Mergers and Acquisitions Negotiation: 4 Critical Levers for Deals

A buyer finishes due diligence on a target company and discovers three uncomfortable facts.

One customer represents 32% of revenue, working capital has been running below the level shown in the management presentation, and a tax exposure may not be fully reserved.

The headline valuation may still be attractive, but the buyer can no longer treat the agreed price as clean.

The seller does not want to reopen the entire deal because the buyer already spent months reviewing the business and the financing deadline is approaching.

This is the practical setting where mergers and acquisitions negotiation becomes serious.

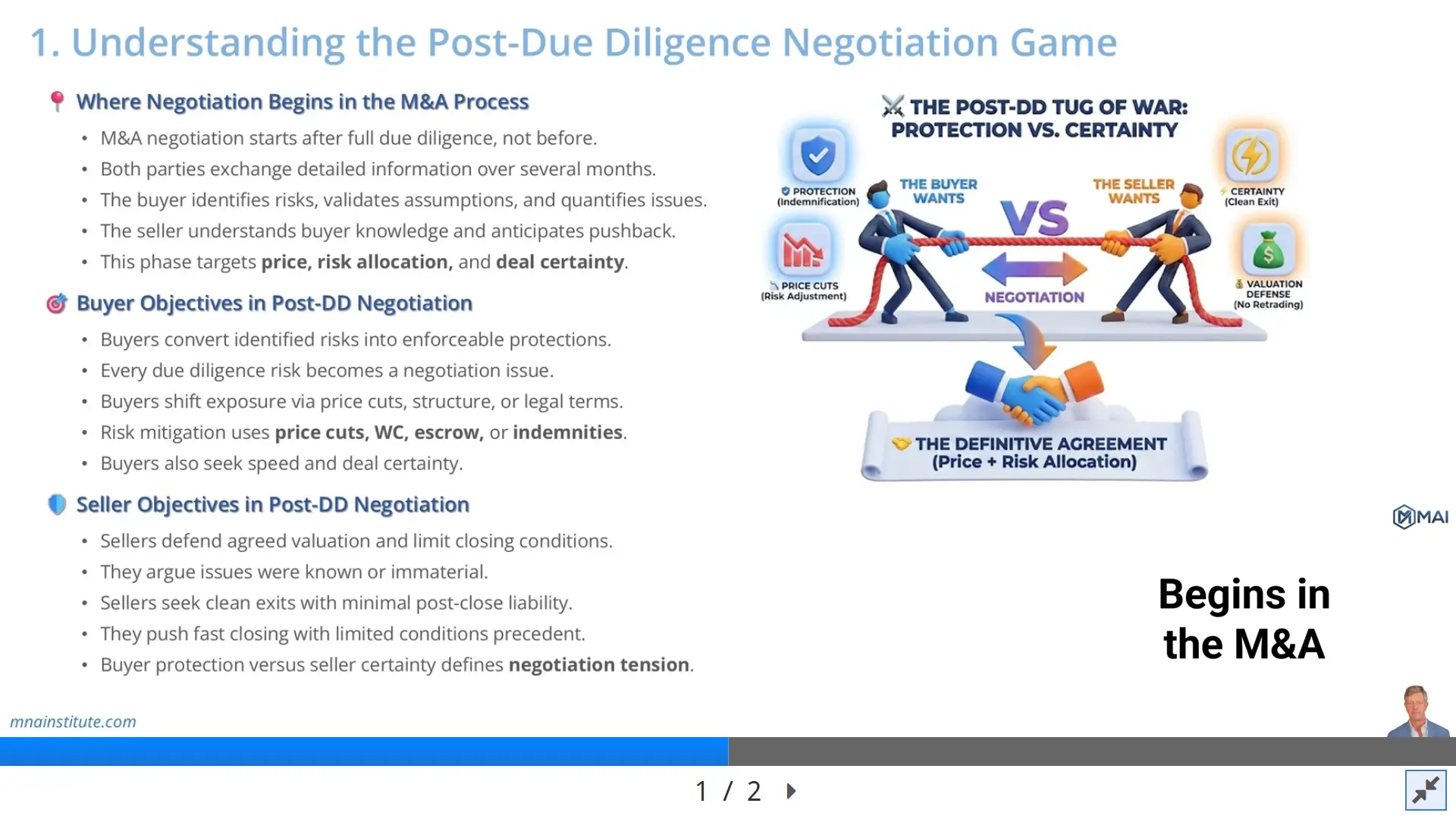

Before due diligence, negotiation often feels like a debate over value.

After due diligence, negotiation becomes a controlled fight over who carries each identified risk.

The buyer wants protection without losing the transaction.

The seller wants closing certainty without giving away too much value.

The strongest M&A deal negotiation does not ask for every possible protection.

It matches each risk to the right lever, such as price, working capital, escrow, indemnity, or closing condition.

That is the core of this guide to mergers and acquisitions negotiation.

Section 1. Where Mergers and Acquisitions Negotiation Begins in the M&A Process

Mergers and acquisitions negotiation does not begin after every party has perfect information.

It begins when the buyer has enough information to convert uncertainty into specific claims.

Early negotiation usually focuses on valuation logic, strategic rationale, process timetable, and broad transaction structure.

Post due diligence negotiation is different because both sides have already exchanged detailed data.

The buyer has reviewed financial statements, customer data, contracts, operations, tax matters, management information, and sometimes site-level evidence.

The seller understands which issues the buyer is likely to use as leverage.

At this stage, the discussion is no longer theoretical.

A customer issue may become an escrow request.

A debt-like item may become a net debt adjustment.

A weak working capital position may become a closing accounts dispute.

A legal exposure may become a specific indemnity.

A regulatory concern may become a condition precedent.

This is why basic negotiation in M&A should be taught as a risk translation exercise, not as a generic bargaining exercise.

The negotiation phase has three practical objectives.

This makes mergers and acquisitions negotiation a structured commercial discipline rather than a last-minute pricing argument.

- Finalize the price that will actually be paid at closing.

- Allocate known and unknown risks between buyer and seller.

- Preserve enough deal certainty for both sides to continue toward signing and closing.

Those objectives often conflict with each other.

A buyer can reduce risk by demanding a lower price, a larger escrow, stronger indemnities, and more closing conditions.

But asking for every protection at once may convince the seller that the buyer is retrading the deal.

A seller can preserve certainty by resisting every adjustment and insisting that diligence findings are already reflected in the original price.

But refusing to address real findings may cause the buyer to question whether the seller is hiding deeper problems.

Good mergers and acquisitions negotiation lives between those two extremes.

Section 2. Buyer Objectives in Mergers and Acquisitions Negotiation After Due Diligence

Buyers enter post due diligence negotiation with a simple question.

What did we find, and how should the deal protect us from it.

Every due diligence finding can become a negotiation point, but not every finding deserves the same treatment.

A small reporting weakness may require better interim information before closing.

A material working capital shortfall may require a purchase price adjustment.

A tax exposure may require a specific indemnity.

A litigation risk may require escrow support if the seller has limited credit strength after closing.

A customer concentration issue may require a combination of price discipline, customer retention analysis, and post-closing revenue protection.

Buyer behavior in acquisition negotiations usually falls into four categories.

- Direct price cuts when the risk reduces the economic value of the target today.

- Structural adjustments when the risk affects closing financials such as working capital, cash, debt, or earnouts.

- Legal protections when the buyer wants recourse if pre-closing facts later create loss.

- Closing conditions when the buyer needs a walk-away right if a defined event is not resolved before closing.

The buyer also needs speed.

In mergers and acquisitions negotiation, speed matters because uncertainty can weaken financing, board confidence, and stakeholder commitment.

A deal team, financing bank, board committee, tax adviser, legal counsel, and integration team may already be mobilized.

Long uncertainty can damage process momentum and increase execution cost.

That is why a buyer should not translate every problem into a price reduction.

Price is only one lever in mergers and acquisitions negotiation.

For example, imagine a buyer discovers that the target has a possible warranty claim exposure of 5 million dollars.

If the claim is highly uncertain, a direct 5 million dollar price cut may be hard to justify.

A more balanced solution could be a 5 million dollar escrow for 18 months with release mechanics tied to claim resolution.

The seller avoids an immediate price concession if the risk never materializes.

The buyer receives a funded source of recovery if the risk becomes real.

That is a stronger negotiation structure than simply arguing over valuation language.

The buyer objective is therefore not maximum protection in the abstract.

The objective is risk protection that is enforceable, commercially credible, and proportionate to the finding.

Section 3. Seller Objectives in Mergers and Acquisitions Negotiation After Due Diligence

Sellers enter post due diligence negotiation with a different fear.

In mergers and acquisitions negotiation, the seller is not only defending price but also defending the probability of closing.

They worry that the buyer will use every discovered issue to reopen a price that was already negotiated.

The seller usually wants three outcomes.

- Defend the original valuation.

- Minimize post-closing obligations.

- Protect closing certainty.

Sellers often argue that identified issues were known, immaterial, already disclosed, or already captured in the agreed valuation.

That argument can be reasonable when the buyer is using ordinary business risk as leverage.

It becomes weaker when diligence identifies a specific exposure that was not visible when the initial valuation was negotiated.

A seller also wants a clean exit.

This matters especially in private company sales where the seller may distribute proceeds, repay investors, or leave the business after closing.

Broad indemnification, long survival periods, high escrow amounts, and open-ended conditions precedent all reduce the seller’s certainty.

A seller may accept a targeted indemnity for a known tax matter but resist broad indemnity language that effectively keeps the seller exposed to ordinary business risk.

This is the reason mergers and acquisitions negotiation often becomes a trade between economic value and legal comfort.

The seller may accept a smaller price concession if the buyer reduces the escrow request.

The buyer may accept a lower indemnity cap if the seller provides stronger financial warranties.

The seller may accept a working capital target if the buyer accepts clear accounting principles for the closing statement.

Both sides are solving for the same end point from opposite directions.

The buyer wants enough protection to proceed.

The seller wants enough certainty to sign.

The tension between buyer protection and seller certainty defines advanced M&A deal negotiation.

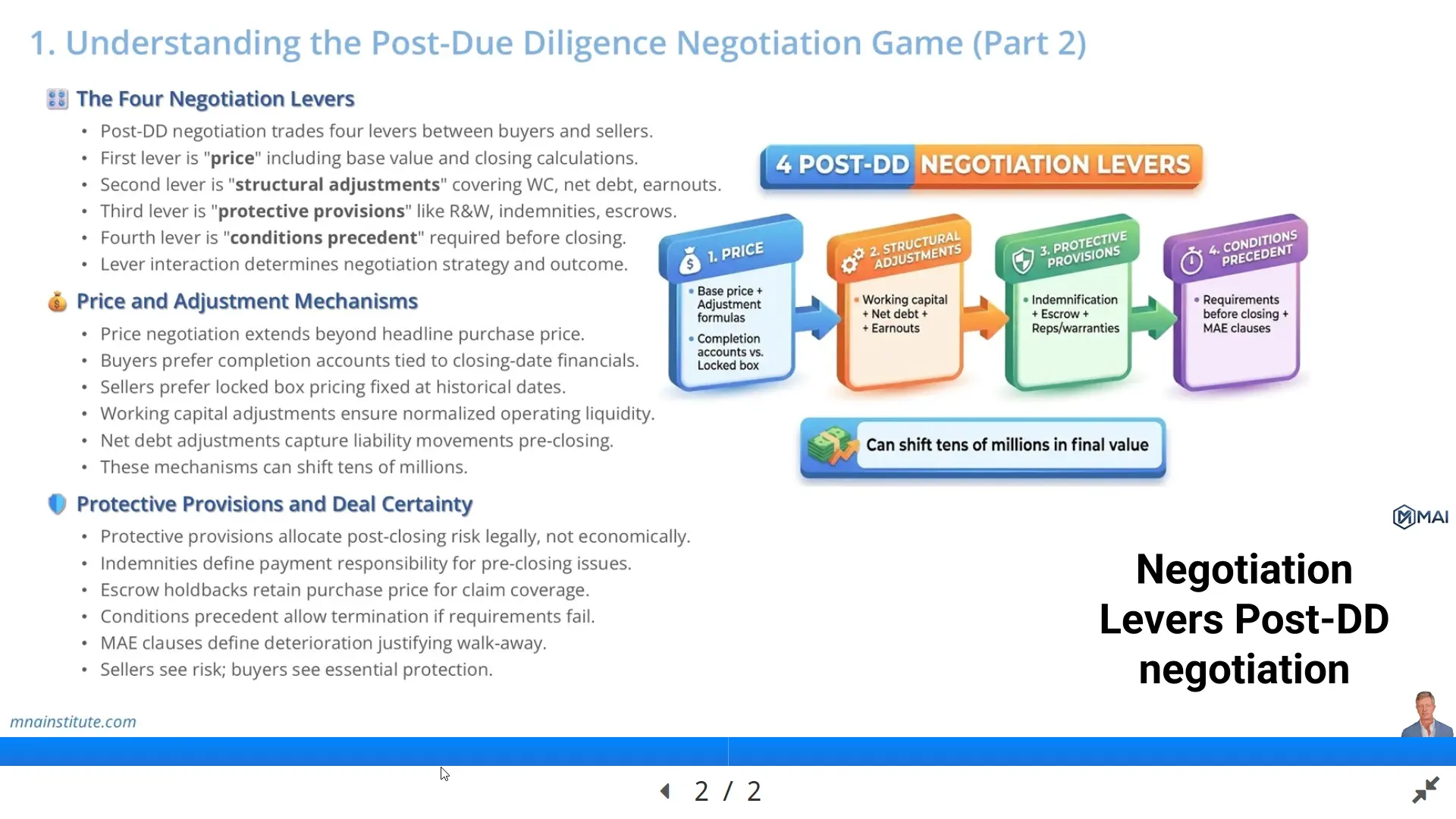

Section 4. The Four Levers in Mergers and Acquisitions Negotiation

Post due diligence mergers and acquisitions negotiation usually revolves around four levers.

These levers are price, structural adjustments, protective provisions, and conditions precedent.

The mistake is to view them separately.

In real acquisition negotiations, the levers work together.

Lever 1: Price

Price includes the headline purchase price, any direct reductions, and the way equity value will be converted into final consideration.

A buyer seeks a direct price cut when a diligence finding reduces expected cash flow, growth, margin, or enterprise value.

A seller resists when the issue is temporary, already known, or manageable after closing.

Lever 2: Structural Adjustments

Structural adjustments change the economics without always changing the headline price.

They include working capital mechanisms, net debt calculations, cash adjustments, earnout formulas, deferred consideration, and sometimes retention of specific liabilities.

This lever is often more precise than a blunt valuation cut.

Lever 3: Protective Provisions

Protective provisions allocate post-closing risk through legal language.

They include representations, warranties, indemnification, caps, baskets, survival periods, specific indemnities, and escrow arrangements.

These provisions do not always reduce price today, but they determine who pays if a pre-closing issue becomes a loss later.

Lever 4: Conditions Precedent

Conditions precedent define what must happen before closing can occur.

They may cover regulatory approvals, third-party consents, financing availability, no material adverse effect, or completion of specific remediation steps.

They give the buyer a protection route before closing rather than a claim route after closing.

A practical example shows the interaction.

This is where mergers and acquisitions negotiation becomes more analytical than ordinary bargaining.

Assume due diligence shows that a target has one customer representing 40% of revenue and the contract is up for renewal two months after signing.

A buyer could ask for a price reduction because future revenue is uncertain.

The seller may reject this because the customer has renewed for years.

A more structured solution may combine a modest price adjustment, a condition requiring no termination notice before closing, and an earnout tied to customer renewal.

The economic outcome depends on future evidence rather than on a single negotiation speech.

This is why basic negotiation in M&A becomes more powerful when the negotiator understands the available levers.

Section 5. Price and Adjustment Mechanisms in Mergers and Acquisitions Negotiation

Price negotiation in mergers and acquisitions negotiation extends beyond the headline number.

The parties must decide how the price will be measured, tested, and adjusted between signing and closing.

Two mechanisms appear often in private company transactions.

The first is completion accounts.

The second is locked box pricing.

Completion Accounts

Under completion accounts, the final price adjusts based on actual financial information at closing.

The buyer tends to prefer this structure when it wants the final consideration to reflect the target’s actual cash, debt, and working capital position on the closing date.

The mechanism may protect the buyer if the target leaks cash, increases debt, or allows working capital to fall below an agreed normalized level before closing.

The weakness is that completion accounts can create post-closing disputes over accounting policies, estimates, classifications, and calculation methods.

Locked Box

Under a locked box, the parties fix the price by reference to a historical balance sheet date.

The seller tends to prefer this structure because it gives price certainty at signing and reduces the need for a post-closing price calculation.

The buyer must be comfortable that the locked box balance sheet is reliable and that leakage protections prevent value transfer to the seller between the locked box date and closing.

The negotiation therefore moves from closing accounts to locked box date quality, permitted leakage, leakage claims, and interim conduct controls.

Working Capital and Net Debt

Working capital adjustments address whether the target has enough operating capital at closing to run the business normally.

A buyer does not want to pay full price for a company and then immediately inject cash because receivables are weak, payables were stretched, or inventory is insufficient.

A seller does not want the buyer to manipulate the target level by applying aggressive assumptions after the deal economics were agreed.

A clear working capital target, calculation method, and dispute mechanism reduce the risk of later conflict.

Net debt adjustments address financial liabilities that affect equity value.

Debt-like items may include loans, overdrafts, finance leases, unpaid transaction expenses, tax liabilities, or other obligations depending on the agreement.

This is where legal drafting and financial analysis meet.

A term that looks technical can move substantial value from one side to the other.

For example, suppose a business is valued at 100 million dollars on a cash-free and debt-free basis with a normalized working capital target of 12 million dollars.

At closing, actual working capital is 9 million dollars and net debt is 4 million dollars.

If the agreement requires a dollar-for-dollar reduction for both items, the final equity consideration falls from 100 million dollars to 93 million dollars.

The buyer receives protection without reopening the enterprise value debate.

The seller can still say the headline valuation was preserved, but the final consideration reflects the actual closing balance sheet.

That is why adjustment mechanics sit at the center of mergers and acquisitions negotiation.

Section 6. Protective Provisions and Deal Certainty in Mergers and Acquisitions Negotiation

Protective provisions handle risk through the purchase agreement rather than through immediate price movement.

They are especially relevant when the buyer can identify a risk but cannot fully quantify it before signing.

Representations and warranties create factual statements about the business.

If those statements are inaccurate and the agreement provides a remedy, the buyer may have a claim after closing.

Indemnification clauses specify who bears losses connected to defined matters.

A general indemnity may cover breaches of warranties.

A specific indemnity may cover a known tax issue, litigation matter, environmental exposure, or customer claim.

Escrow holdbacks improve recovery by retaining part of the purchase price for a defined period.

Without an escrow, the buyer may have a legal right but still face recovery risk if the seller has distributed proceeds or lacks resources.

Conditions precedent protect the buyer before closing.

They may allow termination if regulatory approval is not obtained, key consents are missing, financing fails, or a material adverse effect occurs.

A material adverse effect clause defines the level of deterioration that may justify not closing.

The seller usually wants narrow wording because broad walk-away rights reduce deal certainty.

The buyer usually wants enough flexibility to avoid closing into a materially different business.

Legal protections are not equivalent to price reductions.

A price cut gives immediate economic protection.

An indemnity only helps if a covered loss occurs, the claim is brought on time, the contractual limits allow recovery, and the seller can pay.

An escrow gives stronger recovery support but may create seller resistance because it delays access to proceeds.

A condition precedent gives pre-closing protection but may create uncertainty that the seller cannot accept.

This is the central trade-off in acquisition negotiations.

Protection is valuable only when it matches the risk, the timing of the risk, and the likely recovery path.

Section 7. Practical Negotiation Map: Matching the Risk to the Lever

The fastest way to improve mergers and acquisitions negotiation is to map each due diligence finding to the correct response.

The table below shows a practical approach.

It can be used as a simple mergers and acquisitions negotiation checklist after diligence.

|

Due Diligence Finding |

Likely Negotiation Lever |

Practical Logic |

|

Customer concentration |

Escrow, earnout, targeted condition, or price adjustment |

Use price if the revenue loss is already visible; use escrow or earnout if the risk is uncertain. |

|

Working capital shortfall |

Working capital adjustment |

Use a clear target, accounting policy, and dispute process. |

|

Tax exposure |

Specific indemnity or escrow |

Use legal protection when the amount and timing remain uncertain. |

|

Debt-like liabilities |

Net debt adjustment |

Define debt-like items clearly to avoid closing disputes. |

|

Regulatory approval risk |

Condition precedent |

Use a closing condition when the issue must be resolved before ownership transfers. |

|

Weak financial warranties |

Representations, warranties, and indemnification |

Use drafting to allocate risk from inaccurate statements about the business. |

This mapping prevents two common mistakes.

The first mistake is using price reductions for every issue.

That approach can damage trust and make the seller believe the buyer is renegotiating the deal from the beginning.

The second mistake is relying on legal protections when the economic problem is already visible.

If a target has lower recurring revenue today, a warranty may not solve the valuation issue.

If a tax matter may or may not create future liability, a specific indemnity or escrow may be more logical than a broad price cut.

Strong M&A deal negotiation requires this discipline.

The question is not which side can demand more.

The question is which lever most accurately prices, transfers, or controls each risk.

Related M&A Institute Courses

Post due diligence negotiation sits at the intersection of deal process, diligence, legal drafting, and integration planning.

The following M&A Institute courses connect naturally with the issues discussed in this article.

- Mergers and Acquisitions Online Course: A full-process course for understanding how sourcing, diligence, valuation, negotiation, signing, and integration connect in real transactions.

- M&A Due Diligence: CDD, FDD, LDD, & HRDD: Useful for understanding how diligence findings become negotiation points and contractual protections.

- M&A Deal Negotiation Mastery: Focused on the negotiation logic behind price, risk allocation, seller certainty, buyer protection, and deal execution.

- Stock Purchase Agreement Mastery: Relevant when negotiation outcomes must be translated into warranties, indemnities, escrows, conditions, and closing mechanics.

- Post-Merger Intergration and Value-Up Strategy: Relevant when negotiated protections must connect with post-closing execution and value creation.

Sources

- Baker McKenzie Global Private M&A Guide, United Kingdom quick reference guide

- KPMG, Locked box and completion accounts

- Lewis Silkin, US and UK M&A price adjustment mechanisms, the locked box

- Hill Dickinson, Anatomy of a share purchase agreement