M&A in Investment Banking: 4 Conflict Types Every Client Must Understand

A company decides to sell. The board retains an investment bank, signs an engagement letter, and assumes the bank will do everything possible to maximize the sale price.

Six months later, the deal closes at a price the seller considers acceptable but not exceptional.

Only afterward does the seller’s CFO realize the bank had a lending relationship with the buyer and had pre-arranged financing for the transaction.

This scenario plays out across sell-side and buy-side mergers and acquisitions transactions more often than most clients recognize.

M&A in investment banking is a structured, high-stakes advisory service with well-defined roles, processes, and fee structures.

It also has structural conflicts built into its design that every company engaging an investment bank should understand before signing.

This article covers how the investment banking M&A process works on both sides of a mandate, how M&A advisory fees are calculated, and where client and advisor incentives diverge.

Whether you are a first-time dealmaker or an experienced CFO, understanding M&A in investment banking at this level of detail changes how you structure, manage, and evaluate your advisory relationships.

Section 1: Sell-Side Investment Banking Services

Sell-side M&A in investment banking refers to the bank representing the seller in a transaction.

The sell-side is the most common starting point for understanding M&A in investment banking because the bank takes on the greatest process responsibility in this mandate type.

The bank manages the entire sale process from preparation through closing, acting as the seller’s strategic and operational advisor throughout.

Marketing and Buyer Identification

The first task in the sell-side investment banking M&A process is preparing marketing materials and identifying the right buyers.

The bank begins by preparing a teaser document, a one or two page anonymous overview of the company that describes the business and financial highlights without disclosing the seller’s identity.

The teaser goes to a broad list of potential buyers to gauge interest before any confidential information is shared.

Buyers who express interest sign a non-disclosure agreement.

Once the NDA is executed, the bank distributes the Information Memorandum, a comprehensive document covering the company’s business model, financial performance, management team, market position, and growth opportunities.

The bank identifies two categories of buyers: strategic acquirers and financial sponsors.

Strategic acquirers are companies in the same or adjacent industries seeking operational synergies, market share, or technology access.

Financial sponsors, primarily private equity firms, focus on financial returns through operational improvement and eventual exit.

Reaching the right buyers requires more than a database search.

Experienced sell-side banks use proprietary relationships built over years of deal activity to approach qualified buyers discreetly, without triggering market rumors or alerting the seller’s competitors prematurely.

Valuation and Deal Positioning

Before approaching buyers, the bank conducts a comprehensive valuation of the seller’s business.

The valuation uses three primary methods: discounted cash flow analysis based on projected free cash flows, comparable company multiples from publicly traded peers, and precedent transaction benchmarks from similar completed deals.

The result is a valuation range, not a single number, that guides the bank’s price expectations and shapes how it responds to buyer LOIs.

Deal positioning is a dimension of M&A in investment banking that is often underappreciated relative to technical valuation work.

The bank frames the company story to highlight competitive advantages, market position, and growth trajectory in a way that makes the business compelling to the specific buyers being approached.

The bank frames the company’s story to highlight competitive advantages, market position, and growth trajectory in a way that makes the business compelling to the specific buyers being approached.

Effective positioning creates competitive tension among buyers.

When multiple qualified buyers believe they are competing for the same asset, bid prices tend to converge at the upper end of the valuation range.

Auction Process Management

The investment banking M&A process on the sell-side is typically structured as a controlled auction.

The bank runs multiple buyers simultaneously through a defined sequence of stages, each designed to filter participants while maintaining competitive pressure.

The process typically includes management presentations, where shortlisted buyers meet the seller’s leadership team to assess operations and strategy.

The bank manages the data room, a secure virtual repository that provides buyers with controlled access to financial statements, contracts, customer data, and other materials needed for due diligence.

The bank also coordinates site visits, reference calls with key customers or suppliers where permitted, and Q&A sessions addressing buyer questions.

Bid evaluation compares final offers across multiple dimensions: price, payment structure, certainty of close, financing contingencies, and timing.

A higher headline price with significant financing risk may be less attractive than a slightly lower all-cash offer from a buyer with committed capital.

Negotiation and Fairness Opinion

The bank negotiates transaction terms on behalf of the seller, covering price, payment structure, representations and warranties, and indemnification provisions detailed in the stock purchase agreement.

In public company transactions or deals requiring board approval, the bank typically issues a fairness opinion.

A fairness opinion is a formal written opinion stating whether the transaction price is fair from a financial perspective to the seller’s shareholders.

Fairness opinions exist primarily to protect board members from shareholder litigation alleging they accepted an inadequate price.

The board can point to the fairness opinion as independent financial validation of their decision.

Fairness opinions are prepared by the advising bank, which creates a potential conflict: the bank issuing the opinion also earns its success fee when the deal closes.

Section 2: Buy-Side Investment Banking Services

Buy-side M&A in investment banking refers to the bank representing the acquirer.

Mergers and acquisitions investment banking on the buy-side requires a different skill set from the sell-side because the bank is helping a client make a purchase decision rather than manage a competitive sale.

The buy-side mandate is structurally different from the sell-side because the client is making a purchase decision rather than managing a sale process.

The bank’s role shifts from process manager and marketeer to strategic advisor, target identifier, deal structurer, and financing arranger.

Target Identification and Screening

The investment banking M&A process on the buy-side begins with defining acquisition criteria and building a target list.

This origination work is where M&A in investment banking and internal corporate strategy overlap most directly.

The bank uses industry databases, proprietary market intelligence, and its own deal relationships to identify companies fitting the acquirer’s strategic profile.

Desktop screening evaluates targets using publicly available information before any confidential outreach, which mirrors the early stages of formal deal sourcing done by the acquirer’s own corporate development team.

Once targets are prioritized, the bank makes initial contact with target management or shareholders to gauge interest in a potential transaction.

For proprietary deals, where no formal sale process exists, the bank’s relationships are particularly valuable.

A bank with an existing relationship with a target’s management or board can facilitate introductions that an internal corporate development team cannot easily achieve on its own.

Valuation and Deal Structuring

On the buy-side, the bank builds valuation models to support price negotiations rather than to establish an asking price.

The analysis covers standalone DCF valuation of the target on its current trajectory and synergy quantification estimating the additional value the acquirer can create through the combination.

Synergy quantification is one of the most consequential and most frequently overstated parts of the buy-side investment banking M&A process.

A strategic acquirer might model 50 million dollars per year in cost savings from eliminating redundant functions and consolidating suppliers.

If those savings are used to justify paying a premium over the target’s standalone valuation, the acquirer must actually deliver them after closing or the deal destroys value.

Deal structuring addresses whether to pursue a stock purchase or asset purchase, what mix of cash and debt to use in financing, and whether earnout provisions are appropriate to bridge a price gap between buyer and seller.

The bank advises on the optimal structure balancing tax efficiency, risk allocation, and seller preferences.

Financing Arrangement

Financing arrangement is one of the most operationally intensive parts of M&A in investment banking on the buy-side.

The bank arranges debt financing for acquisitions requiring leverage, a function that directly overlaps with the skills covered in acquisition financing and leveraged buyout modeling.

This includes preparing bank presentations for lenders, negotiating debt terms, and syndicating loans across multiple lenders to distribute risk.

For large transactions, the bank may underwrite bridge financing, providing the acquirer with a commitment of funds before permanent financing is arranged.

Bridge financing gives the acquirer certainty of funds at signing, which strengthens its negotiating position with the seller.

When the acquirer uses stock as consideration, the bank coordinates equity financing and manages the market implications of issuing new shares.

Negotiation Support and Due Diligence Coordination

Throughout negotiations, the buy-side bank advises on tactics, evaluates counteroffers, and helps the acquirer understand which deal points to contest and which to concede.

The bank also serves as coordinator across all external advisors, including the legal team, accounting firm, and any specialist consultants engaged for technical due diligence.

Weekly coordination calls align workstreams and maintain deal momentum.

A deal with five or six external advisor teams running parallel workstreams, without a central coordinator, quickly produces conflicting timelines and missed dependencies.

The bank identifies deal-breaking issues early in the process, allowing the acquirer to address them proactively rather than discovering problems at or after signing.

Section 3: Case Study: Dell Acquisition of EMC

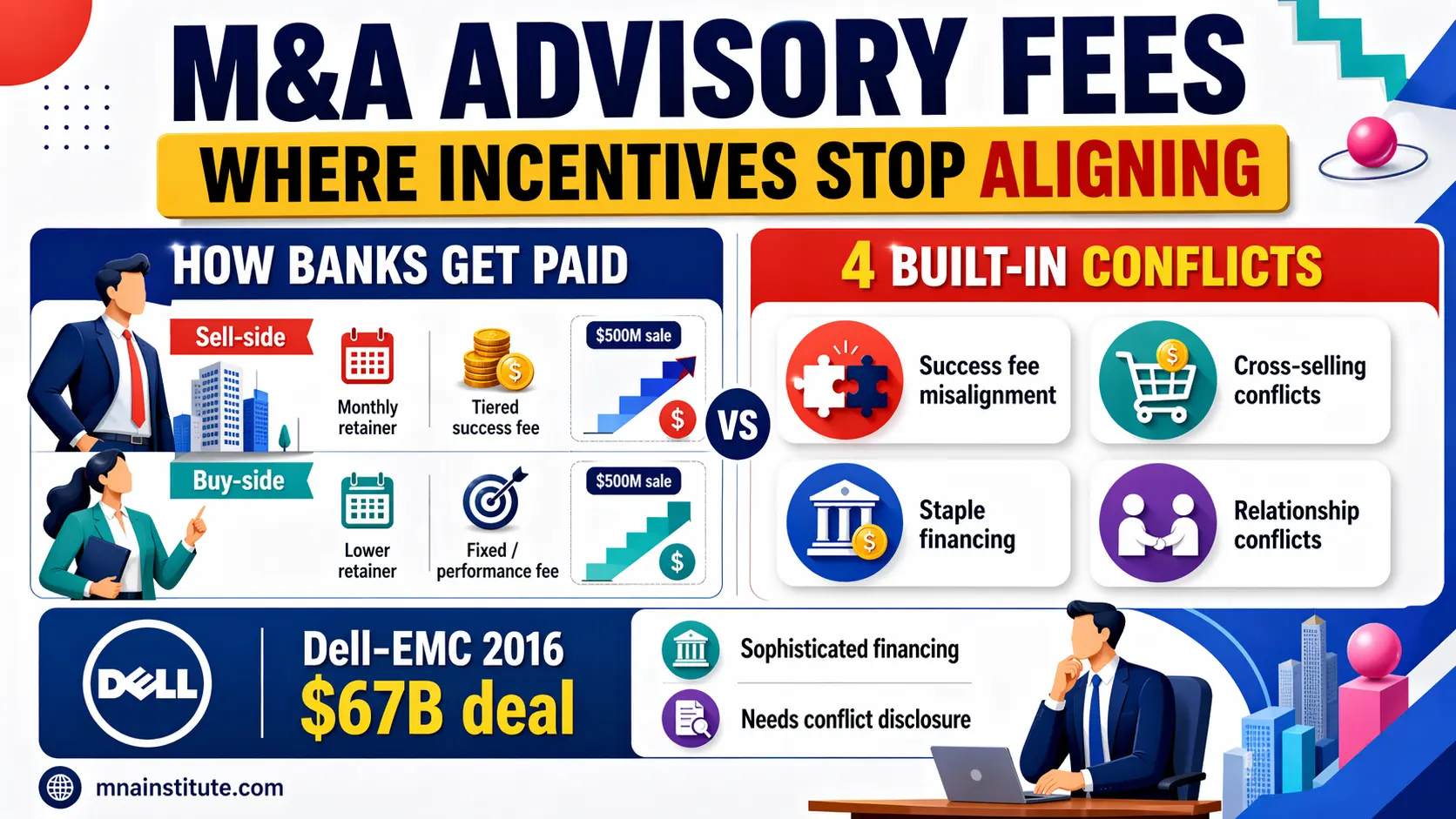

The 2016 acquisition of EMC Corporation by Dell Technologies illustrates what complex buy-side M&A in investment banking looks like in practice.

This case is one of the clearest examples of how M&A in investment banking extends well beyond advisory into financial engineering and cross-workstream coordination.

Dell completed the acquisition for approximately 67 billion dollars, making it one of the largest technology M&A transactions in history at the time.

JPMorgan served as the primary buy-side advisor.

EMC was not a straightforward target.

The company held a majority stake in VMware, a publicly traded virtualization software company, which complicated valuation significantly.

VMware had its own share price, its own shareholder base, and its own strategic value distinct from EMC’s core storage hardware business.

JPMorgan’s valuation work had to assess EMC’s standalone business, quantify the implied value of the VMware stake, and model what Dell could extract from the combined entity.

The financing structure was equally complex.

The transaction combined several funding layers: senior secured debt, unsecured notes, equity contributions from Dell’s existing investors, and a VMware tracking stock.

The tracking stock was an unconventional instrument designed to give former EMC shareholders economic exposure to VMware’s performance without actually selling VMware.

This structure allowed Dell to preserve VMware’s standalone listing while completing the broader acquisition of EMC.

JPMorgan coordinated due diligence across EMC’s diverse portfolio of business units including storage hardware, data protection, cloud infrastructure, and the VMware stake.

Each unit required separate diligence workstreams with different technical and financial expertise.

The Dell-EMC transaction demonstrates that buy-side investment banking M&A process is not limited to finding targets and arranging loans.

In complex deals, the bank must simultaneously serve as financial architect, valuation analyst, financing arranger, and cross-workstream coordinator.

Section 4: M&A Advisory Fee Structures and Engagement Models

Understanding M&A advisory fees is one of the most practical skills any executive or dealmaker working in mergers and acquisitions investment banking should develop.

M&A advisory fees are not standardized, and the gap between what different clients pay for equivalent services can be substantial.

Fee structures directly shape advisor incentives, and incentives determine behavior.

Sell-Side M&A Advisory Fees

Sell-side mandates typically combine two fee components: a monthly retainer and a success fee.

The monthly retainer compensates the bank for work done before a deal closes, including preparing the teaser and Information Memorandum, identifying buyers, running the data room, and managing the auction process.

Retainers typically range from tens of thousands to several hundred thousand dollars per month depending on deal size and complexity.

The success fee is calculated as a percentage of total transaction value, structured in tiers.

The classic starting point was the Lehman Formula, which charged 5% on the first million dollars of deal value, 4% on the second million, 3% on the third, 2% on the fourth, and 1% on everything above five million.

The Lehman Formula was designed for an era of smaller deals and is rarely used as written today.

Modern sell-side M&A advisory fees use custom tiered schedules negotiated at the time of engagement.

For a hypothetical sale of a company at 500 million dollars, the success fee might be structured as 1% on the first 100 million, 0.75% on the next 150 million, and 0.5% on the remaining 250 million.

That produces a total success fee of 1 million plus 1.125 million plus 1.25 million, or 3.375 million dollars.

The exact percentages depend on deal size, sector, deal complexity, and the competitive dynamics between banks pitching for the mandate.

Buy-Side M&A Advisory Fees

Buy-side M&A advisory fees follow a similar structure but at lower levels.

Monthly retainers on buy-side mandates tend to be lower than sell-side retainers because the bank does not need to prepare marketing materials or manage a multi-party auction.

Success fees on buy-side mandates are typically smaller percentages of deal value compared to sell-side, reflecting the different scope of work.

Some buy-side mandates replace percentage-based success fees with fixed fees agreed at the outset.

Performance bonuses may be added to reward the advisor for achieving specific outcomes, such as negotiating a price below the initial asking price or securing favorable indemnification terms.

Full-Service Versus Limited Mandates

Engagement structure is a separate decision from fee structure, and it shapes how much control the client retains over the M&A in investment banking process.

A full-service mandate means the bank manages the entire process with minimal client involvement, selects all other external advisors, and takes responsibility for coordination across legal, accounting, and specialist workstreams.

This model suits sellers or acquirers who lack internal M&A experience or the bandwidth to manage a deal alongside their operating responsibilities.

The trade-off is reduced client oversight.

When the bank selects the lawyers and accountants, the client has less direct visibility into those relationships.

A limited mandate means the client manages the overall process and retains the bank for specific services only, such as valuation, buyer identification, or financing arrangement.

This model suits companies with experienced internal M&A teams that want advisory support in specific areas without ceding full process control.

Fees are lower under a limited mandate, but the client must provide more internal resources to fill the gaps.

Section 5: 4 Conflict Types in M&A in Investment Banking

M&A in investment banking generates structural conflicts that exist regardless of how ethical or capable the individual bankers involved may be.

These conflicts are features of the mergers and acquisitions investment banking fee model, not exceptions to it.

These conflicts arise from how banks earn revenue, which clients they serve across multiple deals, and how they structure their advisory relationships.

Every company engaging an investment bank for mergers and acquisitions should understand these four conflict types before signing an engagement letter.

1. Success Fee Misalignment

The first and most pervasive conflict in M&A in investment banking is success fee misalignment.

Success fees create a direct incentive to close deals regardless of whether the price is adequate.

A bank earns its fee when a transaction closes, not when it closes at the optimal price.

On the sell-side, this conflict means the bank may pressure sellers to accept offers that are acceptable rather than holding out for a higher price, particularly if deal momentum is slowing or a competing auction process is under time pressure.

On the buy-side, a success fee structure can discourage the bank from raising concerns that might kill the deal, even if those concerns are legitimate.

Clients on both sides should independently validate bank valuation recommendations against market data and maintain internal financial capability to challenge the bank’s analysis.

2. Cross-Selling and Relationship Conflicts

Investment banks serve many clients across many deals simultaneously.

A bank advising a seller in one transaction may have a long-standing relationship with the buyer in another, creating a conflict between maximizing value for the current sell-side client and preserving the bank’s relationship with a frequent buyer.

Cross-selling conflicts arise when a bank advising a seller steers buyers toward the bank’s own lending desk, where the bank earns additional financing fees on top of its advisory fee.

Clients should require full disclosure of all bank relationships with counterparties in the transaction before the engagement letter is signed.

3. Staple Financing Conflicts

Staple financing refers to an arrangement where the sell-side bank offers pre-approved debt financing to potential buyers as part of the sale process.

The name comes from the practice of attaching a financing term sheet to the auction materials distributed to buyers.

The conflict is direct: the bank simultaneously advises the seller and provides debt to the buyer.

This creates an incentive for the bank to favor buyers who are most likely to use the stapled financing, even if those buyers are not the highest bidders.

Buyers participating in a process where staple financing is offered should obtain independent financing quotes rather than accepting the stapled package as the default.

Independent financing may be cheaper, and the process of obtaining it removes the bank’s ability to influence buyer selection through financing dependency.

4. Mitigating These Conflicts

None of these conflicts eliminate the value of working with an experienced investment bank.

They do require clients to engage with active oversight rather than passive reliance.

Engagement letters should require the bank to disclose all material conflicts before and during the engagement.

Clients should obtain valuation opinions from at least one independent source rather than relying solely on the advising bank’s analysis.

Fee structures can include clawback provisions that recover part of the success fee if the deal unwinds within a defined period after closing.

Boards approving transactions should ask probing questions about the bank’s recommendations rather than accepting them as independent validation.

The most effective protection is a strong internal team that understands the investment banking M&A process well enough to identify when the bank’s advice is shaped by its own incentives rather than the client’s interests.

This is the structural answer to the conflicts embedded in M&A in investment banking: informed clients produce better advisory relationships than trusting ones.

🏦 Understanding the Full Investment Banking M&A Process

- For readers using this topic as an entry point, the Mergers and Acquisitions Online Course provides the broadest map of the full transaction sequence from strategy through closing and integration.

- The banker led front end of buyer outreach and target prioritization sits close to M&A Deal Sourcing & Pipeline Management.

- The workstream coordination that follows management access and data room review maps naturally into M&A Due Diligence: CDD, FDD, LDD, & HRDD.

- Where leverage, bridge commitments, and debt capacity change the bid, the technical layer is developed further in Acquisition Financing & LBO Modelling Course.

- Negotiation around purchase price, structure, and protections connects closely with M&A Deal Negotiation Mastery and then with final agreement terms in Stock Purchase Agreement Mastery.

- Post close execution issues touched by the banker during diligence and signing ultimately continue into Post-Merger Intergration and Value-Up Strategy.

Sources

- Dell Technologies combination announcement on completion of EMC acquisition

- EMC proxy statement and prospectus describing the VMware tracking stock and merger consideration

- FINRA Rule 5150 on fairness opinions and related conflict disclosures