Merger Integration Strategy: 8 Deal Types, One 100-Day Plan

A company closes an acquisition, declares success, and begins integration.

Eighteen months later, key managers from the acquired company have left, projected cost savings have not materialized, and the combined entity is underperforming both businesses on a standalone basis.

This outcome is not bad luck.

It is the result of applying a generic merger integration strategy to a deal that required a specific one.

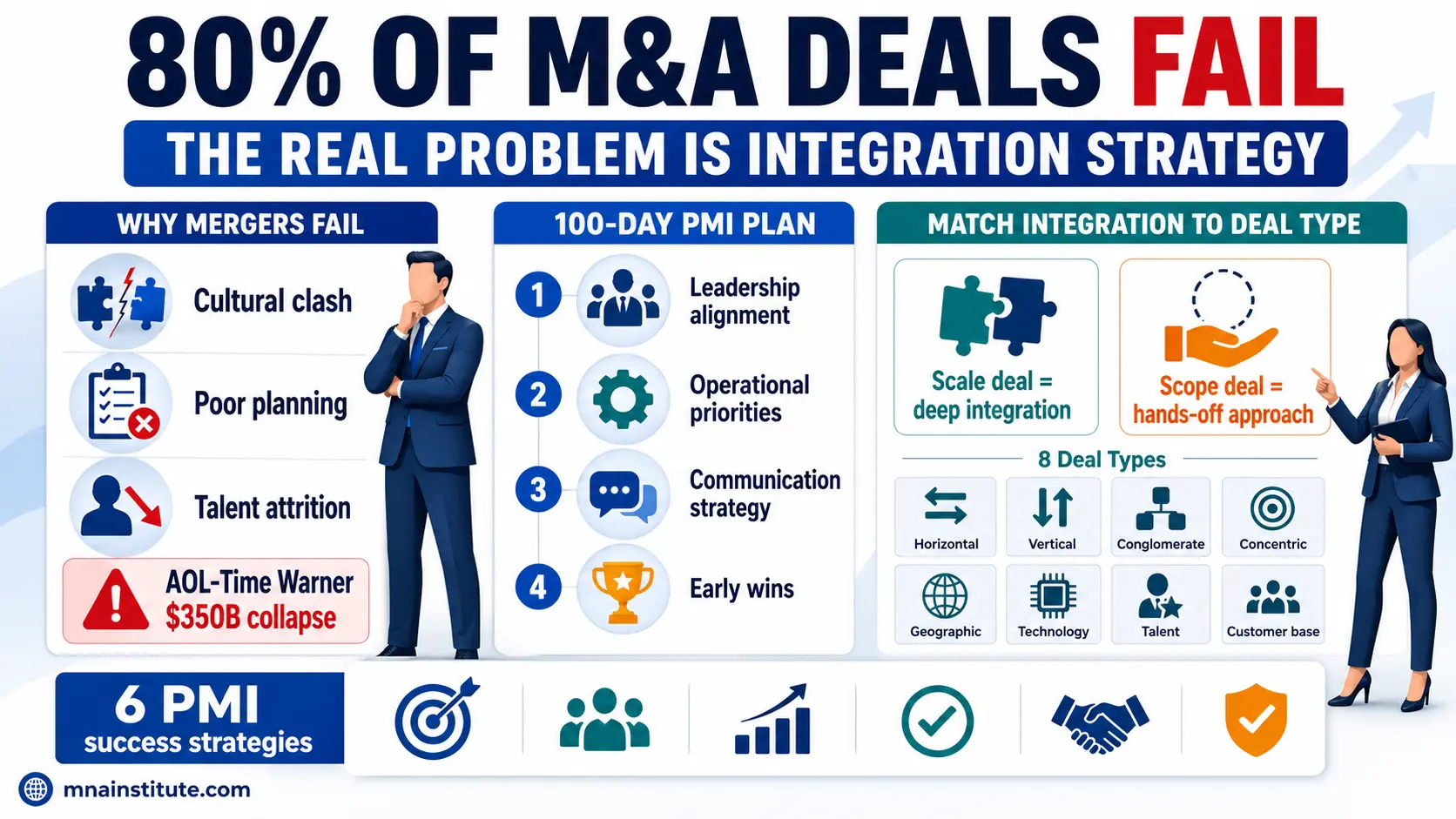

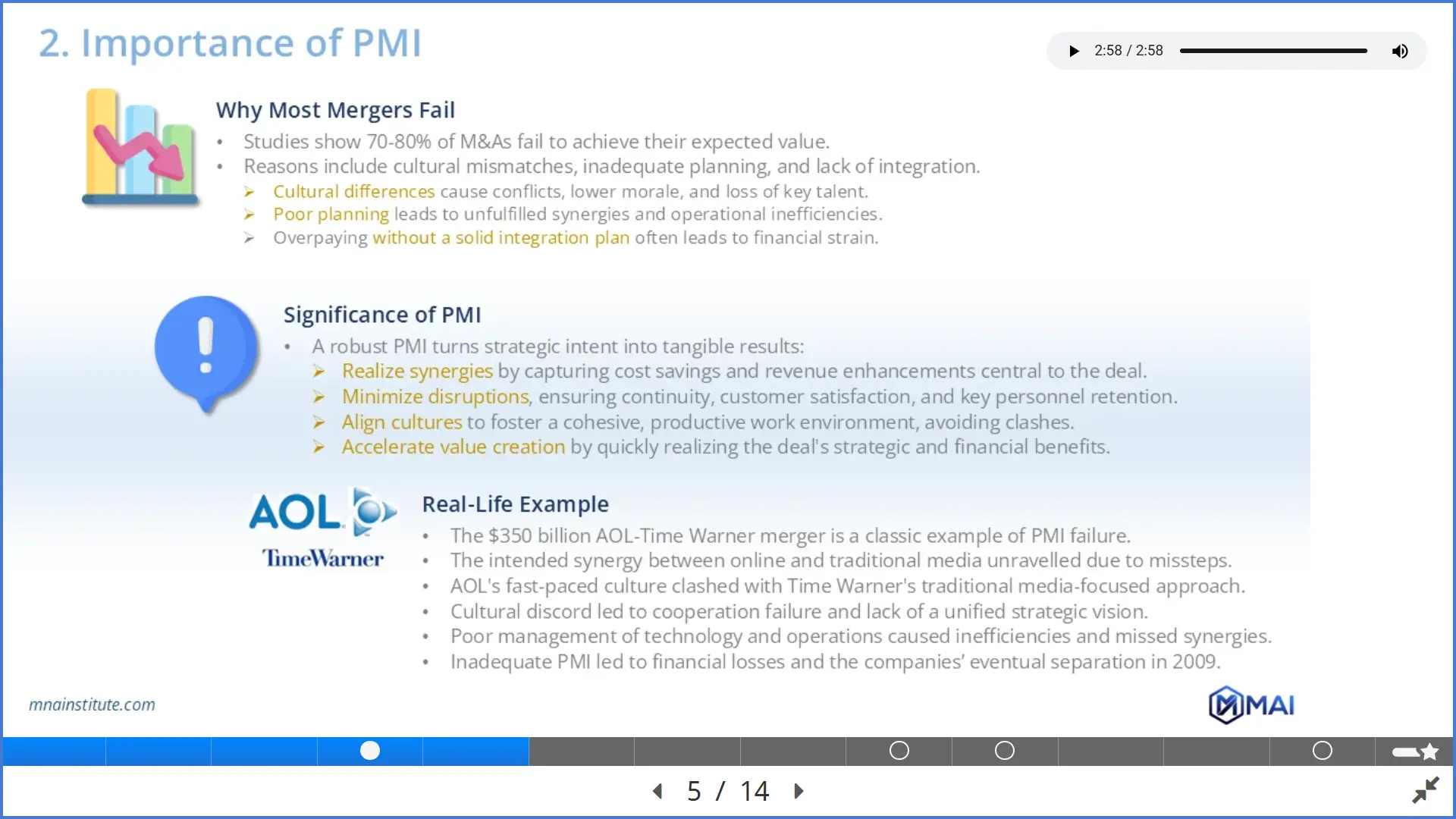

Studies consistently show that 70 to 80 percent of M&A transactions fail to deliver their expected value, and the failure point is almost always the post-merger integration phase rather than the deal itself.

This article explains what an effective merger integration strategy looks like, why the 100-day integration plan matters, what the main M&A integration challenges are, and how to match the integration approach to the specific type of deal being executed.

What Post-Merger Integration Actually Involves

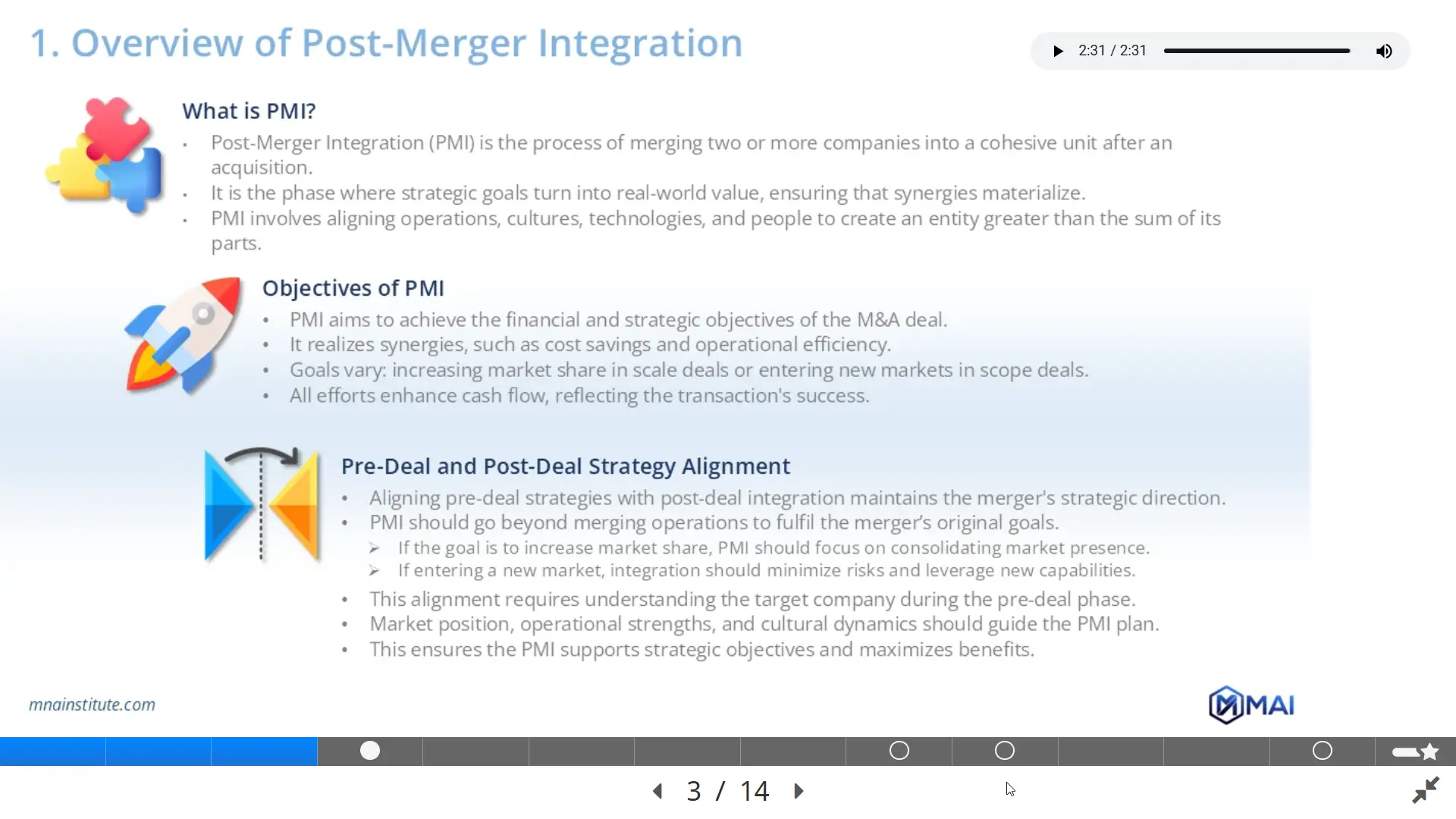

Post-merger integration is the process of combining two or more companies into a functioning unit after a deal closes.

It is where the strategic intent of the transaction is either executed or abandoned.

Every merger integration strategy must deliver on the financial and strategic objectives that justified the deal in the first place, which is why integration planning belongs inside the mergers and acquisitions process from the earliest stages, not as an afterthought after signing.

PMI covers four distinct dimensions: operational alignment, cultural integration, technology consolidation, and people management.

Each dimension carries its own risks and timeline, and the failure to manage any one of them can undermine the entire deal thesis.

Realizing Synergies

Synergies are the financial justification for paying an acquisition premium.

Cost synergies typically come from eliminating redundant functions, consolidating facilities, and achieving procurement scale.

Revenue synergies come from cross-selling, expanding into new markets, or combining product lines.

The merger integration strategy must convert these projected synergies into operational decisions with owners, timelines, and measurable outcomes.

A synergy that is not assigned to a specific person with a specific deadline is not a synergy plan.

It is a hope.

Maintaining Business Continuity

Integration activity creates internal disruption, and customers notice.

A merger integration strategy that prioritizes internal consolidation over external continuity risks losing customers to competitors who simply show up and execute while the combined company is absorbed in itself.

Key employee attrition during integration compounds this risk.

When the people who carry customer relationships leave within the first year, the revenue assumptions built into the deal model deteriorate alongside them.

Pre-Deal and Post-Deal Alignment

The merger integration strategy must be built from the deal rationale, not designed independently after closing.

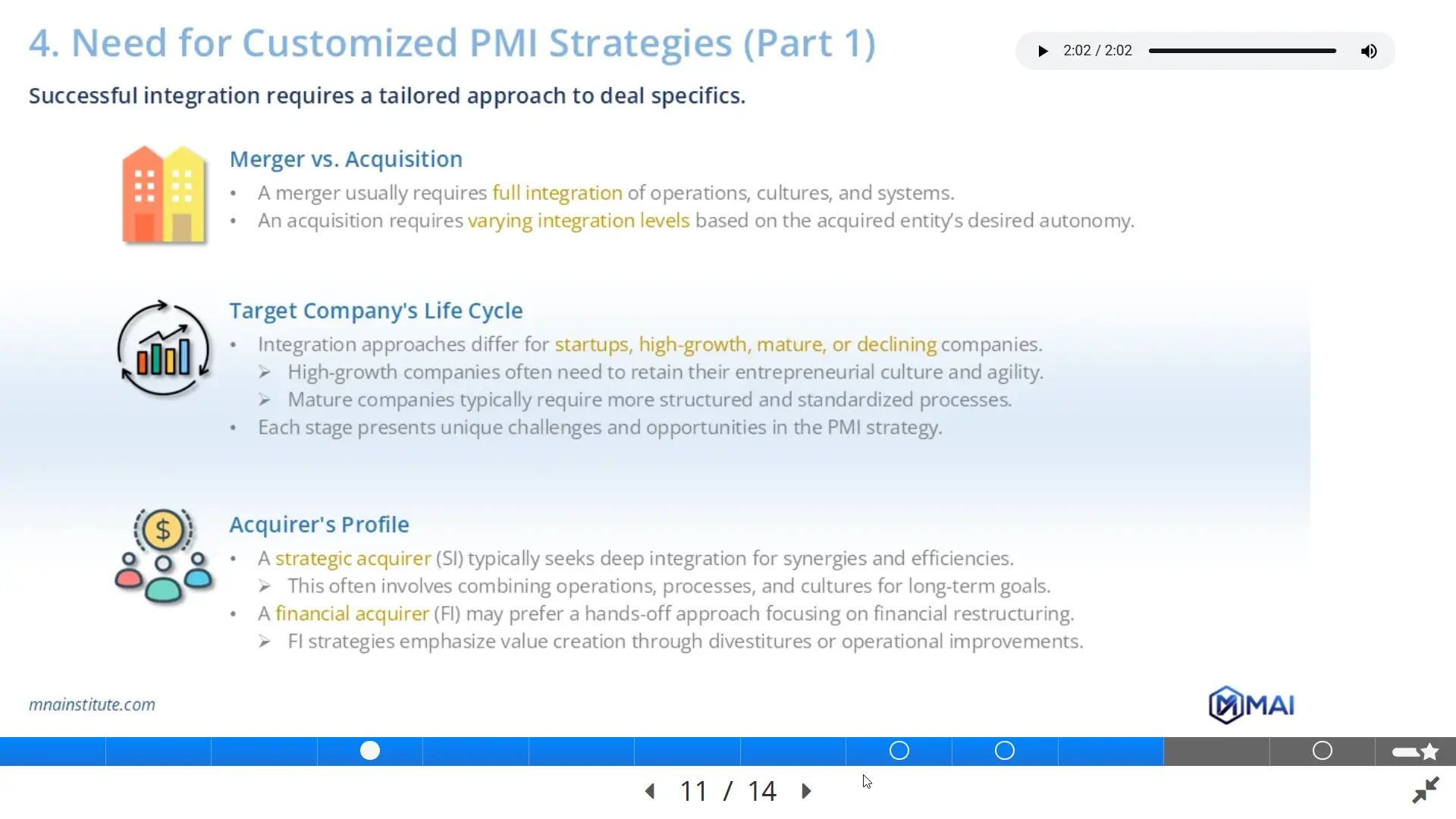

If the deal was a scale acquisition within the same industry, the integration should prioritize operational consolidation and cost synergy capture.

If the deal was a scope acquisition entering a new market or acquiring new capabilities, the integration should focus on minimizing disruption to the acquired company while extracting knowledge and market access.

These two types of deals require fundamentally different integration approaches, and confusing them is one of the most common M&A integration challenges acquirers face.

Why Most Merger Integration Strategies Fail

The AOL-Time Warner merger in 2000, valued at approximately 350 billion dollars, is the most widely cited example of integration failure at scale.

The merger was designed to combine AOL’s internet reach with Time Warner’s content and cable infrastructure.

AOL’s fast-moving, technology-driven culture collided with Time Warner’s established, media-centric organizational style.

The two leadership teams could not agree on strategic priorities, decision-making authority, or operational direction.

Employees from both companies were uncertain about the organizational structure they belonged to, which accelerated attrition across both sides.

Technology integration was mismanaged, synergies were not captured, and the companies formally separated in 2009 after writing down nearly 100 billion dollars in goodwill.

The AOL-Time Warner case illustrates three M&A integration challenges that appear across failed mergers regardless of industry or deal size.

Cultural Mismatch

Cultural differences between two organizations do not resolve themselves after a deal closes.

They accelerate if not addressed deliberately.

When management philosophy, risk tolerance, decision-making speed, and performance expectations differ between the two companies, the combined organization produces conflict rather than collaboration.

The merger integration strategy must include a cultural assessment during due diligence and a structured cultural integration workstream from day one of closing.

Inadequate Planning

Integration planning that begins after signing is too late.

Effective due diligence surfaces integration risks and synergy opportunities before the price is locked.

When integration planning starts only after closing, the first 100 days are consumed by discovery rather than execution, and synergy capture delays compound into permanent value destruction.

Talent Loss

Key employees from the acquired company face uncertainty about their roles, their reporting lines, and their future in the combined organization.

Without a proactive retention strategy, the people who carry the institutional knowledge and customer relationships that justified the acquisition price are the first to leave.

Replacing senior talent takes time and budget that the integration plan did not account for.

In knowledge-intensive businesses such as professional services, technology, or advisory firms, talent loss can directly translate into client loss within the same quarter.

6 Rules for an Effective Merger Integration Strategy

The following six rules apply across deal types and acquirer profiles.

They are not sequential steps but parallel disciplines that must run simultaneously from the moment the deal is signed.

Rule 1: Integration Planning Starts in Due Diligence

The merger integration strategy should be drafted in parallel with the due diligence process, not after it concludes.

Due diligence findings on cultural fit, operational compatibility, technology infrastructure, and talent depth directly inform the integration workstreams that will need to run after closing.

Cross-functional teams from both organizations should be identified and briefed on integration objectives before the deal closes so that execution can begin immediately on day one.

Rule 2: Appoint a Dedicated Integration Leader

The integration cannot be managed as a part-time responsibility alongside existing operational roles.

A dedicated PMI leader with real decision-making authority must own the process end to end.

This person sets the cadence, resolves cross-functional conflicts, holds workstream owners accountable, and communicates progress to the executive team and board.

Without a single accountable leader, integration workstreams drift independently and the synergy timeline slips.

Rule 3: Retain Key Talent Before Competing Offers Arrive

Retention packages for identified key employees should be agreed and communicated within the first weeks of closing, not weeks or months later.

The window for retaining critical talent is narrow because competitors and executive search firms begin reaching out to acquired company employees as soon as a deal is announced.

A shared vision and set of organizational values must be communicated clearly and consistently to give employees from the acquired company a reason to stay beyond the financial retention package.

Rule 4: Execute a Concrete 100-Day Integration Plan

The 100-day integration plan covers the period immediately following close and sets the organizational tone for the entire integration.

It should specify three priorities: leadership alignment between the two executive teams, early operational wins that demonstrate integration momentum, and a communication cadence that keeps all employees informed about what is happening and why.

An early operational win does not need to be large.

A consolidated procurement contract, a unified IT helpdesk, or a shared finance reporting process gives employees visible evidence that the integration is progressing rather than stalling.

Weekly steering committee reviews during the 100-day period allow the integration leader to surface blockers, reallocate resources, and adjust workstream sequencing before delays compound.

The 100-day integration plan does not complete the merger integration strategy.

It establishes the foundation on which the longer integration timeline is built.

Rule 5: Build in Adaptability

No integration plan survives first contact with the combined organization unchanged.

Technology systems that appeared compatible during due diligence reveal incompatibilities during migration.

Synergies that looked achievable in a model prove operationally complex to execute.

Customer responses to the merger are different from what management expected.

The merger integration strategy must include explicit contingency responses for the most predictable failure modes, and the integration team must have the authority to adjust the plan without escalating every decision to the C-suite.

Rule 6: Document and Build Institutional Knowledge

Every integration, whether it succeeds or struggles, produces lessons that are worth preserving.

Organizations that document their integration experiences in structured playbooks, including what worked, what failed, and what they would do differently, develop a compounding M&A execution advantage over competitors who treat each deal as their first.

This institutional knowledge reduces setup time on future integrations and helps the organization avoid repeating the same planning mistakes.

The 8-Type PMI Matrix: Matching Merger Integration Strategy to Deal Type

The single most common M&A integration challenge is applying a standardized integration approach to deals that require fundamentally different ones.

The merger integration strategy must be calibrated to the type of deal being executed.

The following framework covers the eight deal types and the integration approach each requires.

Horizontal M&A: Scale Within the Same Industry

Horizontal deals combine companies operating in the same industry to achieve cost synergies and market share gains.

The merger integration strategy for a horizontal deal demands deep operational integration: consolidating overlapping functions, rationalizing duplicate facilities, and standardizing processes across the combined entity.

Consider a hypothetical example: a regional bank acquires a smaller competitor in the same market.

The integration immediately consolidates back-office operations, merges the branch networks where geography overlaps, and unifies the technology platform to eliminate duplicate licensing costs.

These actions are the entire point of the deal and must be executed with precision and speed.

Vertical M&A: Supply Chain Integration

Vertical deals combine companies at different stages of the same supply chain, such as a manufacturer acquiring a key supplier.

The M&A integration strategy here sits between scale and scope, requiring the integration of different production stages while preserving the operational identity of each unit.

The risk in vertical integration is over-consolidating and losing the efficiency that made the acquired company valuable as a specialized supplier.

Conglomerate M&A: Scope Through Diversification

Conglomerate deals combine companies across unrelated industries.

The merger integration strategy for a conglomerate acquisition is deliberately light.

The acquired company operates with significant autonomy because shared operations would add complexity without adding value.

The acquirer provides capital allocation and financial oversight while leaving management and operations intact.

Berkshire Hathaway is the most widely known example of this model applied consistently across decades and dozens of acquisitions.

Concentric M&A: Scale and Scope Combined

Concentric deals expand into adjacent markets or product categories that are synergistic with the acquirer’s core business.

The M&A integration strategy for concentric deals requires both operational integration in overlapping areas and cultural adaptation to manage the differences between the two organizations.

This is one of the more demanding integration profiles because it requires simultaneous execution in multiple dimensions.

Geographic Expansion

Geographic expansion deals replicate an existing business model in a new market.

The merger integration strategy must balance standardization of the core operating model with localization of customer-facing operations to reflect the preferences and regulations of the new geography.

A retail chain entering a new country, for example, might standardize its supply chain and technology infrastructure while adapting its product range, store format, and marketing to local consumer behavior.

The M&A integration challenges in geographic expansion deals are often regulatory rather than operational, requiring the acquirer to navigate employment law, data protection rules, and competition oversight in the new jurisdiction.

Technology and R&D Acquisition

Technology acquisitions are motivated by the acquirer’s need for capabilities, platforms, or intellectual property it cannot develop fast enough internally.

The M&A integration strategy for technology deals must protect the innovation environment that produced the value being acquired.

This means light operational integration, significant knowledge transfer investment, and a talent retention approach that preserves the engineering and product teams.

When Google acquired YouTube in 2006 for 1.65 billion dollars, the YouTube team continued to operate with substantial autonomy while benefiting from Google’s infrastructure and advertising platform.

Disrupting the YouTube product team would have undermined the acquisition thesis.

Talent Acquisition

Some deals are motivated almost entirely by the people being acquired rather than the business they operate.

The merger integration strategy for talent acquisitions focuses on cultural integration, retention packages, and role definition within the combined organization.

Operational integration is secondary because the acquired business may be wound down or absorbed as a product line rather than maintained as a standalone entity.

Customer Base Expansion

Customer base expansion deals acquire a company primarily for its existing customer relationships.

The merger integration strategy must prioritize the integration of sales teams, CRM systems, and customer service operations to capture the revenue potential of the combined customer base.

Disrupting the acquired company’s customer-facing operations before the integration of sales and service infrastructure is complete risks the customer attrition that the deal was designed to prevent.

Acquirer Profile and Target Life Cycle Determine Integration Depth

The deal type is not the only variable that shapes the merger integration strategy.

The acquirer’s profile and the target’s stage of development both affect how deeply the two organizations should be integrated.

Strategic Acquirer Versus Financial Acquirer

A strategic acquirer is typically a corporation seeking operational synergies and long-term market position.

Its merger integration strategy involves deeper integration of operations, processes, and culture because the synergies that justify the deal require actual organizational combination.

A financial acquirer such as a private equity firm typically pursues a lighter integration approach.

The firm focuses on financial restructuring, operational efficiency improvements, and positioning the business for exit rather than combining it with another operating company.

The 100-day integration plan for a private equity acquisition looks very different from that of a corporate strategic merger, even when the target business is identical.

Target Life Cycle Considerations

Integrating a startup requires preserving entrepreneurial agility and the innovation culture that produced the technology or product being acquired.

Imposing the acquirer’s corporate processes on a 30-person startup immediately after close typically destroys the organizational characteristics that made the acquisition attractive.

Integrating a mature company with established processes and a large workforce requires more structured coordination.

The integration workstreams are larger, the change management challenge is more complex, and the timeline for capturing cost synergies is typically longer.

A declining company presents a different set of M&A integration challenges entirely, as the acquirer must simultaneously execute integration while stabilizing a deteriorating business.

Building M&A Integration Capability

The merger integration strategy is not a document that is produced once and followed mechanically.

It is an organizational capability that must be built, tested, and refined through each transaction.

Companies that treat integration as a repeatable discipline rather than a one-time project develop faster synergy capture, lower talent attrition, and better deal outcomes over time.

The full deal lifecycle, from sourcing and due diligence through negotiation, financing, and post-merger integration, requires structured knowledge and practical execution skills that compound with every transaction.

M&A Institute’s mergers and acquisitions curriculum is organized around the complete deal process, from first screening through integration completion.

- Mergers and Acquisitions Online Course

- M&A Due Diligence: CDD, FDD, LDD, & HRDD

- Post-Merger Intergration and Value-Up Strategy

Sources

- The Secret of Successful Acquisitions, Harvard Business Review

- Perspectives on Merger Integration, McKinsey & Company

- AOL Time Warner Merger: A Cautionary Tale, The New York Times