M&A Team Structure: 5 Powerful Rules for Building an Internal Deal Team

Learn M&A team structure, corporate development team roles, and how to build an internal M&A team with clear responsibilities.

A mid-sized industrial company announces an acquisition.

The target is well-chosen, the price is fair, and the strategic rationale is clear.

Six months after closing, synergy capture is behind schedule, three key managers from the target have resigned, and the finance team is still reconciling two incompatible accounting systems.

The problem was not the deal itself.

The problem was that the company had no functioning M&A team structure before the deal was signed.

Every stage of a mergers and acquisitions transaction depends on a coherent internal team that knows its roles before the pressure starts.

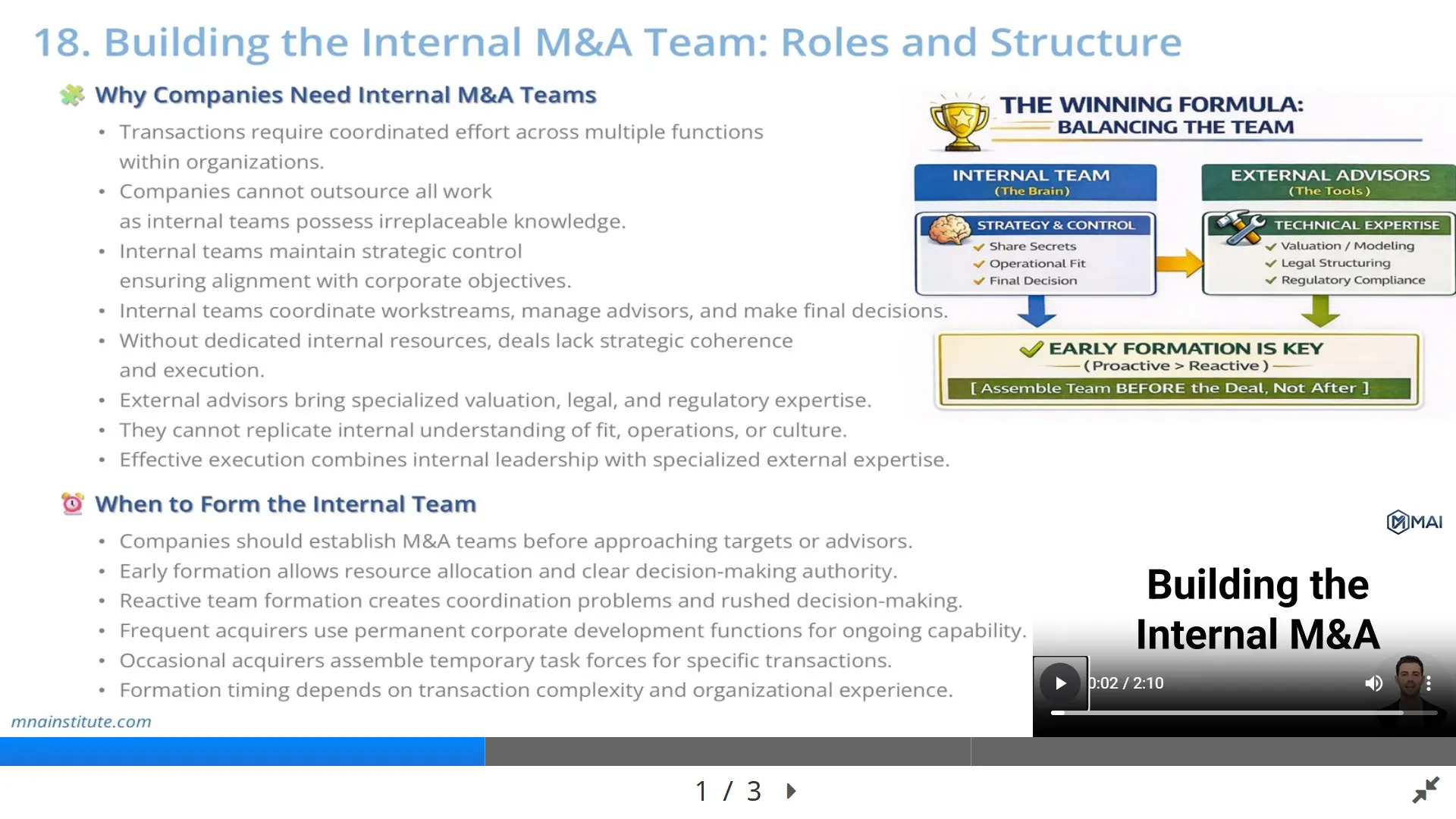

External advisors bring indispensable technical expertise, but they cannot replicate internal knowledge of corporate strategy, operational constraints, or cultural dynamics.

The most effective M&A team structure combines internal strategic ownership with external specialized support, and this article explains exactly how to build it.

Section 1: When to Form the Internal M&A Team

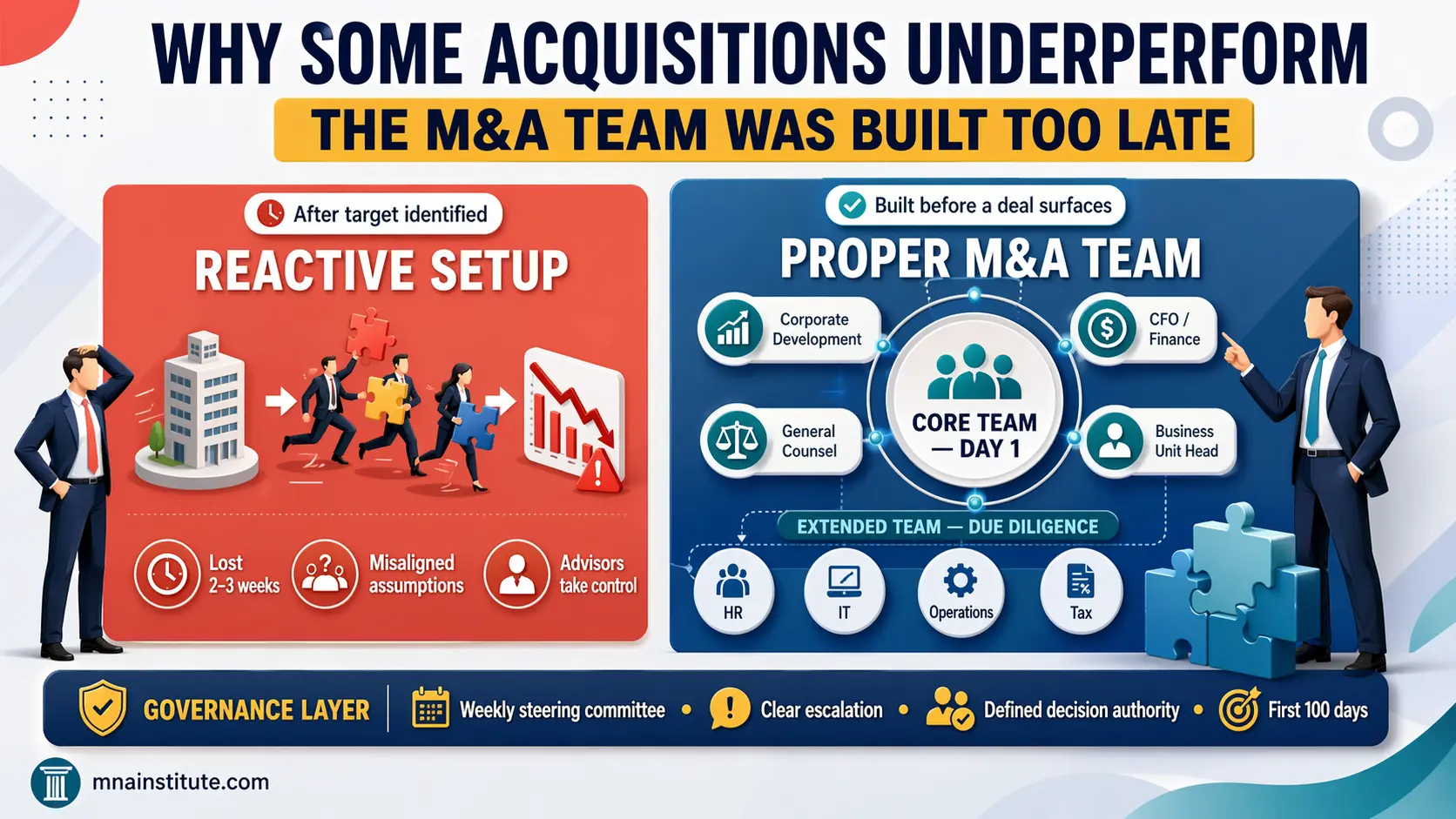

The timing of M&A team formation is one of the most consequential decisions a company makes in the deal process.

Most companies get it wrong by treating team assembly as a reaction to an opportunity rather than a standing capability.

When a potential target surfaces and the company scrambles to identify who leads due diligence and who approves the valuation, weeks of coordination time are already lost.

A sound M&A team structure is established before approaching targets or engaging advisors, not after a deal opportunity emerges.

Early formation creates three structural advantages.

First, resource allocation can be planned rather than improvised, ensuring the right people are available at each deal stage without pulling senior leaders from operating responsibilities at the last moment.

Second, clear decision-making authority is established before the pressure of a live transaction creates ambiguity about who can approve what.

Third, capability gaps become visible in advance, allowing the company to identify where external advisors are genuinely needed versus where internal expertise can lead.

Permanent Functions Versus Transaction Task Forces

The right model depends on acquisition frequency and organizational experience.

Companies that pursue multiple acquisitions annually benefit from a permanent corporate development team that maintains ongoing deal sourcing, relationship management, and M&A process capability.

A dedicated corporate development team running a live deal sourcing pipeline can identify and qualify targets systematically rather than reacting to inbound approaches from advisors.

Companies that make occasional acquisitions, perhaps one transaction every two or three years, typically assemble a temporary task force for each deal and disband it after integration is complete.

This model costs less in steady-state but requires careful design each time to ensure that roles, authorities, and processes are rebuilt without starting from zero.

A practical example illustrates the difference.

A large pharmaceutical company with a stated strategy of acquiring oncology pipeline assets needs a permanent corporate development team continuously evaluating clinical-stage companies.

A family-owned manufacturing group that acquires a competitor once a decade assembles a task force led by the CFO when the opportunity arises.

Both approaches can work, but only if the M&A team structure is defined before the deal clock starts running.

Learning how to build an internal M&A team before a live deal surfaces is the single most underrated preparation step in corporate M&A.

Section 2: Core M&A Team Roles and Responsibilities in a Winning M&A Team Structure

The core M&A team structure consists of four functions that must be represented in every transaction regardless of deal size or complexity.

Understanding M&A team roles and responsibilities at this level is the foundation of any effective M&A team structure.

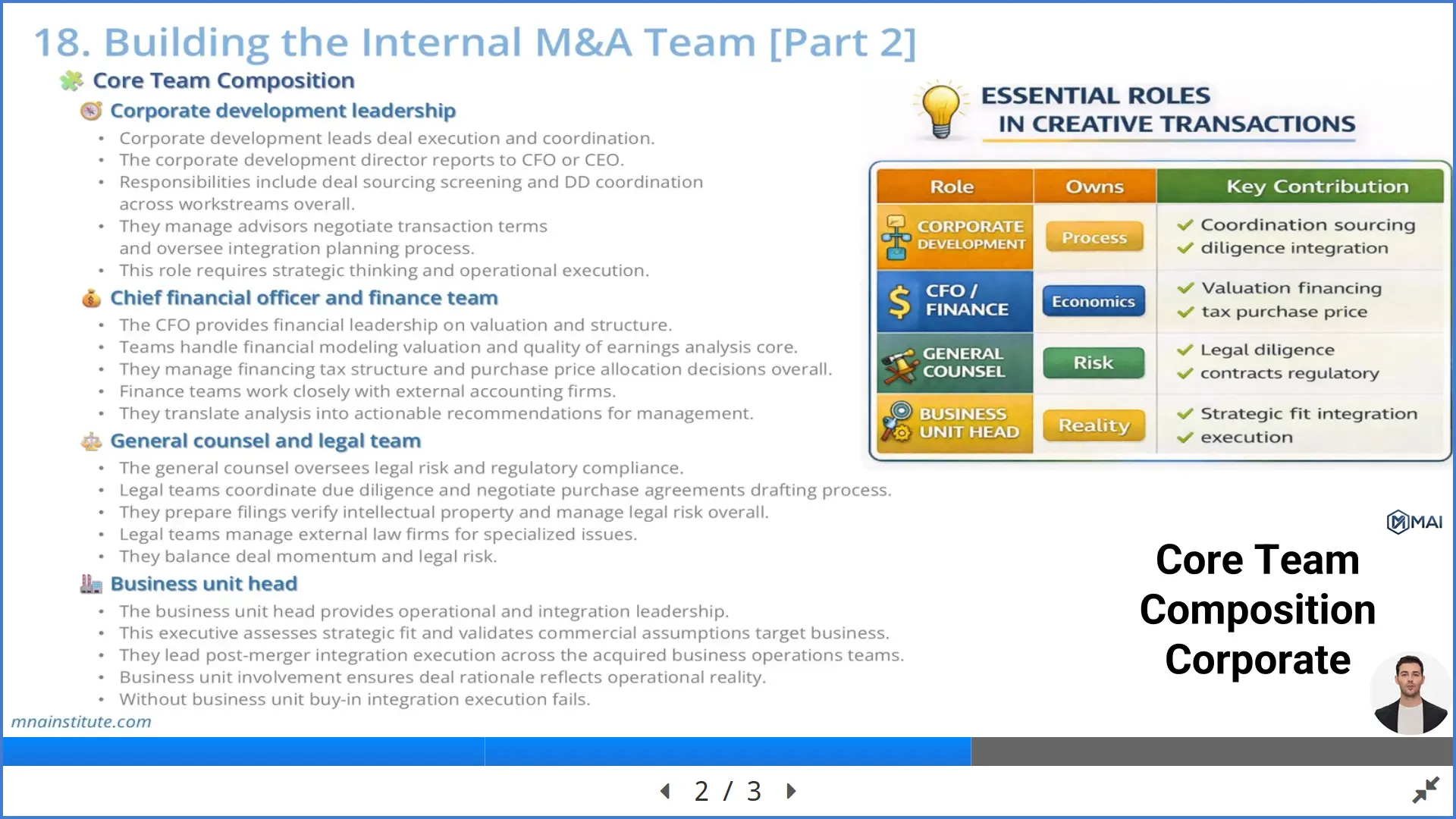

Corporate Development Leadership

The corporate development lead is the operational center of any M&A team structure.

This person coordinates all workstreams, manages the overall deal timeline, serves as the primary contact for external advisors, and translates strategic objectives into daily execution priorities.

The corporate development director typically reports to the CFO or the CEO, depending on the materiality of the transaction and the organizational structure.

For a company where M&A is a core growth driver, the corporate development lead may report directly to the CEO to ensure strategic decisions receive immediate executive attention.

The responsibilities of the corporate development team span the full deal lifecycle.

During origination, this function drives target screening and initial outreach.

During diligence, it coordinates parallel workstreams covering financial, legal, commercial, and operational due diligence while ensuring findings are synthesized into a coherent risk picture.

After signing, the corporate development lead oversees integration planning until a dedicated integration team takes over.

Chief Financial Officer and the Finance Team

The CFO serves as the senior financial decision-maker throughout the transaction and often acts as deal sponsor for mid-market acquisitions.

Finance team responsibilities within the M&A team structure cover financial modeling and valuation, quality of earnings assessment, financing arrangements, tax structure analysis, and purchase price allocation.

Quality of earnings deserves specific attention because external accounting firms typically conduct the formal analysis, but the internal finance team must understand and challenge the adjustments being made.

Without internal financial fluency, the company cannot evaluate whether a normalized EBITDA figure reflects the target’s true earnings power.

The financing decision, whether to use cash, debt, equity, or a combination, directly shapes the deal structure and affects returns in acquisition financing and leveraged buyout contexts.

Tax structure is another area where internal finance leadership is essential.

The choice between a stock purchase and an asset purchase has significant tax consequences for both buyer and seller, and the internal team must understand these mechanics to evaluate trade-offs during negotiation.

General Counsel and the Legal Team

The general counsel oversees all legal dimensions of the transaction and manages the interface with external law firms.

Internal legal teams rarely have the bandwidth to handle every legal workstream independently.

The practical division is that the general counsel maintains strategic oversight and makes decisions on risk tolerance, while external firms execute detailed work on regulatory filings, IP transfers, and SPA drafting.

The negotiation of the stock purchase agreement is one of the most consequential legal workstreams in any acquisition, covering representations and warranties, indemnification provisions, and price adjustment mechanisms.

The general counsel’s role is to ensure that legal risk management does not slow deal momentum unnecessarily.

Every deal carries legal risks, and the question is which risks are acceptable, which can be mitigated through deal structure, and which require price adjustments or specific deal protections.

Business Unit Head

The business unit head is the operational owner of the deal rationale and the single most important member of the internal M&A team for integration success.

This executive assesses strategic fit at the product and market level, validates the commercial assumptions underlying the financial model, and leads post-merger integration once the transaction closes.

A deal that makes sense on paper but lacks business unit ownership almost always struggles after closing.

The business unit head is the person accountable for delivering the synergies and growth assumptions that justified the acquisition price.

If they were not involved in building those assumptions, they have no stake in defending them when execution becomes difficult.

Business unit involvement during due diligence also surfaces commercial risks that financial analysis alone cannot identify.

A business unit leader visiting a target’s facility will notice capacity constraints, workforce skill gaps, or customer concentration issues that do not appear on a balance sheet.

These findings feed directly into post-merger integration planning and shape which synergies are realistic within which timeframe.

Section 3: Extended Roles That Complete the Internal M&A Team Structure

The extended M&A team structure brings functional specialists whose input shapes due diligence quality and integration feasibility.

A common mistake is engaging these functions only after signing.

By that point, the deal price has been agreed and most structural decisions are locked.

Extending the M&A team structure to include these specialists during due diligence ensures that operational and functional risks are priced into the transaction before closing.

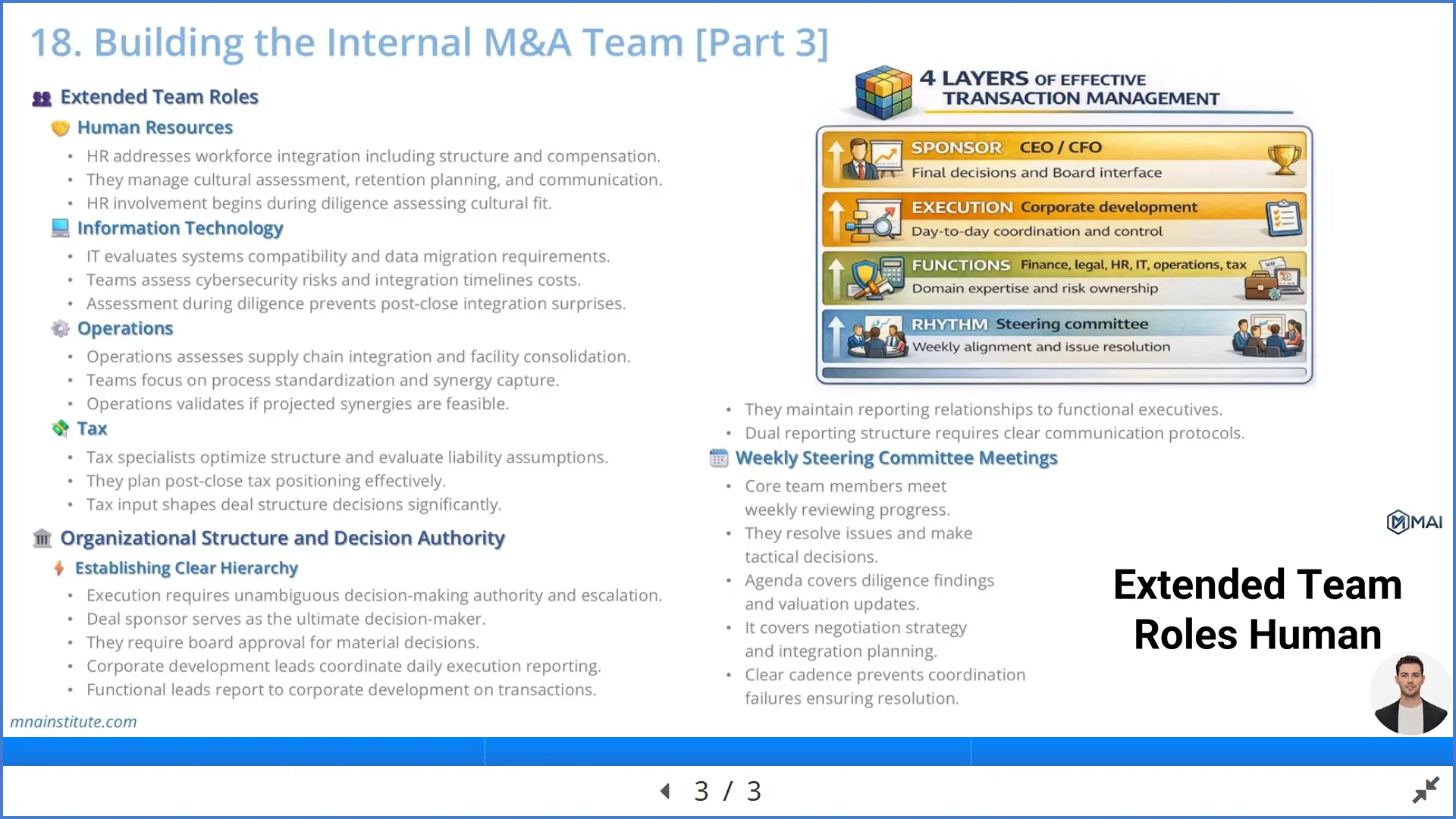

Human Resources

HR’s role in the M&A team structure begins during due diligence, not after integration starts.

The HR workstream covers cultural assessment, organizational structure design, compensation harmonization, key employee retention planning, and change management communication.

Cultural due diligence is one of the most frequently underestimated workstreams.

Two companies can have compatible financials and complementary products while having fundamentally different management styles and decision-making cultures.

When those differences are not surfaced pre-close, integration produces avoidable attrition of exactly the people the acquirer needed to retain.

Key employee retention planning should be completed before signing, identifying which individuals from the target organization are essential to value delivery and designing retention packages that address compensation gaps.

Information Technology

IT assessment during due diligence prevents post-close integration surprises that consume time and budget.

The IT workstream evaluates technology systems compatibility, data migration requirements, cybersecurity posture, and systems integration timeline and costs.

A company acquires a business running a legacy ERP system incompatible with its own platform.

If discovered after closing, the integration timeline extends by months and migration costs are absorbed from budgets sized for a simpler systems environment.

If IT due diligence surfaces this before signing, the acquirer can factor migration costs into the valuation model, adjust the purchase price, or build a longer integration timeline into the deal structure.

Cybersecurity assessment is now a standard component of IT diligence because the acquiring company inherits the target’s cybersecurity posture on the day of closing, including any vulnerabilities that were not disclosed.

Operations

The operations workstream validates whether projected synergies are operationally feasible.

Financial models regularly assume supply chain consolidation, facility rationalization, or procurement savings that look compelling on paper but require operational conditions the target does not meet.

Operations leaders often identify sequencing constraints that determine when synergies can realistically be captured.

A facility consolidation may generate significant annual savings, but if it requires regulatory approvals, equipment relocations, and workforce restructuring, the earliest realistic savings date may be two years after closing rather than six months as modeled.

Tax

Tax specialists shape structural decisions that cannot be easily reversed after closing.

The tax workstream covers transaction structure optimization, evaluation of tax liabilities being assumed, and post-close tax planning.

An asset purchase typically allows the acquirer to step up the tax basis of acquired assets to fair market value, which increases depreciation deductions and reduces taxable income over the life of the assets.

A stock purchase generally does not provide this step-up, which makes it less attractive from a tax perspective for the buyer, though sellers often prefer it because capital gains treatment is more favorable than ordinary income tax on asset sales.

In cross-border deals, the interaction between multiple tax regimes can materially affect the after-tax return on investment and must be modeled alongside the commercial assumptions.

Section 4: Governance and Decision Authority Within the M&A Team Structure

The M&A team structure is not only about who is in the room.

It is about who has the authority to make which decisions, who escalates to whom, and how the M&A team structure handles disagreement without stalling execution.

Ambiguous decision authority is one of the most consistent weaknesses in a poorly designed M&A team structure, forcing every contested issue up to the CEO level and creating decision fatigue.

Establishing a Clear Hierarchy

The deal sponsor, typically a C-suite executive such as the CEO or CFO, serves as the ultimate decision-maker and holds Board accountability for the transaction.

The corporate development lead reports to the deal sponsor and coordinates daily execution across all workstreams.

Functional leads for finance, legal, HR, and operations report to the corporate development lead on transaction matters while maintaining standard reporting relationships to their respective functional executives.

This dual reporting structure is a defining feature of a well-designed M&A team structure, and it works only when communication protocols are explicit.

Each functional lead must know which decisions they can make independently within their workstream, which require corporate development approval, and which require deal sponsor escalation.

Documenting these thresholds at the start of the process, before disagreements arise, prevents the ambiguity that stalls deals mid-execution.

A practical rule used in many corporate development functions: workstream-level decisions affecting scope and methodology within a function can be made by the functional lead.

Decisions that affect deal price, deal structure, or the overall risk profile of the transaction require corporate development and deal sponsor involvement.

The Integration Management Office

For larger or more complex transactions, a dedicated integration management office takes over execution responsibility once the deal closes.

The integration management office translates the integration plan developed during due diligence into tracked workstreams with owners, milestones, and escalation paths.

The handoff from the deal team to the integration management office is a structural risk point.

If the due diligence team and the integration team are entirely separate, institutional knowledge about the target does not transfer, and the integration team starts from a weaker position than the deal team finished.

Overlapping membership, where the corporate development lead and key functional leads remain involved through the first 100 days post-close, mitigates this risk.

Building M&A Execution Capability That Compounds Over Time

The M&A team structure described in this article is not a one-time project.

It is an organizational capability that compounds with every transaction, and a consistently effective M&A team structure is what separates serial acquirers from opportunistic ones.

Companies that build strong internal M&A team structures develop institutional knowledge, accumulate templates and processes that reduce setup time on future deals, and retain the advisor relationships that make execution more efficient.

The corporate development team is the organizational hub of this capability, and its effectiveness depends on a structured understanding of how to design and run a complete mergers and acquisitions process from origination through integration.

For practitioners looking to build this capability, the full deal lifecycle including team structure, deal sourcing, due diligence, negotiation, financing, and post-merger integration is covered in the M&A Institute curriculum.

Section 5: Communication Discipline That Keeps the M&A Team Structure Aligned

An M&A team structure functions only as well as its communication discipline.

Deals run in parallel across multiple workstreams, and without structured communication the M&A team structure breaks down as problems in one workstream remain invisible to others until they affect the entire deal.

Weekly Steering Committee Meetings

Core team members meet weekly throughout the transaction to review workstream progress, share due diligence findings, update the valuation model, and make tactical decisions on next steps.

The meeting agenda covers due diligence status across all functional workstreams, valuation updates reflecting new information, negotiation strategy and open commercial points, and integration planning progress.

The discipline of a weekly meeting creates shared situational awareness that allows the team to identify cross-workstream dependencies before they become bottlenecks.

For example, if the IT workstream identifies a cybersecurity issue that could require regulatory disclosure, the legal team needs to know immediately rather than at the next scheduled update.

The steering committee provides the forum where information moves across functions without waiting for someone to independently recognize the dependency.

Information Compartmentalization

M&A transactions require strict confidentiality, which creates a communication challenge inside larger organizations.

The internal M&A team must share information freely enough to coordinate effectively while limiting disclosure to individuals who genuinely need access.

A common practice is to assign code names to transactions during the pre-announcement phase, allowing team members to communicate in writing without inadvertently disclosing the target’s identity.

Access to the data room, the financial model, and due diligence reports should be restricted to named team members on a need-to-know basis.

Information leakage before a deal is announced can affect the target’s share price in public company transactions, alert competitors, or compromise the acquirer’s negotiating position.

Board Communication

Board communication is a structured workstream in its own right.

The deal sponsor is responsible for keeping the board informed at each major decision point: investment thesis approval, letter of intent, final due diligence findings, deal structure and price, and signing authorization.

Board presentations should translate technical due diligence findings, valuation outputs, and risk assessments into strategic language that allows directors to exercise meaningful oversight.

The deal negotiation process produces the commercial terms the board ultimately approves, which means the corporate development lead must maintain an accurate summary of open deal points throughout the negotiation period.

Sources

- Building the Right Organization for Mergers and Acquisitions, McKinsey & Company

- Is Your M&A Organization Built to Win? BCG 2024 M&A Report

- Corporate Development Explained: Strategy and M&A Tactics, DealRoom