Merger vs Acquisition – 4 Powerful Deal Structure Rules

A buyer signs the purchase agreement, wires the funds, and takes ownership of the target.

Two weeks later, the combined company loses a major customer, three senior engineers resign, and the projected synergies are quietly revised downward.

Most of the time, this outcome was decided before anyone met at the negotiating table.

It was decided at the moment the parties settled the merger vs acquisition question.

The merger vs acquisition decision is not a technicality that lawyers handle after the numbers are agreed.

It determines who retains control, which liabilities transfer, how goodwill is recorded, and whether the customers who valued the target still recognize the company they bought from.

A sharp merger vs acquisition analysis also shapes the financing structure, the regulatory timeline, and the cultural reality that employees experience on day one.

Understanding the merger versus acquisition choice is therefore the starting point for anyone serious about dealmaking, whether in corporate development, private equity, or the advisory seat.

This article walks through the merger vs acquisition structural distinctions and the situations where each route produces the better result.

Two Primary Acquisition Structures and How They Differ From Mergers

The merger vs acquisition debate begins with a legal fact that matters more than most first-time buyers realize.

A statutory merger dissolves one of the two companies into the other, leaving a single surviving legal entity.

An acquisition leaves both companies intact as separate legal persons, with the buyer holding ownership of the target as a subsidiary.

That single difference cascades into every downstream issue, including contracts, tax basis, employee continuity, regulatory exposure, and integration speed.

Under the acquisition route, the buyer becomes the parent company with full ownership and operational control.

The target continues to exist under its own corporate name, with its own board, its own contracts, and, in most cases, its own workforce.

This is the practical heart of the merger vs acquisition distinction: in one case the target survives with its legal personality intact, in the other it disappears into the acquirer.

For publicly listed targets, the buyer typically extends a tender offer to shareholders at a defined price.

For private targets, the buyer negotiates a share purchase agreement with the majority shareholders or with every owner, depending on the ownership register.

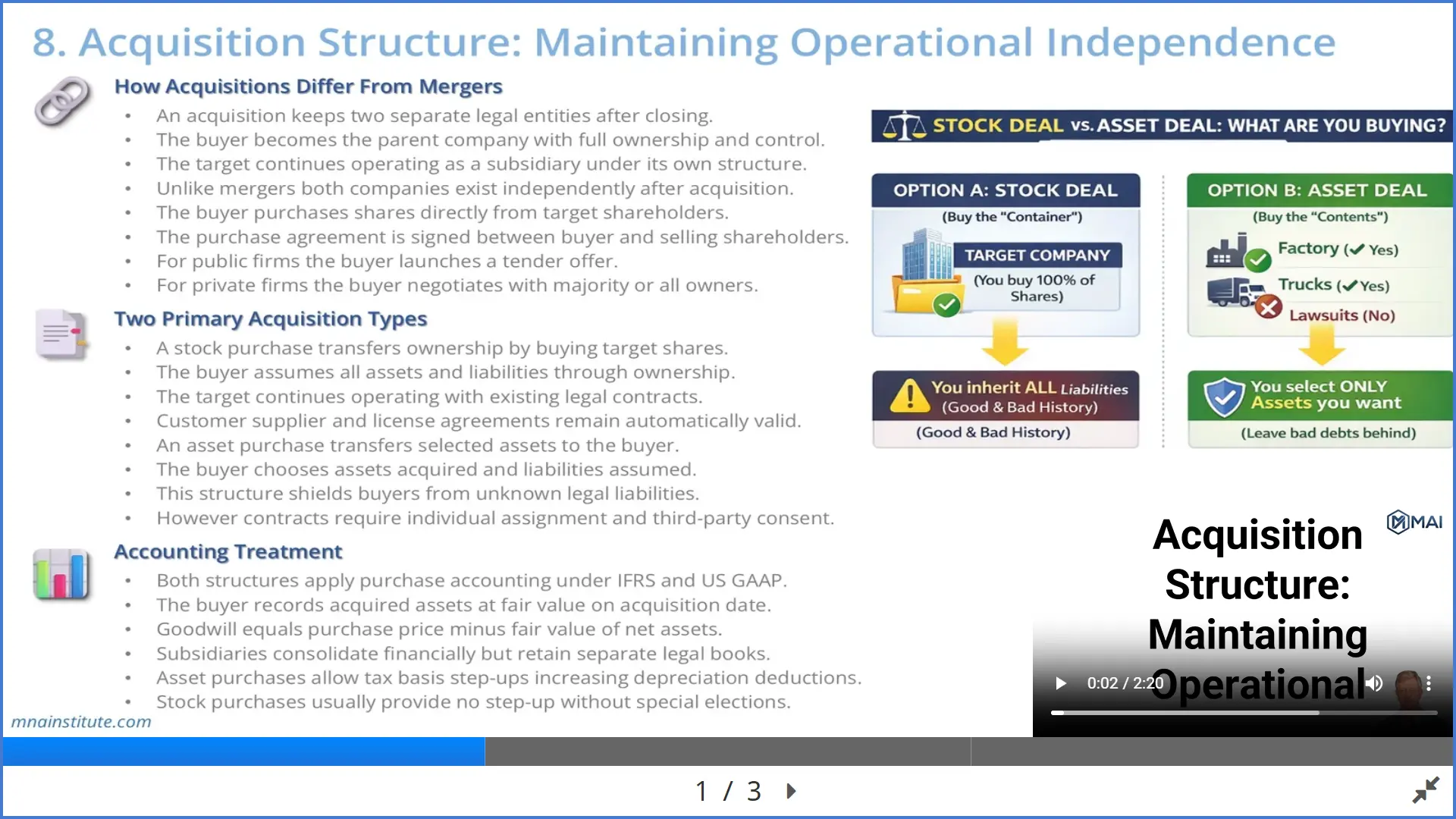

Stock Purchase vs Asset Purchase

Once the acquisition route is chosen, the next question is how the ownership transfer actually happens.

The stock purchase vs asset purchase choice is the second fork in the road, and it carries consequences that are often misunderstood until the deal is already at signing.

In a stock purchase, the buyer acquires the target’s shares directly from its shareholders.

Everything the target owns and owes transfers automatically, because the legal entity itself has simply changed hands.

Customer contracts, vendor relationships, real estate leases, intellectual property licenses, and employee arrangements stay in place, because the counterparty is still the same company.

This is usually the fastest path to closing when the target operates in a contract-dependent business such as software licensing, construction, or regulated financial services.

The trade-off is that every known and unknown liability travels with the shares, including ongoing litigation, historical tax exposure, environmental obligations, product warranty claims, and pension deficits.

In an asset purchase, the buyer selects specific assets and assumes specific liabilities rather than taking the target company whole.

This acquisition structure is common when the target has attractive operating assets but also carries risks the buyer wants to isolate.

A buyer acquiring a specialty chemicals manufacturer, for instance, may take the plants, inventory, customer list, and brand while leaving behind historical environmental liabilities tied to older facilities.

The protection is real, but the friction is also real.

Each material contract typically requires a novation or assignment, often with third-party consent, which introduces delay and gives counterparties a moment to renegotiate terms.

Employee transfers follow jurisdiction-specific rules: in the UK under TUPE, in the EU under the Acquired Rights Directive, and in the US generally under a rehire model.

Accounting and Tax Consequences

Both share and asset purchases use purchase accounting under International Financial Reporting Standards and under US Generally Accepted Accounting Principles.

The buyer records the acquired business at fair value on the closing date, and goodwill equals the purchase price minus the fair value of identifiable net assets.

From a tax standpoint, the two routes behave differently.

An asset purchase typically delivers a stepped-up tax basis, which means the buyer can depreciate and amortize the acquired assets from their new fair value rather than the target’s historical book value.

Over the life of the assets, this reduces taxable income and increases after-tax cash flow.

A stock purchase, by default, does not create a step-up, because the legal entity and its tax basis pass through unchanged.

In the US, a Section 338(h)(10) election allows certain stock purchases to be treated as asset purchases for tax purposes, but only in specific circumstances and with the seller’s consent.

In cross-border transactions, local elections differ, and buyers routinely factor tax leakage into the headline valuation.

Two practical conclusions follow from this section.

First, the merger versus acquisition distinction is not cosmetic, because it changes who survives and who dissolves.

Second, within the merger vs acquisition framework, the stock purchase vs asset purchase decision dictates what actually transfers on day one and what the buyer pays in cash, risk, and post-closing tax treatment.

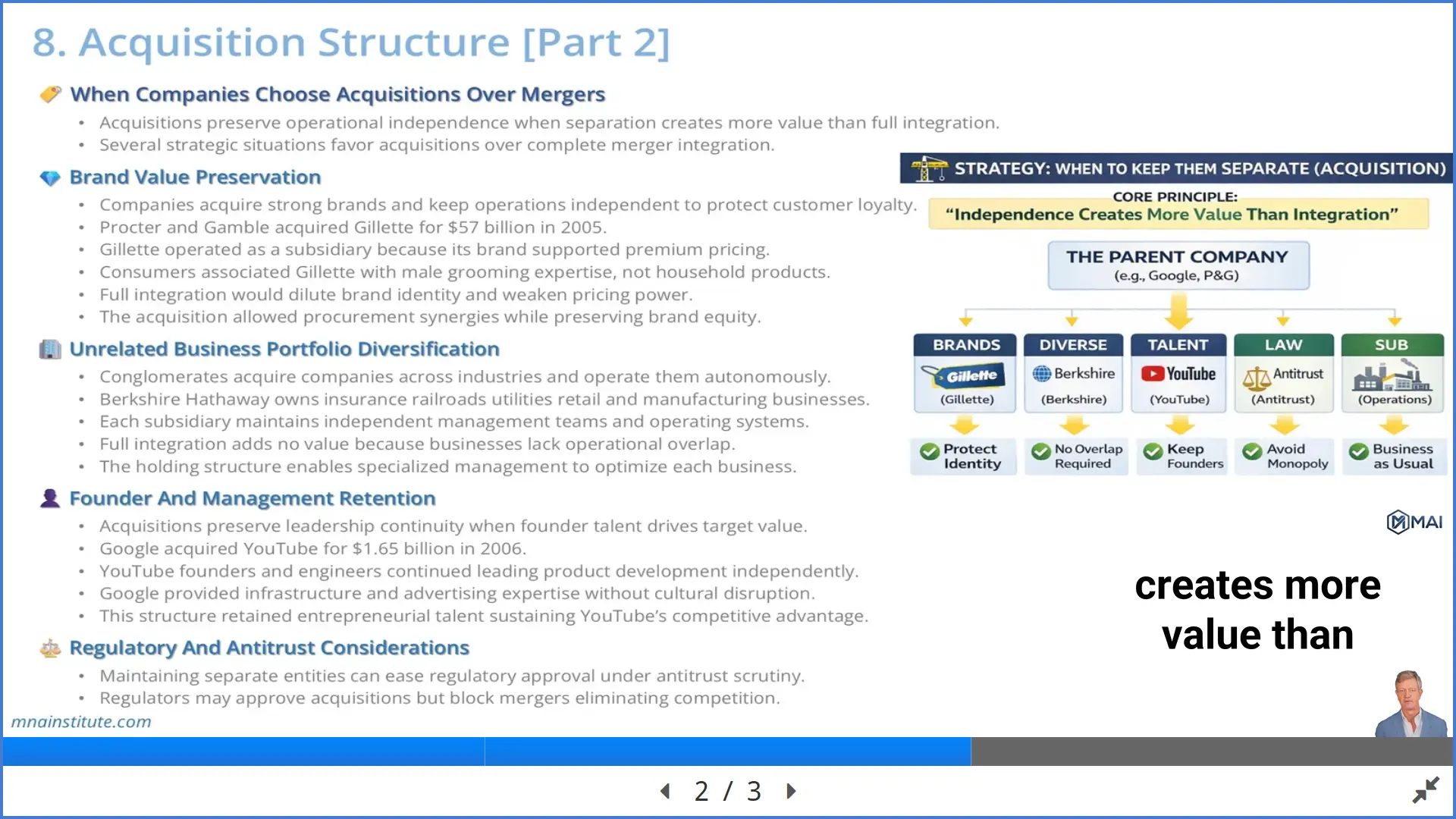

When Companies Choose Acquisitions Over Mergers

Not every transaction benefits from full integration.

Sometimes the value the buyer is paying for is the exact thing that integration would destroy.

Understanding when companies choose acquisitions over mergers starts from this test: would combining the two organizations strengthen what the target is good at, or would it erase it?

When the answer points to erasure, the merger vs acquisition decision almost always favors an acquisition structure with operational independence.

1. Brand Value Preservation

The clearest case sits in consumer markets, where customers pay premiums for identity as much as for performance.

Procter and Gamble acquired Gillette in 2005 in a transaction valued at approximately 57 billion dollars.

Gillette continued to operate under its own brand and with a distinct commercial organization, because the premium that consumers associated with the Gillette name was tied to its focused identity in grooming.

Folding Gillette into P&G’s diversified consumer goods portfolio would have diluted that identity at exactly the moment the buyer was counting on it to justify the price.

By keeping the subsidiary structurally separate, P&G consolidated procurement, media buying, and back-office operations without touching the brand experience that customers were paying for.

This is the clearest answer to the merger vs acquisition question in brand-driven categories.

2. Portfolio Diversification Without Operational Overlap

Conglomerate acquirers face a different problem.

When the businesses in a portfolio operate in unrelated industries, there is no operational gain from integration.

Berkshire Hathaway is the textbook illustration: insurance, railroads, utilities, retail, and manufacturing all sit under one holding company, each with its own management team, its own customers, and its own operating model.

Full integration would not create synergies here.

It would destroy the specialized expertise that made each acquisition worth making in the first place.

The acquisition structure exists precisely to allow this split, with ownership and capital allocation at the parent and operating decisions at the subsidiary.

3. Founder and Management Retention

In technology and innovation-driven industries, the value inside a target is often concentrated in a small group of people.

Google acquired YouTube in 2006 in a deal valued at 1.65 billion dollars.

The founding team and the core engineers continued to lead product development after closing, with Google providing infrastructure, advertising technology, and legal resources without taking over the product roadmap.

The retention of the founders was not a courtesy.

It was the entire thesis of the deal.

Had Google dissolved YouTube into its own product organization, the culture that produced YouTube’s breakout would have dispersed, and the strategic rationale would have collapsed with it.

A parallel logic shaped Facebook’s acquisition of Instagram in 2012.

The backend infrastructure was eventually integrated with Facebook’s systems to benefit from scale, but the Instagram product and brand team remained autonomous.

That autonomy preserved the distinct user experience that attracted the one billion dollar price tag in the first place.

In founder-led technology businesses, the merger vs acquisition choice almost always tilts toward acquisition, because the target is the team, and the team needs room to keep building.

4. Regulatory and Antitrust Considerations

Regulators evaluate deals through a concentration lens: does the transaction reduce competition in a defined market?

Maintaining two separate legal entities after closing can make the difference between a deal that clears review and a deal that gets blocked.

If the subsidiaries continue to price, compete, and sell independently, regulators may conclude that consumer choice has not been materially reduced.

If the parties announce a full merger with a single combined sales force and a unified pricing strategy, the same transaction may face divestiture demands or outright prohibition.

For cross-border deals, this becomes a multi-jurisdictional exercise, with the European Commission, the US Department of Justice, the UK Competition and Markets Authority, and regulators in Korea, Japan, and China often applying different thresholds.

Antitrust exposure is one of the most common reasons when companies choose acquisitions over mergers, because preserving competitive independence can turn an otherwise blocked transaction into a cleared one.

5. Private Equity and the Speed Calculation

Private equity firms almost always prefer the acquisition structure, and the reason is mechanical rather than ideological.

A fund needs to produce a return within a defined holding period, usually three to seven years.

Finding the right target starts well before structuring decisions, and systematic deal sourcing discipline separates consistent acquirers from opportunistic ones.

Acquisition ownership gives the general partner clean authority to install new management, redirect capital expenditure, refinance the balance sheet, and drive operational change on a timetable that matches the planned exit.

A merger structure would require consensus with a second party that no longer exists in a typical private equity deal, which is why leveraged buyouts are universally structured as acquisitions.

The pattern across these categories is consistent.

An acquisition is the right answer whenever the target’s value is embedded in something that combination would damage: brand equity, founder talent, portfolio independence, regulatory tolerance, or speed of control.

A merger is the right answer when the two organizations are genuinely more valuable combined than separate, and when the capability to execute a full integration exists on both sides.

Framed this way, the merger vs acquisition decision stops being an abstract legal question and becomes a commercial test about where value actually lives.

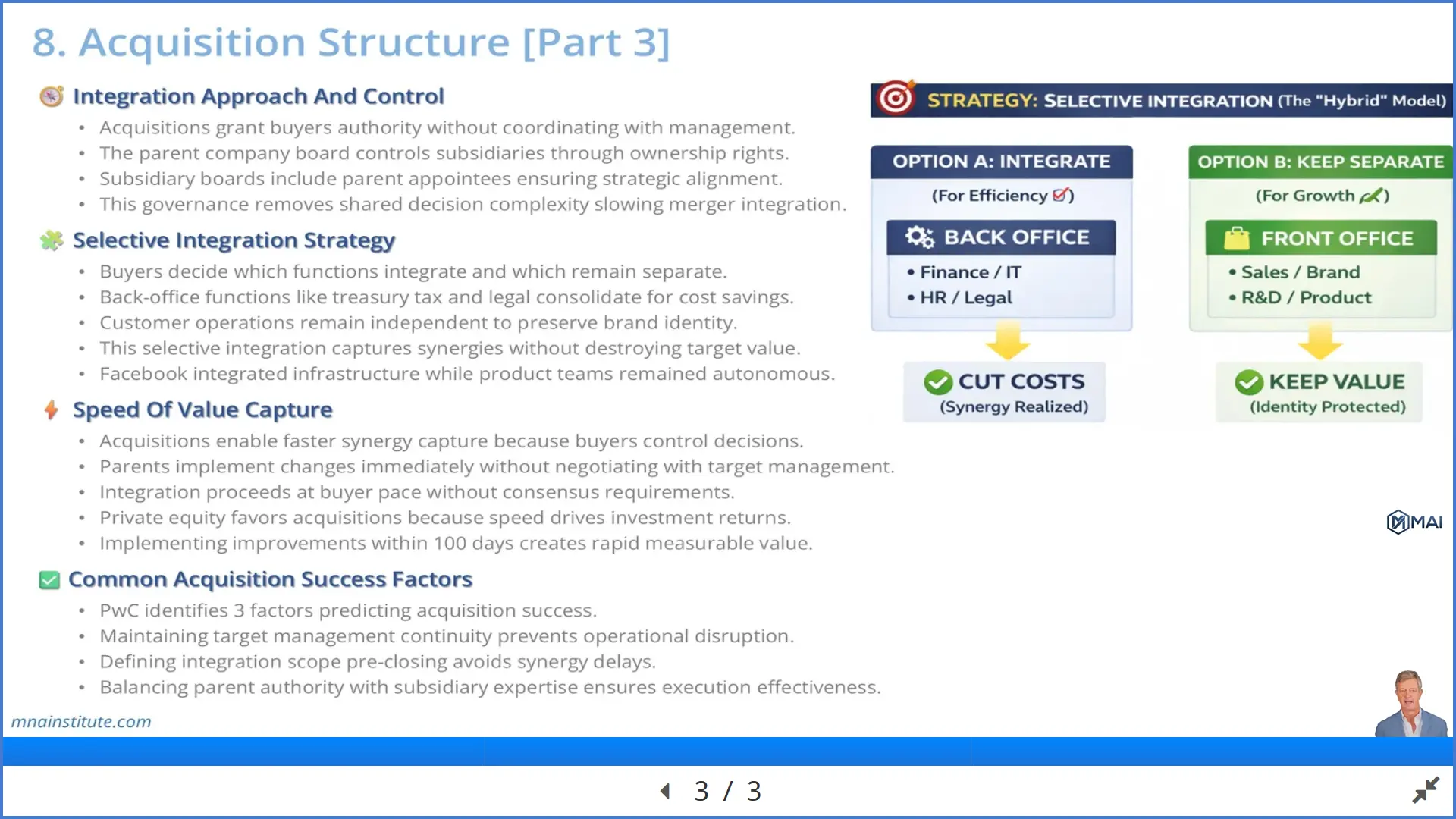

Post-Transaction Governance Structure

Once closing is complete, the merger vs acquisition choice continues to shape daily operations through the governance structure that survives.

In a merger, a single combined entity operates under one board and one management team.

In an acquisition, the subsidiary retains its own board, typically reconstituted to include parent company appointees, while the parent exercises strategic control through its ownership of the shares.

Board Control and Decision Rights

The parent’s board controls the subsidiary through standard corporate governance mechanisms, including director appointments, reserved matters, and shareholder resolutions.

Operating decisions such as hiring, pricing, and vendor selection typically remain with subsidiary management, while capital allocation, major strategic moves, and executive compensation require parent approval.

This creates a cleaner decision architecture than a merger, where every significant choice requires alignment between two formerly independent leadership teams who may have joined under very different expectations.

The governance layer is one of the most underappreciated dimensions of the merger vs acquisition trade-off, because it determines how quickly the buyer can actually act on its thesis.

Selective Integration

The acquisition structure makes selective integration possible in a way that a full merger does not.

Buyers commonly integrate back-office functions to capture cost savings, including treasury management, tax compliance, audit, legal support, procurement, and information technology infrastructure.

Customer-facing functions are the opposite case: sales teams, account managers, brand marketing, and product development usually remain independent when the target’s value depends on its relationships or its identity.

When Facebook acquired Instagram, backend infrastructure merged with Facebook’s systems to gain scale, but Instagram’s product team continued to set its own roadmap.

This pattern, deep integration in support functions and independence in customer-facing operations, appears repeatedly across successful acquisitions.

Speed of Value Capture

Acquisitions typically capture synergies faster than mergers because the parent does not need to negotiate with a counterpart.

When the parent decides to consolidate a shared services center or refinance the subsidiary’s debt, the decision executes at the parent’s chosen pace.

PwC’s 2023 M&A Integration Survey reports that long-term operating models are increasingly planned during deal screening, well before signing, which lets successful acquirers begin extracting value within the first 100 days of ownership.

For private equity sponsors, this speed translates directly into internal rate of return, because every month of delayed synergy capture reduces the compounding value of the fund’s investment.

Common Integration Failure Points

Even well-structured acquisitions fail with uncomfortable frequency.

Harvard Business Review has repeatedly cited failure rates between 70 and 90 percent across historical studies of M&A outcomes, a range that holds across industries, deal sizes, and decades.

A sound merger vs acquisition decision at the structuring stage does not guarantee success, but a poor one makes failure almost inevitable.

The failure modes are not mysterious.

The first is cultural mismatch that is discovered after closing rather than diagnosed before it.

When the acquirer assumes a uniform corporate culture will take hold, and the subsidiary’s people do not see themselves in that culture, key employees leave within the first two years and carry institutional knowledge with them.

The second is scope creep during integration.

An acquisition that was supposed to preserve the target’s independence quietly expands into a partial merger, as central functions reach deeper into the subsidiary in pursuit of incremental savings.

By the time customers or regulators notice, the brand equity or regulatory standing that justified the acquisition structure has already eroded, and the original merger vs acquisition rationale no longer describes what the combined company has become.

The third is over-reliance on due diligence without rigorous post-closing follow-through.

BCG research on post-merger integration finds that more than half of transactions fail to realize their projected value, largely because integration planning is treated as a closing deliverable rather than as the central operating challenge of the first year.

The fourth is governance drift.

When the parent appoints directors to the subsidiary board but fails to give them clear mandates, decisions stall at the subsidiary level, and control provisions that were not precisely defined during deal negotiation become the source of paralysis.

Structural Fluency Across the Full Deal Lifecycle

The merger vs acquisition decision is the first and most consequential choice in any transaction, because it defines what the buyer is actually acquiring and how that value is protected after closing.

Every downstream workstream, from due diligence scope to financing structure to post-merger integration, either reinforces or undermines that initial decision.

M&A Institute’s curriculum on mergers and acquisitions covers every stage of the deal lifecycle, from the first structural decision through execution and value creation.

Sources

- PwC 2023 M&A Integration Survey, PricewaterhouseCoopers

- Post-Merger Integration Framework, Boston Consulting Group

The Big Idea: The New M&A Playbook, Clayton M. Christensen et al., Harvard Business Review