enforceable than looser deal designs.

That is why it appears so often in transactions built around merger synergies.

But no statutory merger creates value automatically.

Value is created when management aligns the merger structure with the real sources of cost synergies and revenue synergies, chooses the right version of absorption merger vs consolidation merger, designs a workable governance model, and executes integration with discipline after close.

That is the difference between a legally completed transaction and a commercially successful one.

If you want a practical end to end framework for how statutory merger decisions connect to synergy planning, diligence, negotiation, integration, and value creation, the Mergers and Acquisitions Online Course is the best place to start.

If you want to go deeper into the process phase, the Merger and Acquisition Process Course breaks down how transactions move from strategic rationale to execution.

If your focus is execution after close, the Post-Merger Intergration and Value-Up Strategy course is the most directly relevant next step because that is where merger synergies are either captured or lost.

Sources

- Delaware General Corporation Law, merger and consolidation provisions. (Delaware Code)

- McKinsey, perspectives on merger integration success and value creation. (McKinsey & Company)

- Deloitte and PwC, research on culture, human capital, and integration execution in M&A. (Deloitte)