M&A Finance Integration: A 6-Phase Roadmap That Works

In many acquisitions, the deal model assumes that revenue synergies, cost savings, tax benefits, and better cash flow will appear after closing.

M&A finance integration is the operating discipline that tests whether those assumptions are becoming measurable reality.

The finance team is not only closing the monthly books or mapping accounting codes.

It is controlling cash, aligning reporting, tracking synergy KPIs, managing debt capacity, testing customer profitability, and making sure the post-close company does not drift away from the investment case.

That is why post merger integration finance needs a structured roadmap from Day 1 to Year 1.

A buyer may have a strong strategy, but if finance cannot see cash flow, control reporting, identify risks, and monitor value creation, the deal thesis becomes difficult to manage.

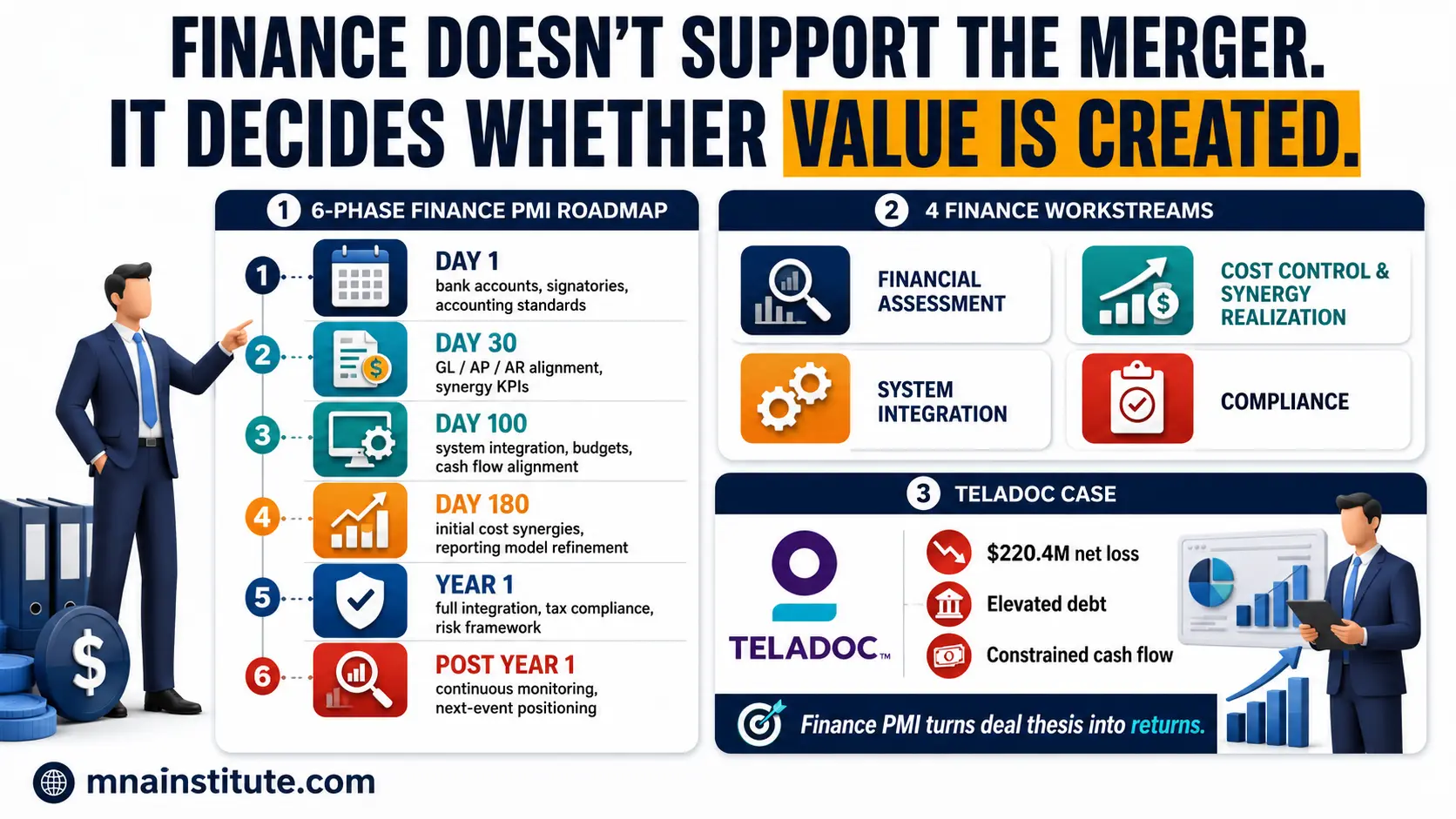

This article explains M&A finance integration through a six-phase roadmap that covers finance planning, value-up strategy, diligence, systems integration, KPI tracking, and a financial integration example using Teladoc-style private equity ownership.

A well-run M&A finance integration process gives executives one integrated view of cash, risk, reporting, and value creation.

Section 1. Finance Team’s Role in M&A Finance Integration Planning

M&A finance integration starts with financial control and decision visibility.

The finance team must understand the financial health of both companies before integration work becomes a series of disconnected system tasks.

A practical finance review begins with balance sheets, cash flow, debt levels, working capital requirements, tax exposures, and projected synergies.

The purpose is not simply to confirm historical numbers.

The purpose is to determine whether the combined company can fund integration, protect liquidity, meet reporting requirements, and deliver the value that justified the acquisition price.

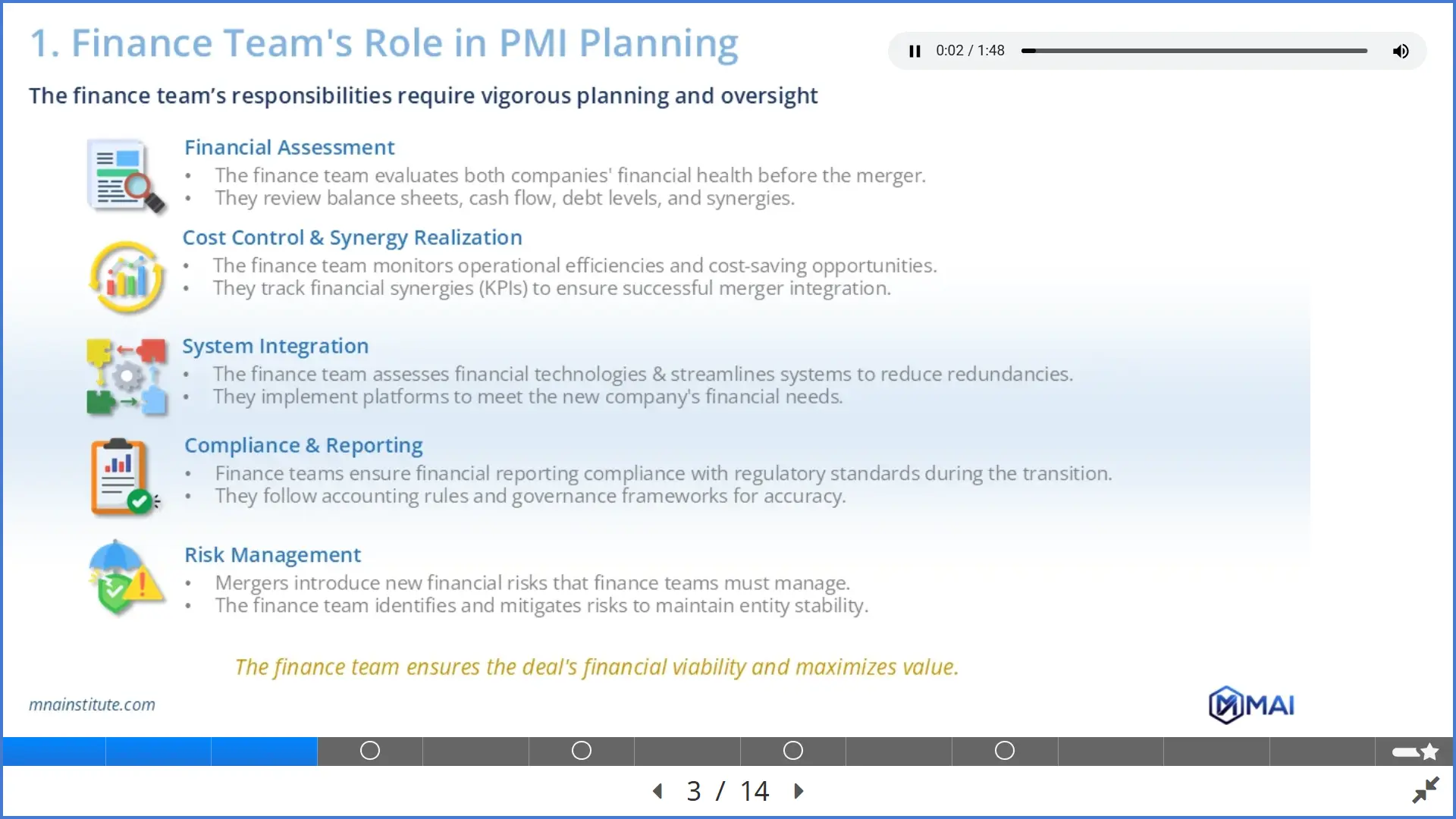

In a finance-led PMI setting, the CFO and finance leadership usually own five workstreams.

First, they perform financial assessment by reviewing historical performance, debt burden, cash conversion, and near-term funding needs.

Second, they lead cost control and synergy realization by tracking which savings are actually captured rather than merely announced.

Third, they support system integration by evaluating financial platforms, general ledger structures, consolidation tools, accounts payable processes, payroll interfaces, and reporting workflows.

Fourth, they maintain compliance and reporting by ensuring that the acquired business moves toward the acquirer’s accounting standards, governance procedures, and management reporting cadence.

Fifth, they manage financial risk by identifying liquidity pressure, debt constraints, tax issues, control gaps, and exposure created by inconsistent data.

This is where a financial integration plan becomes useful.

In practical M&A finance integration work, the plan should show exactly how finance will protect liquidity and measure value after closing.

It converts abstract integration objectives into specific finance workstreams, owners, deadlines, control points, and reporting outputs.

EY notes that M&A integration should begin by determining value drivers, guiding principles, integration strategy, leaders, governance, and workstreams.

For finance, those ideas translate into a question that should be asked immediately after signing.

What financial information, control rights, and reporting mechanisms must be in place on Day 1 so management can run the combined business without waiting for a full systems merger.

The answer should be practical rather than theoretical.

If cash access is unclear, signatories are not changed, debt obligations are not mapped, or reporting calendars are not harmonized, management cannot make reliable decisions after closing.

That is the first operating test of M&A finance integration.

A finance team should usually own these PMI control questions:

- Can the acquirer see cash, debt, working capital, and liquidity immediately after close?

- Can management produce reliable reporting without waiting for a full system migration?

- Can synergy KPIs be tracked against a baseline rather than against vague improvement claims?

- Can compliance, tax, governance, and risk controls operate without interruption during transition?

Section 2. Finance Team’s Value-Up Strategy in M&A Finance Integration

The second phase of M&A finance integration is value-up strategy.

This makes M&A finance integration a performance agenda rather than a back-office conversion exercise.

This is where the finance team moves from control to performance improvement.

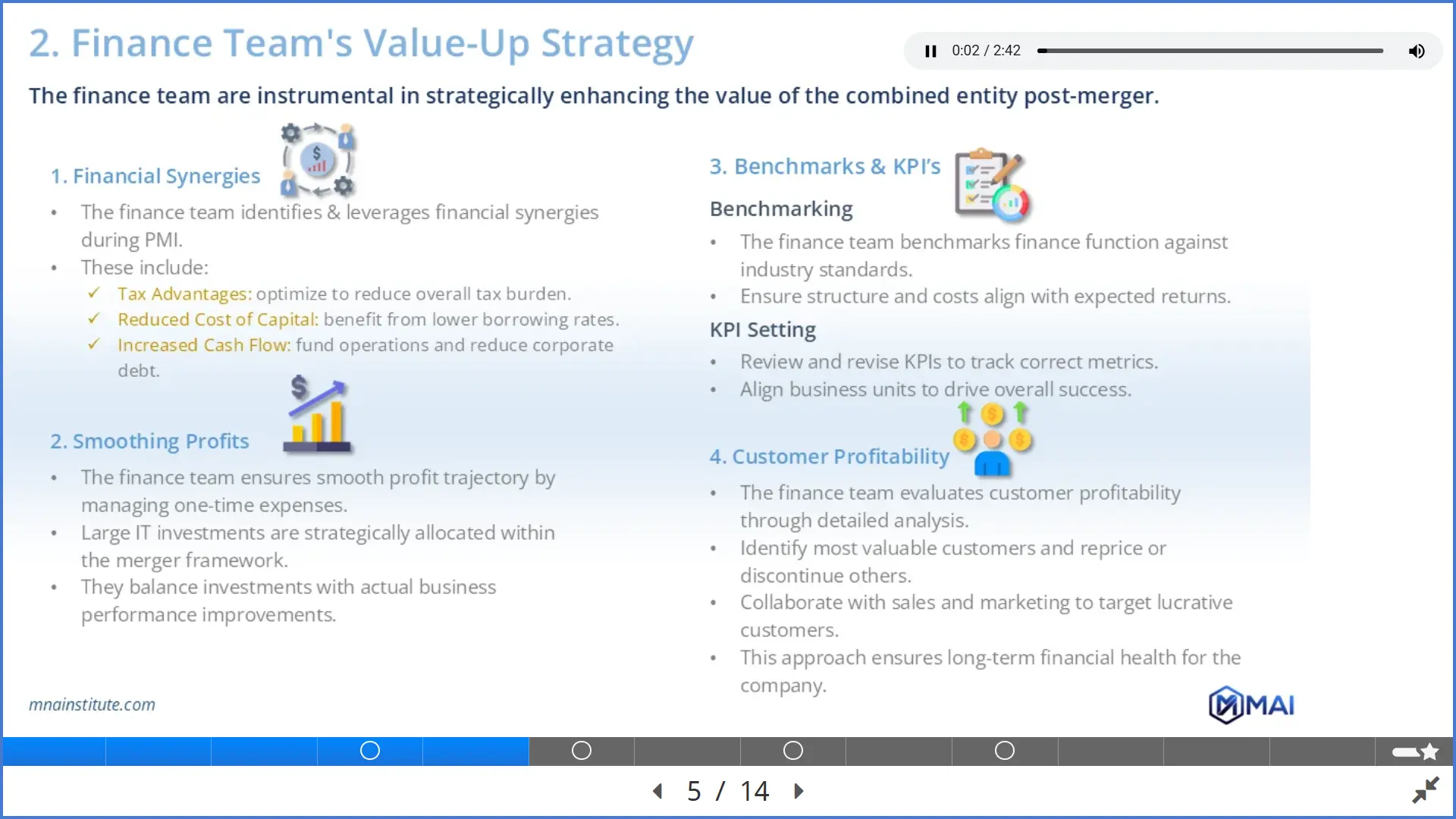

A transaction may create several categories of financial synergies, but they must be translated into measurable initiatives.

Tax advantages may come from improved structure, better use of losses, more efficient legal entity design, or jurisdictional planning.

Reduced cost of capital may become available if the combined company has a stronger credit profile, broader asset base, or more predictable cash flow.

Increased cash flow may come from cost savings, working capital improvements, pricing changes, lower customer acquisition cost, or reduced duplication across functions.

None of these benefits should be treated as automatic.

A finance team should create a synergy register that defines each initiative by owner, baseline, target, timing, required action, dependency, and KPI.

Deloitte’s post-merger integration guidance emphasizes that synergy initiatives should be prioritized and tracked with clear KPIs tailored to the target’s business model.

That principle is central to post merger integration finance because value that is not measured tends to become a management story rather than a financial result.

The finance team also plays a role in smoothing profits without hiding reality.

For example, a large IT migration may be required to integrate reporting, consolidation, payroll, and forecasting.

Finance should not simply approve the spend because integration requires it.

Finance should stage the investment, connect it to measurable process improvement, and compare the cost to the expected control, reporting, and synergy benefits.

This makes M&A finance integration different from ordinary budgeting.

The budget is not just a spending limit.

It is a value-control mechanism for the acquisition thesis.

Benchmarking and KPI setting also matter.

A merged company may need to revise its finance function metrics after closing because the scale, complexity, reporting needs, and risk profile have changed.

Relevant indicators may include cash conversion, days sales outstanding, days payable outstanding, working capital intensity, operating margin, tax leakage, finance cost as a percentage of revenue, forecast accuracy, and reporting close cycle time.

Customer profitability is another overlooked finance responsibility.

A buyer may celebrate revenue growth while ignoring low-margin customers that consume service resources, marketing spend, or working capital.

Finance can work with sales and marketing to identify customers that should be repriced, renewed differently, supported more efficiently, or exited over time.

That is why a financial integration plan should not stop at financial systems.

It should show how the finance function will help convert ownership into higher-quality earnings and stronger cash flow.

Section 3. Finance Team’s PMI Due Diligence for M&A Finance Integration

The third phase is PMI-focused financial due diligence.

For M&A finance integration, diligence is only useful when it identifies the financial control points that must be ready before and after closing.

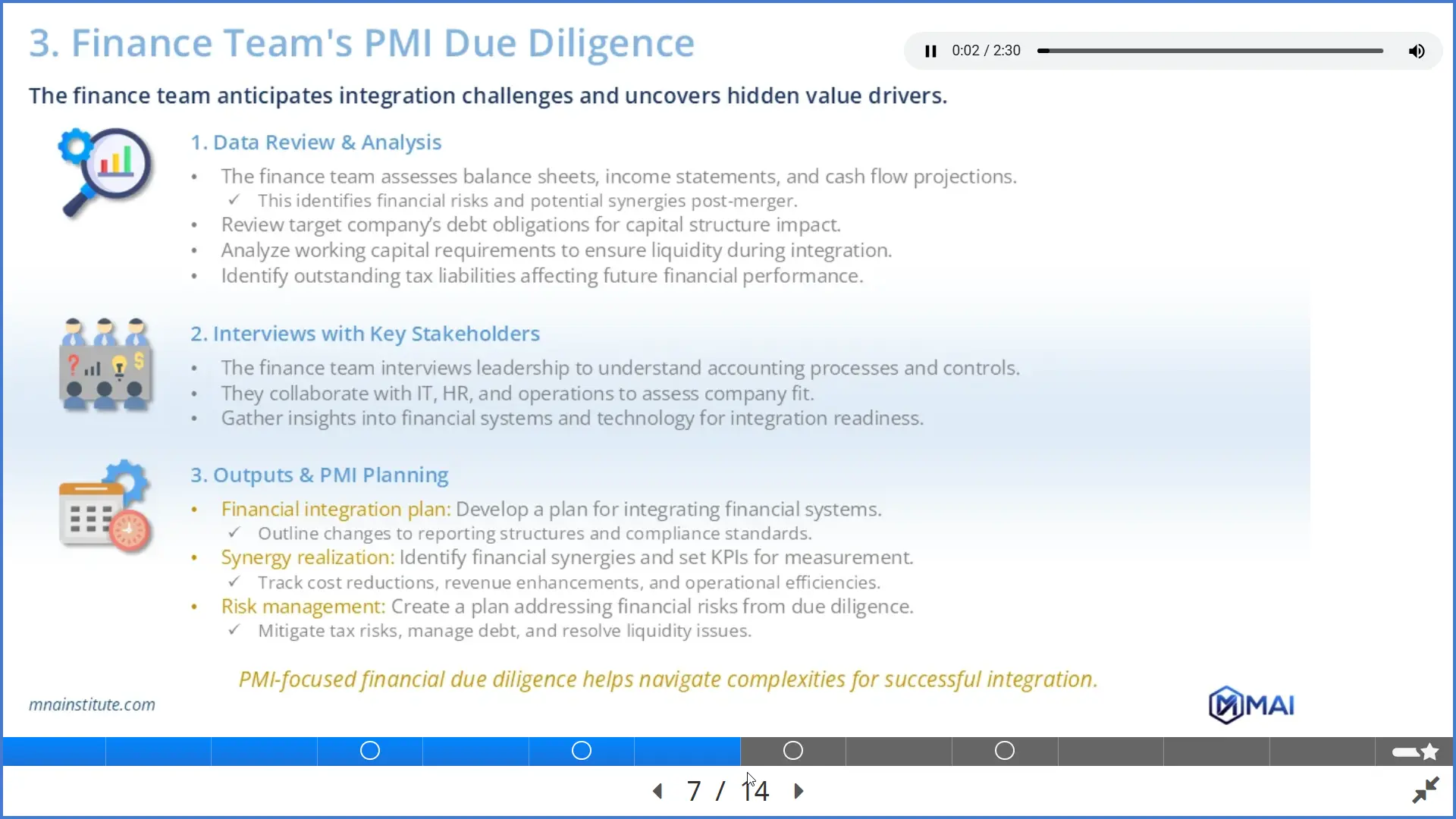

Traditional financial due diligence tests historical earnings, debt, working capital, tax exposure, accounting quality, and cash flow.

PMI-focused financial due diligence asks one additional question.

What must finance know before closing to integrate the company without losing control of liquidity, reporting, or value capture.

This means the due diligence team should not only review the target’s financial statements.

It should assess how the target actually produces financial information.

The review should cover balance sheets, income statements, cash flow projections, debt schedules, working capital cycles, tax liabilities, reporting calendars, accounting policies, and finance system architecture.

The team should also interview the target’s finance leadership to understand close processes, internal controls, forecasting methods, capital expenditure approval, revenue recognition judgments, and debt covenant monitoring.

A useful diligence question is simple.

If we owned this company tomorrow, how quickly could we produce a reliable management report that shows cash, revenue, margin, debt, working capital, and synergy progress.

If the answer is unclear, post merger integration finance will likely face early friction.

Finance should also collaborate with IT, HR, operations, tax, and legal during this phase.

IT explains system compatibility and data migration risk.

HR explains payroll, incentives, headcount, and restructuring implications.

Operations explains inventory, vendor commitments, supply constraints, and service delivery costs.

Tax explains exposures and structure choices.

Legal explains contractual restrictions that may affect reporting, cash control, or customer economics.

The output should be a finance integration roadmap that shows which tasks must happen on Day 1, Day 30, Day 100, Day 180, Year 1, and after Year 1.

The output should also include a risk management plan for liquidity, debt, tax, control gaps, reporting delays, and system migration issues.

This is where M&A due diligence connects naturally to the finance workstream because diligence findings must become integration actions rather than static reports.

In strong execution, due diligence does not end at signing.

It becomes the first draft of the financial integration plan.

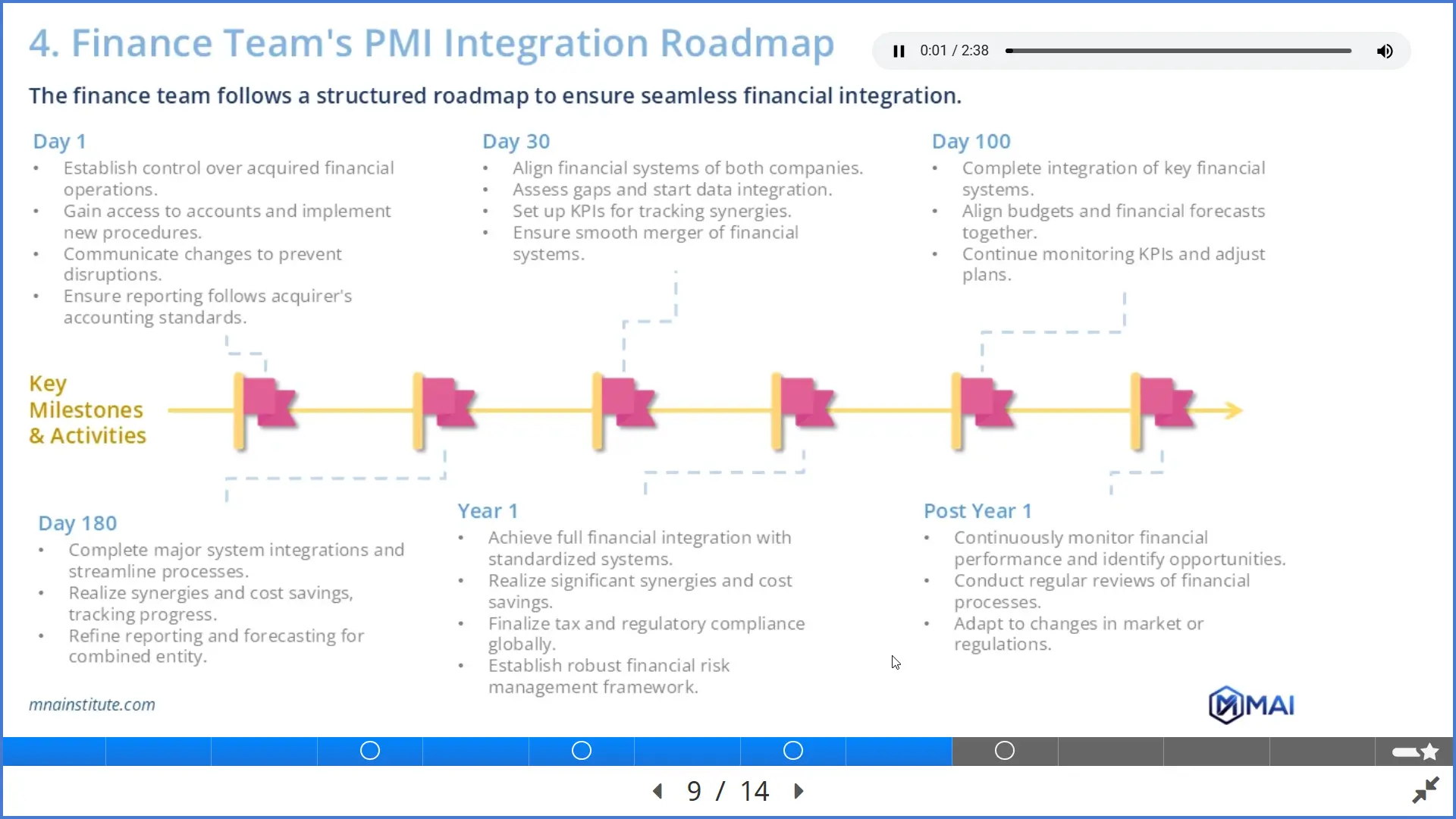

Section 4. M&A Finance Integration Roadmap

The fourth phase is the finance integration roadmap.

This is the point where M&A finance integration becomes a sequence of dated actions rather than a list of finance intentions.

A roadmap gives finance leaders a sequence for control, system alignment, KPI tracking, compliance, synergy realization, and long-term value creation.

The exact timing depends on deal complexity, transaction perimeter, regulatory environment, system compatibility, and the acquirer’s governance model.

Still, a six-phase finance integration roadmap is a useful starting structure.

|

Phase |

Finance priority |

Practical output |

|

Day 1 |

Control cash, reporting access, signatories, and finance governance |

Bank access, reporting timetable, control owner list, accounting standard alignment |

|

Day 30 |

Start finance system alignment and KPI tracking |

Gap assessment, synergy KPI dashboard, initial GL and AP process map |

|

Day 100 |

Complete initial system integration and refresh the forecast |

Combined budget, cash flow forecast, first synergy scorecard, revised integration plan |

|

Day 180 |

Streamline major finance processes and refine reporting |

Improved close cycle, reporting model, working capital actions, cost savings validation |

|

Year 1 |

Standardize finance operations and compliance |

Full finance integration, tax and regulatory compliance, risk management framework |

|

Post Year 1 |

Improve performance and identify new value creation opportunities |

Ongoing process reviews, new margin initiatives, refinancing or exit preparation if relevant |

On Day 1, the priority is control.

The finance team should establish authority over the acquired company’s financial operations.

This includes bank account access, changes to signatories, reporting procedures, cash forecasting, approval authorities, and immediate communication with the acquired finance team.

The aim is not to integrate everything on Day 1.

The aim is to make sure the acquirer can see and control the financial position of the acquired business.

By Day 30, finance should start aligning systems and metrics.

The team should map gaps between the two finance environments and decide whether to migrate, interface, or temporarily maintain separate systems.

KPIs should be launched at this stage, especially financial synergy indicators such as cost reductions, cash flow improvement, working capital movement, and forecast variance.

By Day 100, the combined entity should have a more complete view of budgets, forecasts, cash flow, synergy realization, and reporting reliability.

This is not always the point when all systems are fully integrated.

It is the point when management should know whether the integration is on track financially.

By Day 180, major system integrations and finance process improvements should be materially advanced.

The finance team should validate whether early cost savings are real, whether reporting is more stable, and whether forecasting reflects the combined entity rather than two legacy businesses.

By Year 1, the combined entity should move toward standardized finance processes, common reporting standards, and mature risk management.

Tax and regulatory compliance should be finalized in relevant jurisdictions.

After Year 1, finance should continue to monitor performance, find new value creation opportunities, and adapt to regulatory or market changes.

The best finance integration roadmap therefore does not simply describe milestones.

It links each milestone to control, liquidity, reporting, synergy, and strategic value creation.

This is the part of M&A finance integration that management teams often underestimate.

A clean ledger migration is useful, but it is not the full objective.

The full objective is to make financial performance visible, controllable, and improvable throughout the integration period.

Deloitte’s Day One readiness guidance also emphasizes business continuity as a central integration objective.

For finance, business continuity means that invoices are paid, customers are billed, payroll works, management reports are produced, debt obligations are monitored, and the board can see whether the deal is financially progressing.

Section 5. Financial Integration Example for M&A Finance Integration

A financial integration example makes the roadmap more concrete.

The example also shows how M&A finance integration differs when the buyer is focused on private equity value creation rather than full operating merger.

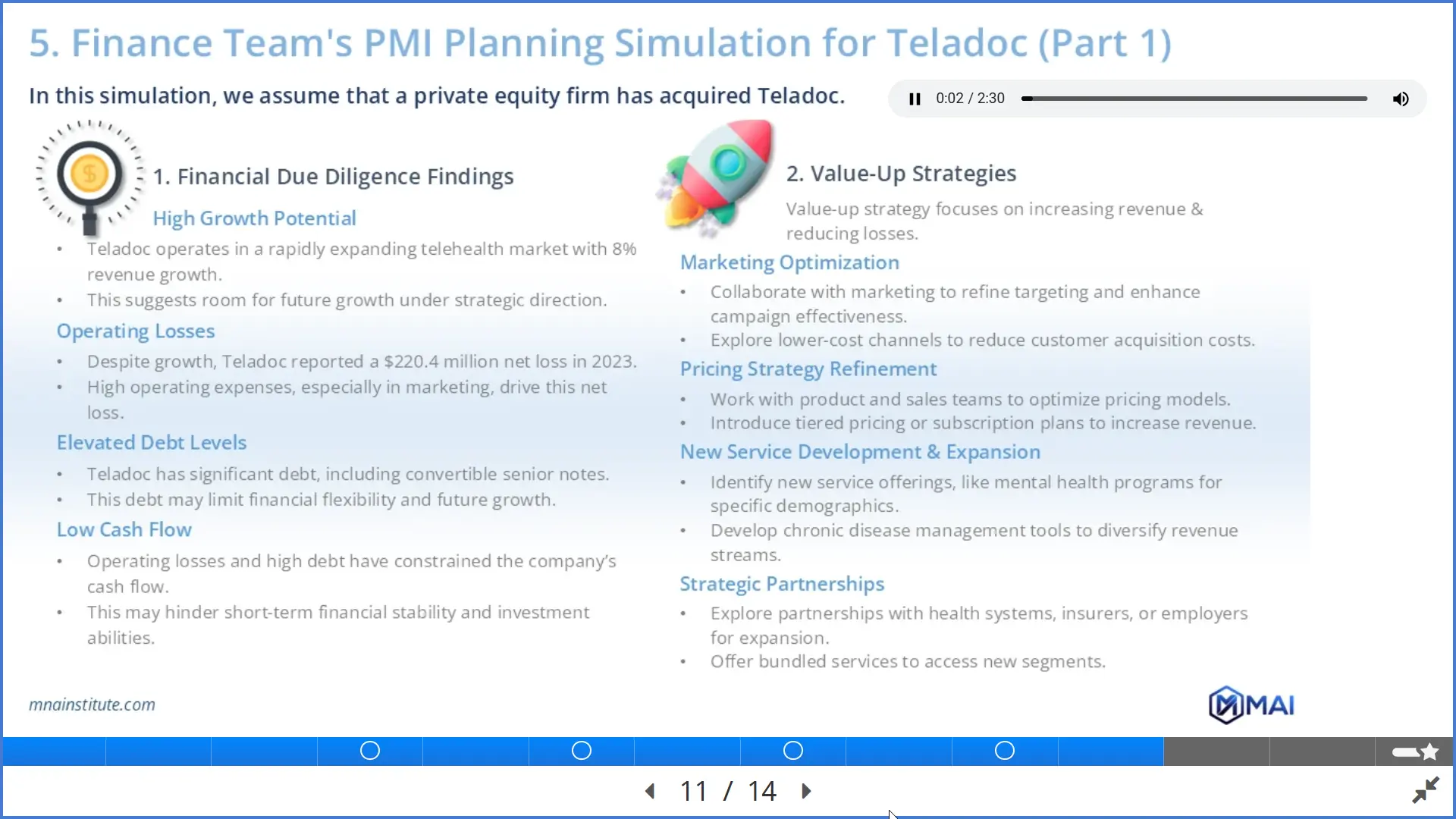

Assume that a private equity firm acquires Teladoc and wants to improve operating performance rather than merge Teladoc into another operating company.

This is a value-up scenario, not a full legal or operating merger.

Teladoc reported that full year 2023 revenue increased 8 percent to 2.6 billion dollars, while full year 2023 net loss was 220.4 million dollars.

Those numbers point to a company with scale and growth, but also a clear need for margin discipline, cost control, cash flow improvement, and stronger operating performance.

The finance team’s first due diligence finding would be growth potential.

Telehealth remains a large and competitive market, so revenue growth may be available under the right commercial and operating strategy.

The second finding would be operating losses.

A private equity owner would want to understand which costs are tied to durable growth and which costs should be reduced, repriced, or redirected.

The third finding would be debt and financial flexibility.

Debt obligations and cash flow constraints can limit the speed at which the company invests in growth initiatives, new products, or technology improvements.

The fourth finding would be cash generation.

Revenue growth does not automatically create value if cash conversion remains weak or the operating model consumes too much capital.

The value-up response would have several workstreams.

Marketing optimization would test customer acquisition cost by channel and move spending toward more efficient acquisition paths.

Pricing strategy refinement would examine whether tiered pricing, subscription design, or customer segmentation can improve average revenue and margin.

New service development could focus on areas such as mental health or chronic disease programs if those offerings improve retention and unit economics.

Strategic partnerships with health systems, insurers, or employers could help expand reach without relying only on direct acquisition spend.

The KPI dashboard would need to track revenue growth rate, customer acquisition cost, operating margin, debt-to-equity ratio, cash conversion, and reporting frequency.

This financial integration example shows why post merger integration finance is not limited to the accounting function.

Finance must evaluate strategy, capital allocation, marketing efficiency, pricing, debt capacity, and cash flow under one integrated value creation view.

The finance integration roadmap would also differ because this is a private equity acquisition rather than a corporate merger.

- On Day 1, finance would review cash flow, debt, working capital, controls, and reporting mechanisms.

- By Day 30, it would identify cost reduction opportunities, pricing actions, and potential portfolio synergies.

- By Day 100, it would execute cost actions, monitor profitability, and begin building new service initiatives identified during diligence.

- By Day 180, it would refine pricing, continue product development, and validate cost improvements.

- By Year 1, it would aim to improve operating income, cash flow, and the strategic case for future refinancing or exit.

This is a practical example of how a financial integration plan changes depending on deal type and ownership objective.

Practical KPI Dashboard for the Financial Integration Example

|

KPI |

Why finance tracks it |

Typical owner |

|

Revenue growth rate |

Tests whether value-up initiatives are expanding the top line |

FP&A |

|

Customer acquisition cost |

Measures whether marketing optimization is improving efficiency |

Finance and Marketing |

|

Operating margin |

Shows whether cost actions and pricing translate into profitability |

FP&A |

|

Debt-to-equity ratio |

Tracks financial risk and refinancing readiness |

Treasury |

|

Cash conversion |

Shows whether earnings quality is turning into available cash |

Treasury and FP&A |

Related Courses

- Mergers and Acquisitions Online Course

- M&A Due Diligence: CDD, FDD, LDD, & HRDD

- Post-Merger Intergration and Value-Up Strategy

M&A finance integration sits inside the broader deal execution and value creation workflow.

- The Mergers and Acquisitions Online Course covers the end-to-end transaction logic that connects deal rationale, due diligence, valuation, negotiation, integration, and value capture.

- For finance teams, M&A Due Diligence: CDD, FDD, LDD, & HRDD is especially relevant where financial findings must be converted into integration priorities.

- For post-close execution, Post-Merger Intergration and Value-Up Strategy connects financial integration with the broader operating model, synergy execution, and value-up agenda.

The practical lesson is straightforward.

M&A finance integration should be treated as a CFO-led value architecture, not a delayed system migration.

Finance should not wait until after closing to design the reporting, control, KPI, and value-capture architecture.

The deal model only becomes real when M&A finance integration turns it into cash flow, governance, and measurable performance.

Sources

- EY-Parthenon, Nine steps to setting up an M&A integration program

- Deloitte, M&A integration plan for Day One readiness

- Deloitte, Delivering the promised returns: Post-Merger Integration

- Teladoc Health, Fourth Quarter and Full Year 2023 Results