Pension Due Diligence Guide for Successful M&A Deals

Guide to Pension Due Diligence in M&A

When engaging in mergers and acquisitions (M&A), pension due diligence (PDD) is a critical yet often overlooked aspect that can have a profound impact on the financial health of the acquiring company. A thorough examination of pension liabilities can uncover hidden financial risks that may outweigh the benefits of the deal. In this blog post, we’ll explore why pension due diligence is so important, the different types of pension schemes to consider, how to conduct a comprehensive PDD, and the consequences of neglecting this crucial process.

Why Pension Due Diligence is Crucial in M&A

Pension schemes often represent long-term financial commitments that extend well beyond the immediate timeline of an M&A transaction. As companies acquire or merge with others, they may inherit pension-related liabilities that have the potential to significantly impact future cash flows. Understanding these liabilities is essential for determining the overall value of the deal.

Key Risks and Challenges

During the pension due diligence process, several key risks and challenges must be addressed:

-

Long-Term Liabilities: Pension obligations, especially in defined benefit schemes, extend years or even decades into the future. The acquiring company must accurately forecast these expenses, as they represent ongoing financial commitments to former employees.

-

Exposure to Market Factors: Pension schemes are subject to external economic factors like inflation, interest rates, and market performance. Fluctuations in these variables can dramatically impact the funding levels of pension schemes, resulting in unexpected liabilities for the acquiring company.

-

Hidden Liabilities: Sellers may present an overly optimistic view of the pension scheme’s health, concealing potential issues in the fine print. Unreported pension guarantees or promises made to high-level executives can create financial “black holes” for the buyer, posing significant risks if not uncovered early in the due diligence process.

Understanding the Regulatory Environment

Pension due diligence is not just about understanding liabilities but also ensuring compliance with relevant regulations and accounting standards. Pension accounting operates within a complex web of international and local regulations that demand careful scrutiny. The following factors must be taken into account:

Global Variations

Pension regulations and accounting practices vary significantly across jurisdictions. When dealing with multinational transactions, it is vital to scrutinize local pension rules to ensure compliance. A lack of understanding of jurisdictional differences can lead to incorrect reporting and future legal challenges.

International Accounting Standards

Frameworks such as IAS 19 govern the recognition, measurement, and disclosure of pension obligations. These standards affect how pension assets and liabilities are reported, directly influencing a company’s financial health. Buyers need to be well-versed in these frameworks to accurately assess the financial impact of pension schemes.

Impact of Accounting Standards

The way pension obligations are accounted for can significantly affect the reported financial status of a company. For instance, certain accounting standards may allow companies to defer recognizing certain liabilities, giving a misleading impression of the company’s financial health. Thorough pension due diligence ensures that these issues are uncovered and addressed before the deal is finalized.

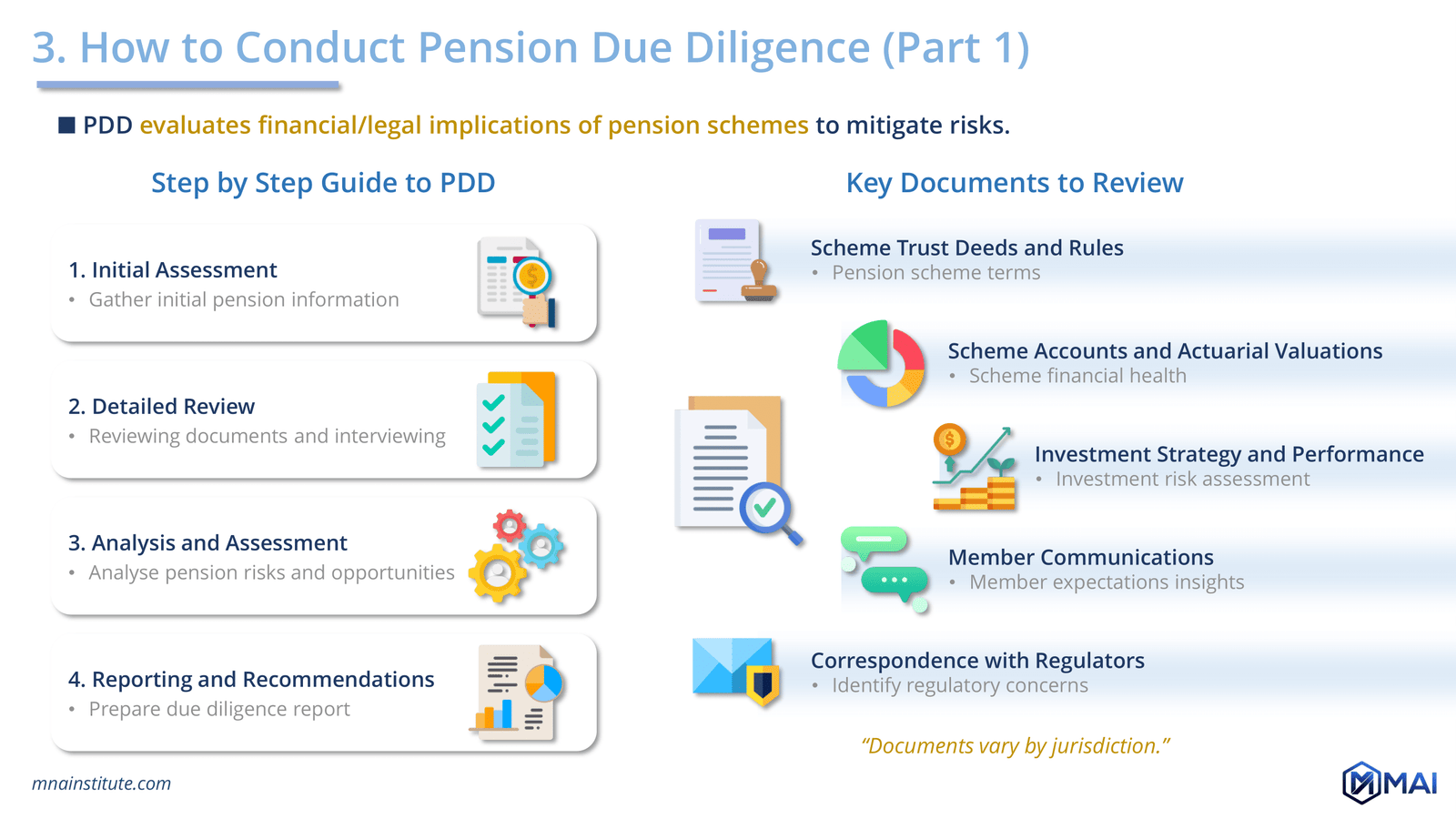

How to Conduct Pension Due Diligence

A comprehensive pension due diligence process can be broken down into several key steps. Each step is essential for identifying and mitigating potential risks and ensuring a smooth transition post-acquisition.

1. Initial Assessment

The first step in pension due diligence is to gather high-level information about the target company’s pension schemes. This includes understanding the type of pension scheme (e.g., defined benefit or defined contribution), the size of the membership, and the funding status of the scheme.

2. Detailed Review

After the initial assessment, a more detailed review is conducted. This involves reviewing critical documents such as scheme trust deeds, rules, scheme accounts, and actuarial valuations. Interviews with key stakeholders, including scheme trustees and the management team, are also an essential part of this step.

3. Analysis and Assessment

Once the necessary information has been gathered, the next step is to analyze the data to identify potential risks and opportunities. This involves assessing the funding levels of the pension scheme, reviewing any hidden liabilities, and evaluating the company’s ability to meet its future pension obligations.

4. Reporting and Recommendations

The final step in the due diligence process is to prepare a report summarizing the findings. This report should provide clear recommendations for mitigating any identified risks and outline the financial implications of the pension liabilities.

Key Documents to Review

- Scheme Trust Deeds and Rules: These documents set out the terms and conditions of the pension scheme, including eligibility criteria, benefits payable, and funding arrangements.

- Scheme Accounts and Actuarial Valuations: These provide financial information about the scheme, including its assets and liabilities, and its funding status.

- Investment Strategy and Performance: This information will help assess the risks and possible returns of the scheme’s investments.

- Member Communications: This offers insights into scheme members’ expectations and concerns.

- Correspondence with Regulators: This can help to identify any regulatory issues or concerns.

Types of Pension Schemes in M&A and Their Implications

Different types of pension schemes present varying levels of risk and complexity in M&A transactions. Understanding these distinctions is crucial for conducting effective pension due diligence.

Defined Benefit (DB) Schemes

Defined benefit schemes guarantee employees a specific retirement income based on factors such as final salary and years of service. These schemes present significant risks for buyers because the company is responsible for funding the promised payouts, regardless of market performance.

Due Diligence Focus: Buyers must assess the funding levels of DB schemes and determine whether any hidden costs could affect the company in the long term. Actuarial valuations are essential to forecast future liabilities and assess the financial sustainability of the scheme.

Defined Contribution (DC) Schemes

Defined contribution schemes, also known as money purchase schemes, place the investment risk on the employee. The company contributes to an individual savings account, and the retirement income depends on the investment performance of those contributions.

Due Diligence Focus: While DC schemes present lower risks for buyers, due diligence should focus on reviewing the investment strategies, fees, and ongoing contribution obligations. Ensuring that the buyer will continue contributing to the scheme is crucial for employee retention and morale.

Hybrid Schemes

Hybrid schemes combine elements of both DB and DC schemes, making them more complex to evaluate. These schemes offer a mix of guaranteed income and market-based returns, creating unique risks for both the company and the employees.

Due Diligence Focus: A thorough evaluation of both the DB and DC components is necessary, with a particular focus on the long-term funding requirements of the DB portion and the investment performance of the DC portion.

Executive and Unapproved Schemes

These schemes are designed for high-income earners and may involve special tax considerations or additional benefits. They often require specialized due diligence to uncover potential hidden costs and liabilities.

Due Diligence Focus: Understanding the tax implications and potential costs of executive schemes is essential. Buyers may also want to evaluate whether these schemes should be continued or altered post-acquisition.

Due Diligence for Different Transaction Scenarios

The type of transaction also affects the pension due diligence process. Each scenario presents unique considerations that must be addressed.

Buying an Entire Company

When acquiring an entire company, detailed financial checks are necessary to fully understand the condition of the pension fund. Buyers should also review employee agreements that may impact pension costs, especially if they plan to close or restructure the pension scheme.

Buying a Subsidiary

In subsidiary acquisitions, agreeing on a fair price for transferring pension funds is crucial. Understanding both your own pension rules and those of the target company is key to successful negotiations.

Buying Assets Only

When acquiring only the assets of a company, setting up a new pension plan for the acquired employees can boost morale and loyalty. Buyers should consider whether it is better to integrate the new employees into an existing scheme or establish a separate pension plan.

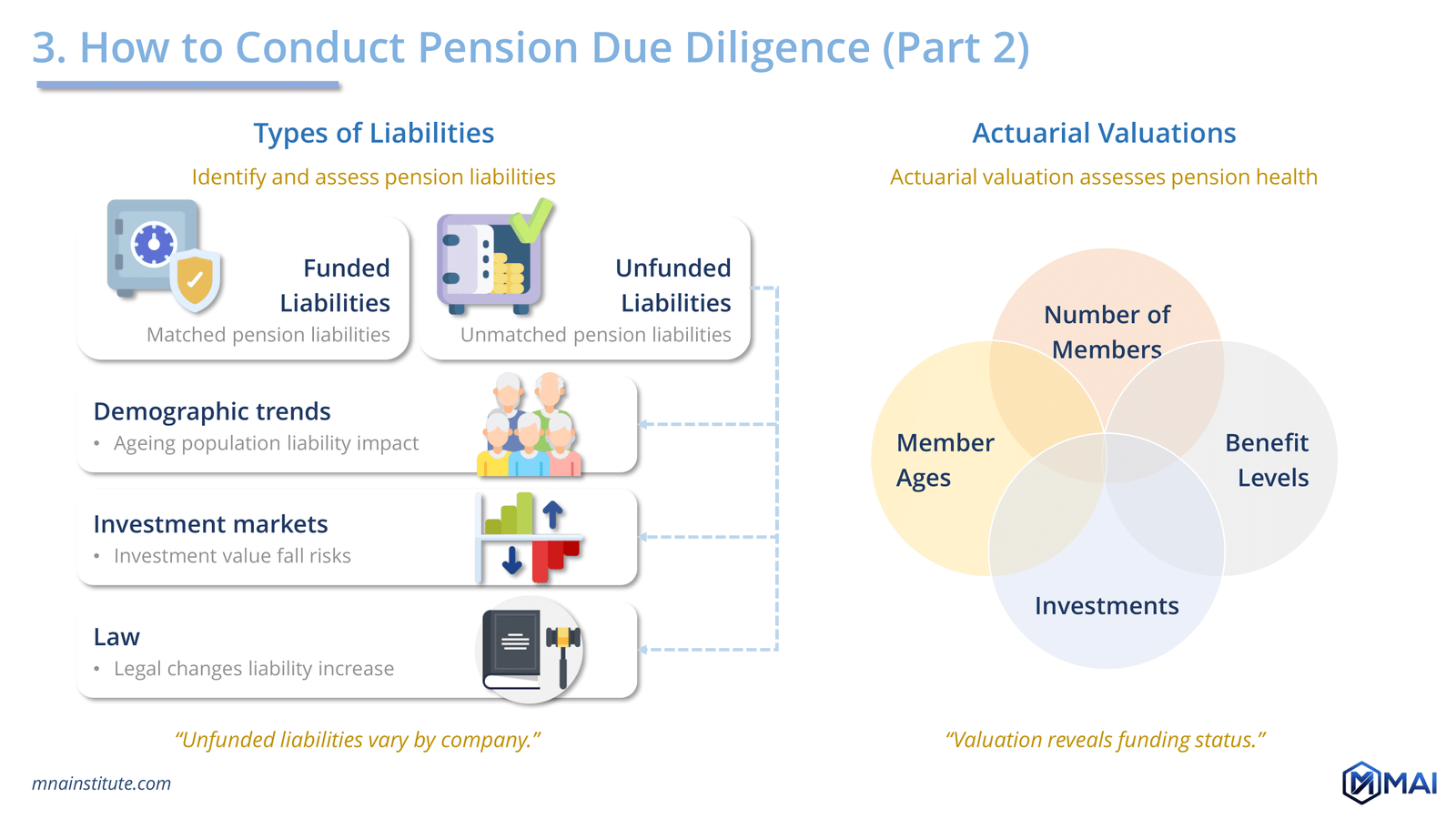

Identifying and Assessing Liabilities in PDD

A critical aspect of pension due diligence is identifying and assessing the target company’s pension liabilities. These liabilities can be categorized as funded or unfunded, with significant implications for the buyer.

Funded Liabilities

Funded liabilities are matched by assets, such as investments held by the pension scheme. These liabilities are generally less risky for the buyer, as the pension scheme has the financial resources to meet its obligations.

Unfunded Liabilities

Unfunded liabilities, on the other hand, have not been matched by assets and will need to be met by the employer in the future. Several factors can contribute to unfunded liabilities, including demographic changes, investment market fluctuations, and changes in pension laws.

Accurately determining the extent of a scheme’s funding shortfall or surplus requires professional actuarial valuations. These valuations help predict how much the company will need to contribute in the future, providing essential information for the buyer.

The Role of Actuarial Valuations in PDD

An actuarial valuation is essentially a financial health check for a pension scheme. Conducted by actuaries, these valuations consider several factors, including:

- Number of Members: How many individuals will receive benefits from the scheme?

- Member Ages: When will benefits need to be paid out, and for how long?

- Benefit Levels: How generous are the promised pension payments?

- Investments: How well are the pension scheme’s assets expected to perform in the future?

The valuation reveals whether the scheme is overfunded (assets exceed obligations) or underfunded (a shortfall exists). This information is crucial for buyers, as it directly impacts their future financial obligations.

Addressing Pension Issues in Mergers & Acquisitions

Once pension issues are identified through the due diligence process, the buyer must take steps to address them. This may involve negotiating terms with the seller, addressing funding deficits, or integrating pension schemes post-acquisition.

Negotiating Terms

During the deal negotiations, the buyer should carefully craft warranties and indemnities related to pensions. These are promises from the seller to cover specific pension-related costs. Obtaining these indemnities is crucial for protecting the buyer from unexpected liabilities.

Addressing Funding Deficits

If the pension scheme is underfunded, the buyer has several options:

- Seller Contributions: The contract can require the seller to cover any funding shortfalls, protecting the buyer financially.

- Insurance Review: If the pension scheme is insured, the buyer should carefully review the insurance policy to ensure it can cover the full costs. In some cases, the buyer may still want an indemnity from the seller, though sellers often resist this.

Surplus Scenarios

If the pension scheme has a surplus, the buyer should not assume that this represents a financial gain. Regulations often require that surplus funds be used to improve benefits rather than being retained as profit. A thorough actuarial valuation can reveal whether any financial gain is possible.

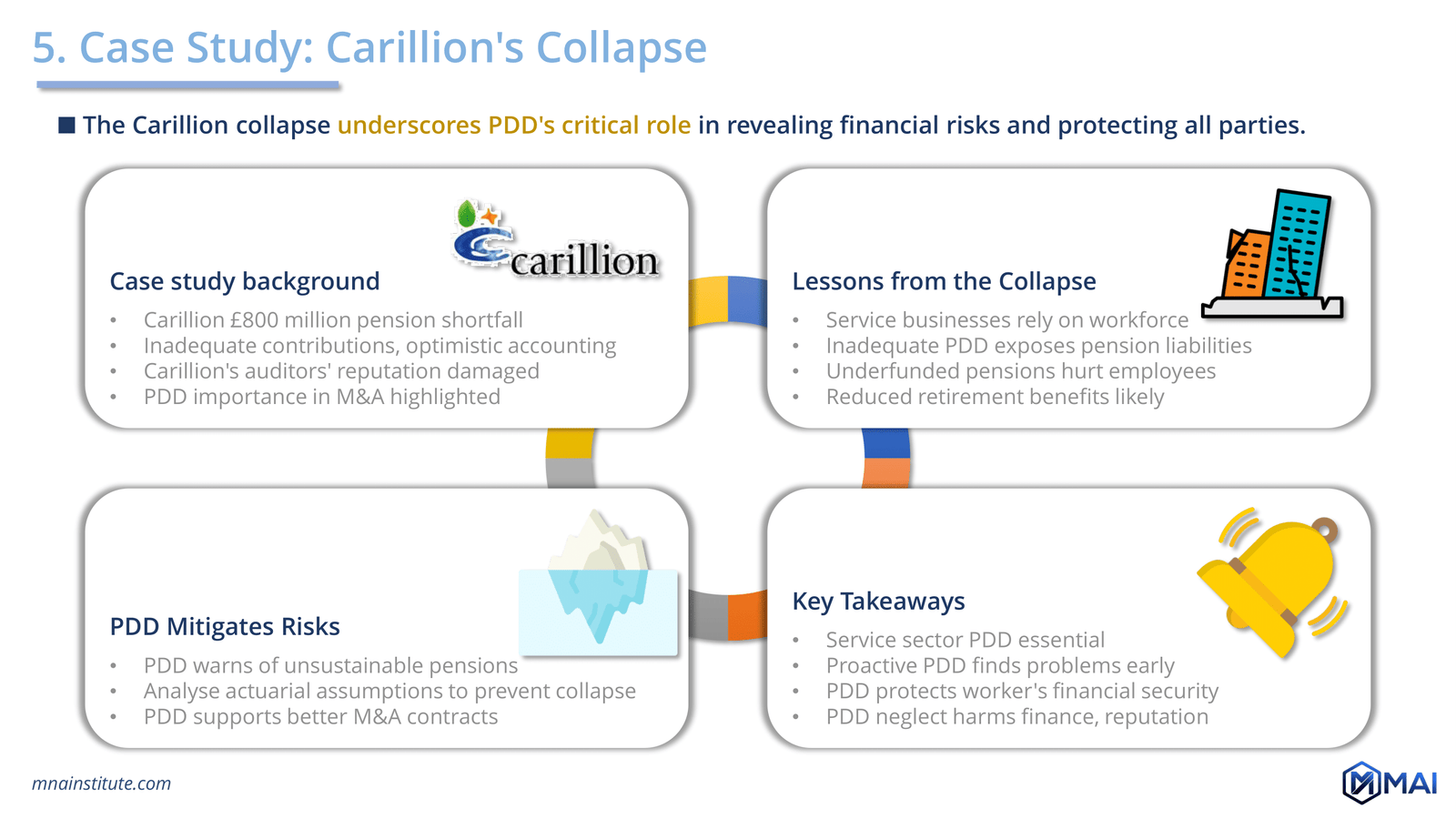

Case Study: Carillion’s Collapse and Pension Due Diligence

One of the most notable examples of inadequate pension due diligence is the collapse of UK construction giant Carillion in 2018. Carillion’s pension schemes were underfunded by £800 million, leading to a financial shortfall that contributed to the company’s downfall.

Lessons from Carillion

- Hidden Liabilities: Service-oriented companies often have large pension obligations. Without proper PDD, these liabilities can remain hidden until it is too late.

- Employee Impact: The collapse of Carillion left employees with severely reduced retirement benefits, highlighting the importance of thorough pension due diligence to protect workers.

- Reputational Risk: Carillion’s auditors and management faced significant reputational damage as a result of the pension shortfall. This case underscores the importance of taking PDD seriously to avoid financial and reputational harm.

How Pension Due Diligence Would Have Helped

- Early Risk Detection: Thorough PDD might have warned Carillion’s management or investors about the unsustainable pension scheme, allowing them to take action.

- Actuarial Oversight: A thorough analysis of actuarial assumptions would have highlighted the scheme’s instability, enabling preventative measures.

- Informed Negotiations: Robust PDD supports better contract terms and indemnities when acquiring companies with defined benefit pensions, mitigating financial risks.

Conclusion: Don’t Overlook Pension Due Diligence

Pension due diligence is a critical component of any M&A transaction, especially when dealing with defined benefit schemes or complex pension structures. By conducting thorough due diligence, buyers can identify hidden liabilities, mitigate risks, and ensure a smooth transition post-acquisition. Ignoring pension due diligence, as demonstrated by cases like Carillion, can lead to significant financial and reputational damage, making it an essential part of any responsible M&A strategy.

Pension due diligence is not just a box to tick during an acquisition—it’s a vital process that protects both the buyer’s financial interests and the well-being of employees relying on pension schemes.