BATNA and WATNA Negotiation in M&A: Set 3 Firm Lines

A serious acquisition negotiation should not begin with the question of how much the buyer wants to pay.

It should begin with a harder question: what happens if this deal fails.

BATNA and WATNA give the buyer that discipline before the first difficult meeting with the seller.

BATNA stands for Best Alternative To a Negotiated Agreement, and WATNA stands for Worst Alternative To a Negotiated Agreement.

In simple terms, BATNA and WATNA define the top and bottom of the buyer’s fallback reality.

That reality matters because a buyer without a quantified alternative is not negotiating from strategy.

It is negotiating from hope.

In M&A, hope becomes expensive when the seller senses urgency, weak alternatives, or internal pressure to close.

A practical buyer therefore converts alternatives, delays, integration costs, investor return thresholds, and non-negotiable conditions into a firm walk away price.

This is the point where negotiation skills BATNA analysis supports become visible in real deal behavior.

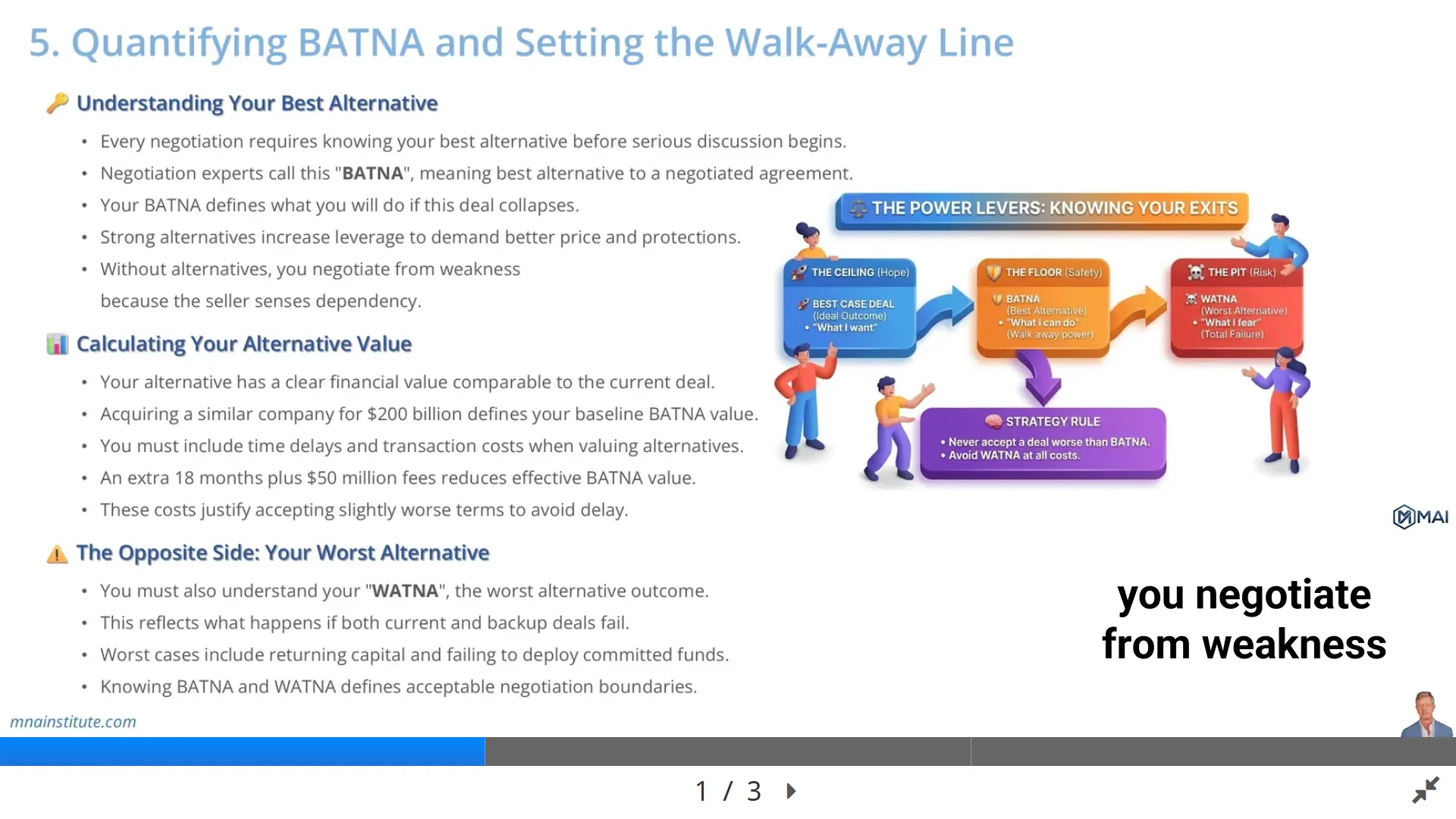

Understanding Your Best Alternative

BATNA and WATNA begin with the buyer’s best alternative to the current deal.

If the current acquisition fails, the buyer must know what it would actually do next.

That alternative might be acquiring another company, investing in organic growth, returning capital to investors, or waiting for a better target.

The alternative must be real enough to execute, not just a name mentioned in an investment committee meeting.

A buyer that says it has many alternatives but has not priced any of them has weak leverage.

A buyer that has identified a realistic backup deal, estimated its cost, assessed its regulatory complexity, and modeled its integration burden has a stronger position.

That is the practical meaning of BATNA negotiation in M&A.

BATNA and WATNA convert alternative deal options into a negotiation boundary.

The seller does not need to know the exact alternative.

However, the seller should sense that the buyer has a credible fallback and will not accept every concession simply to keep the transaction alive.

The Program on Negotiation at Harvard Law School describes BATNA as what a party will do if it does not reach a deal.

For M&A professionals, that definition becomes operational only when the fallback is converted into financial value.

A fallback with no model does not create leverage.

A fallback with quantified value, timing, execution cost, and risk adjustment can anchor the buyer’s walk away price.

Calculating Your Alternative Value

The first step in how to calculate BATNA in M&A is to compare the current target against a realistic alternative transaction.

Suppose a buyer is negotiating to acquire Target A for 280 billion dollars.

The buyer has also identified Target B, a similar company that could be acquired for 220 billion dollars.

At first glance, Target B appears cheaper.

That does not automatically make it a stronger BATNA.

The buyer must adjust Target B for additional costs, delays, risks, and execution uncertainty.

If Target B requires 15 billion dollars of additional integration cost and 24 months of regulatory delay, the buyer should not compare 220 billion dollars with 280 billion dollars directly.

The adjusted alternative value is closer to 235 billion dollars before any time value or execution risk discount is considered.

This calculation forces the buyer to compare real alternatives instead of headline prices.

BATNA and WATNA are useful because they remove emotional pressure from the negotiation table.

The buyer is no longer asking whether the seller is being difficult.

The buyer is asking whether the current deal remains better than the next best path after all costs and risks are included.

A simple BATNA calculation can be written as follows:

Adjusted BATNA value equals alternative purchase price plus incremental transaction cost plus integration cost plus delay cost plus risk adjustment.

This is not a legal formula or a universal valuation rule.

BATNA and WATNA make the buyer compare alternatives on economics rather than slogans.

It is a practical way to prevent false comparisons in acquisition negotiations.

A simple example of BATNA value

Assume a buyer has an alternative acquisition available for 200 billion dollars.

The alternative would take 18 more months to close and require 50 million dollars of advisory fees.

It would also require a new integration team and create additional regulatory review.

The buyer should not treat 200 billion dollars as the full BATNA value.

The better analysis asks what the alternative really costs after delay, fees, opportunity cost, and execution risk.

Once that adjusted value is calculated, the buyer can compare it with the current deal and decide how far it can move on price or terms.

The Opposite Side: Your Worst Alternative

BATNA and WATNA should be used together because the best alternative does not always happen.

A buyer may believe it can acquire another target, but that backup deal might also fail.

The alternative seller may refuse to engage, regulators may delay approval, financing markets may shift, or the target’s board may choose another bidder.

WATNA captures the downside scenario if the current deal fails and the backup path does not materialize.

For a private equity buyer, WATNA might mean returning committed capital without completing a platform acquisition.

For a corporate buyer, WATNA might mean losing a strategic window to a competitor.

For a consolidation strategy, WATNA might mean missing the chance to build scale before market conditions change.

This matters because BATNA alone can make a buyer overconfident.

BATNA and WATNA keep confidence from becoming overreach.

WATNA adds discipline by forcing the deal team to ask what failure really costs.

If the WATNA is severe, the buyer may accept a slightly higher price or stronger seller-friendly protection structure.

If the WATNA is manageable, the buyer can push harder because walking away does not destroy the investment thesis.

This is why negotiation skills BATNA analysis supports should include both the best fallback and the worst realistic outcome.

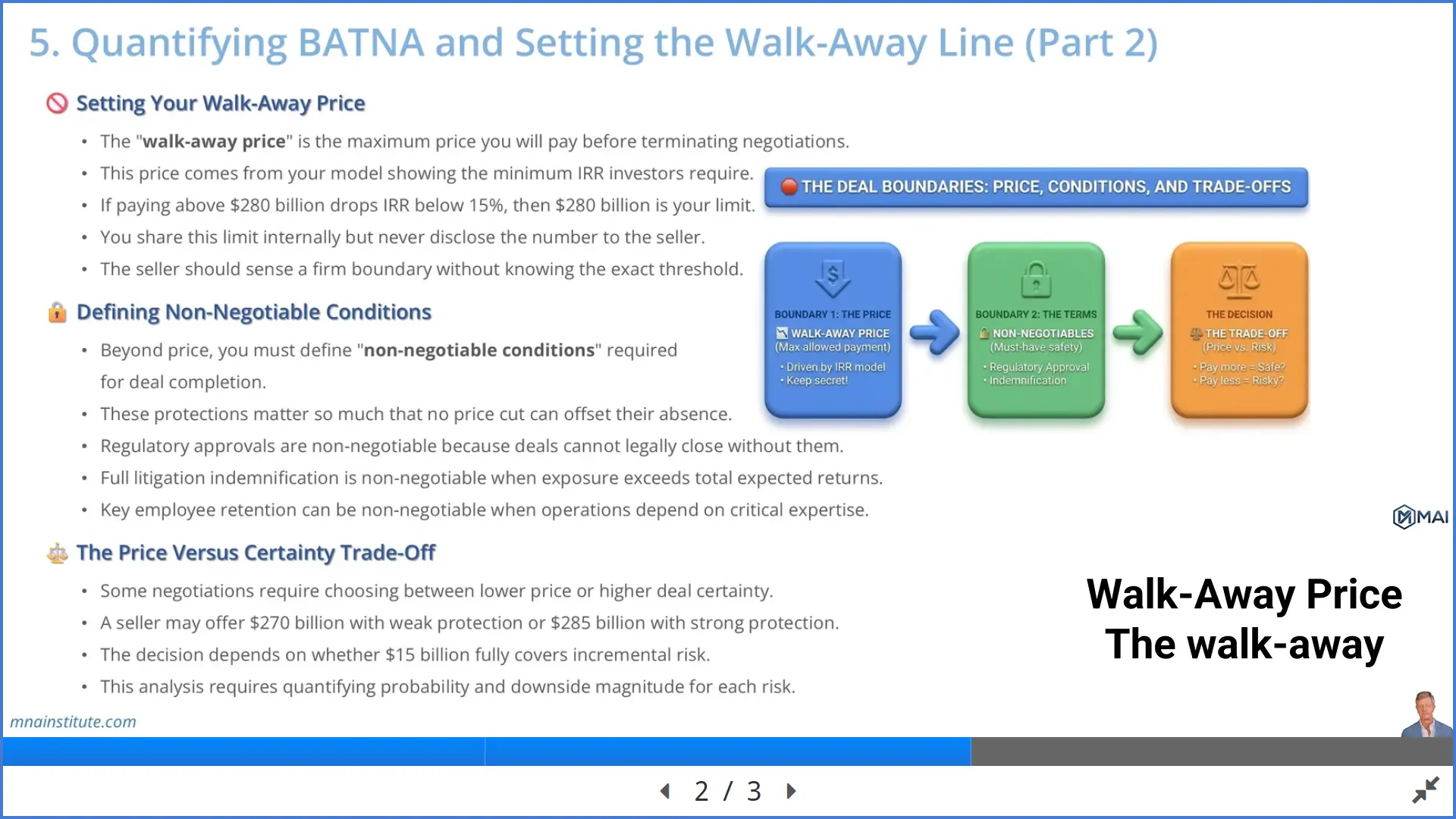

Setting Your Walk Away Price

The walk away price is the maximum amount the buyer will pay before terminating negotiations.

In M&A, this number should come from the financial model, not from a last-minute emotional reaction.

The model should show the price at which the transaction fails to meet the buyer’s minimum return threshold.

If paying more than 280 billion dollars reduces the expected IRR below the investor’s required return, then 280 billion dollars becomes the walk away price.

The buyer should communicate this limit internally and secure investment committee approval before negotiation begins.

BATNA and WATNA help the buyer turn that model output into a firm negotiation rule.

The buyer should not reveal the exact number to the seller.

Revealing the exact walk away price gives the seller a target.

The seller may then push the buyer close to that threshold while extracting other concessions in indemnity, escrow, closing conditions, or employee retention.

A disciplined buyer communicates firmness without disclosing the precise line.

For example, the buyer might say that the investment committee has approved the deal only within defined valuation and risk thresholds.

That sentence signals discipline without giving away the number.

The walk away price should also reflect the adjusted BATNA, the WATNA, and the value of non-price protections.

A buyer might accept a higher price if the seller provides stronger indemnification, cleaner regulatory conditions, or enforceable retention agreements for key employees.

A buyer might reject a lower price if the risk protection is too weak.

That is why BATNA and WATNA are not separate from deal structure.

They sit at the center of price, risk, and certainty.

Defining Non-Negotiable Conditions

BATNA and WATNA should also shape the buyer’s non-price boundaries.

Price is only one boundary in acquisition negotiations.

A buyer also needs non-negotiable conditions that must be satisfied before closing.

These conditions protect the deal thesis when a price reduction cannot solve the problem.

For example, regulatory approval is not a pricing issue if the deal cannot legally close without it.

No discount is useful if the buyer is blocked from completing the transaction.

Known litigation exposure can also become non-negotiable if the downside could exceed the expected return from the deal.

In that situation, the buyer may require full indemnification, a specific escrow, or a separate seller guarantee.

Key employee retention can be another non-negotiable condition.

If the acquired business depends on a small group of engineers, doctors, sales leaders, or product architects, the buyer cannot simply accept a lower price and lose the people who make the business valuable.

The strongest negotiation boundaries usually combine three lines:

- A maximum walk away price tied to the return model.

- A list of non-negotiable closing conditions.

- A clear view of which concessions can be traded without damaging the investment thesis.

BATNA and WATNA help the team decide which line is firm and which line is flexible.

The Price Versus Certainty Trade-Off

A lower price is not always the better deal.

A higher price with stronger protection can sometimes produce a better risk-adjusted outcome.

Consider a seller that offers two options.

Option one is a 270 billion dollar price with limited indemnification and weak conditions precedent.

Option two is a 285 billion dollar price with comprehensive indemnification, regulatory termination protection, and key employee retention agreements.

BATNA and WATNA help the buyer compare price with certainty.

The buyer should not automatically choose the lower price.

The correct question is whether the 15 billion dollar premium is justified by the risk that the stronger protections remove.

This is where BATNA and WATNA become a practical M&A tool rather than a negotiation theory term.

The team should estimate the probability and magnitude of each risk under both structures.

If weak protections create a realistic 40 billion dollar downside, the lower price may be misleading.

If strong protections reduce the probability of major loss and improve closing certainty, the higher price may be rational.

This trade-off also affects how the buyer communicates with the seller.

Instead of saying that the price is too high, the buyer can say that the price only works if specific risk protections remain in the agreement.

That framing keeps the negotiation focused on value and risk rather than emotion.

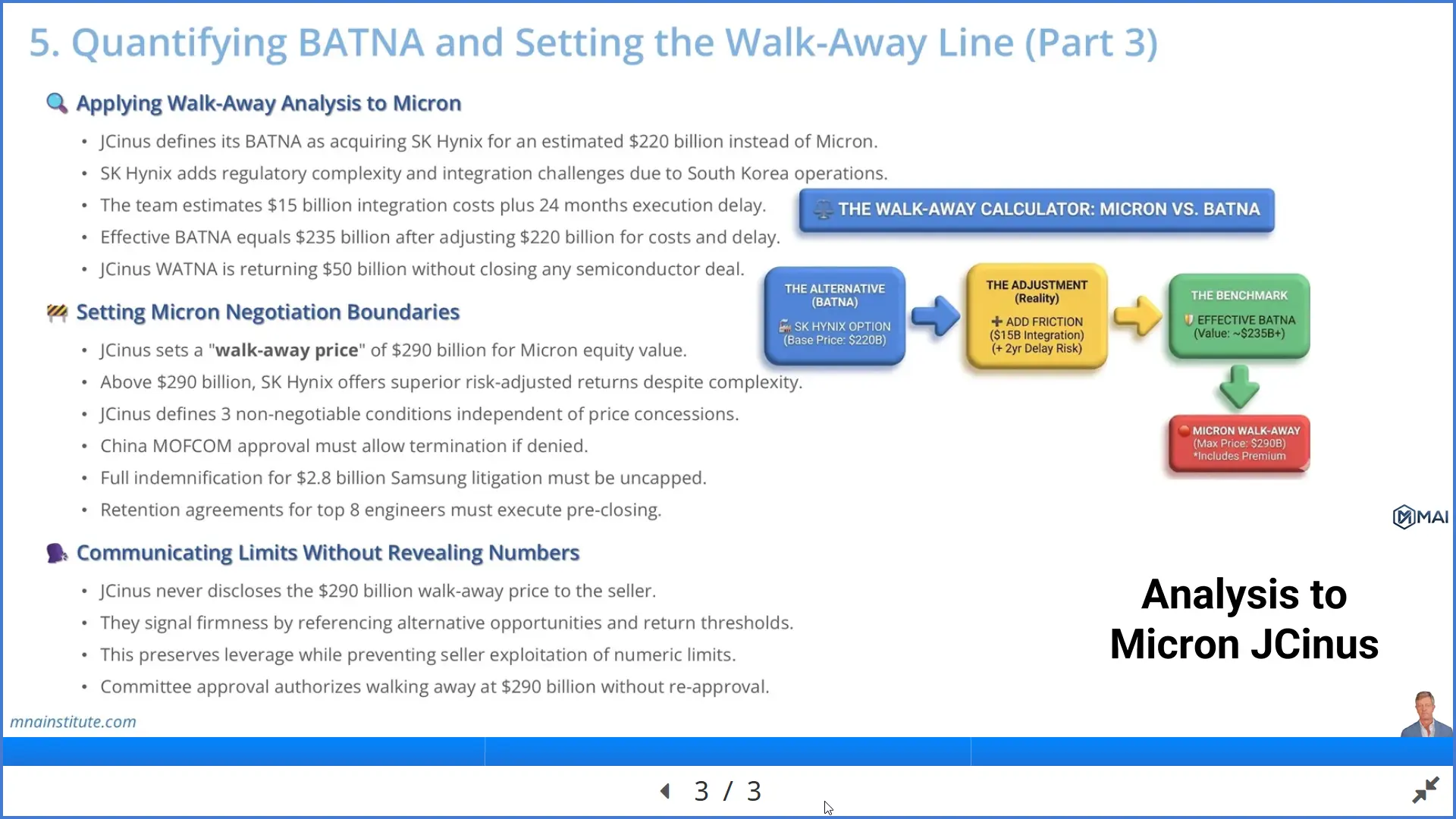

Applying Walk-Away Analysis to Micron

The following financial illustration is hypothetical and is used to explain the framework.

Assume JCinus is evaluating an acquisition of Micron and has identified SK Hynix as its realistic alternative target.

JCinus estimates that acquiring SK Hynix would require 220 billion dollars of equity value.

The alternative appears attractive because it is lower than the price being discussed for Micron.

However, SK Hynix operates primarily in South Korea and would add regulatory complexity, integration challenges, and execution delay.

The deal team estimates an additional 15 billion dollars of integration cost and 24 months of delay.

The effective BATNA value becomes 235 billion dollars before considering further timing and execution risk.

This illustrates how BATNA and WATNA work together in a live deal model.

JCinus also defines its WATNA.

If both the Micron deal and the SK Hynix alternative fail, JCinus may need to return 50 billion dollars to fund investors without completing a semiconductor acquisition during the year.

That WATNA is not catastrophic, but it is commercially unattractive.

The team therefore enters negotiation with a strong alternative but also a clear understanding that delay has a cost.

This is how to calculate BATNA in M&A in a way that is useful for negotiation.

The answer is not only the price of the alternative target.

The answer is the adjusted economic value of the alternative path, including time, cost, risk, and strategic consequences.

Setting Micron Negotiation Boundaries

Based on the adjusted BATNA, the WATNA, and the financial model, JCinus sets its walk away price at 290 billion dollars for Micron equity value.

Above that number, the team believes it earns better risk-adjusted returns by pursuing the SK Hynix alternative despite the extra complexity.

The buyer also defines three non-negotiable conditions that no price reduction can replace.

- China MOFCOM approval must be a condition precedent allowing termination if approval is denied.

- Full indemnification for a known 2.8 billion dollar litigation exposure must be included with no cap.

- Retention agreements for the top 8 semiconductor engineers must be executed before closing.

These conditions are not generic legal preferences.

They protect the deal thesis.

Regulatory approval protects closing certainty.

Litigation indemnification protects downside exposure.

Engineer retention protects operational continuity and technology value.

In BATNA negotiation in M&A, this distinction matters.

A buyer does not define firm lines to sound aggressive.

It defines firm lines because some risks cannot be repaired after closing.

Once the buyer knows which risks are price risks and which risks are deal thesis risks, negotiation becomes clearer.

Communicating Limits Without Revealing Numbers

A buyer should never reveal its exact walk away price unless there is a specific tactical reason to do so.

Most of the time, revealing the number transfers leverage to the seller.

The seller can then ask for the full limit and negotiate away protections in other parts of the agreement.

Instead, the buyer should communicate discipline through language that signals alternatives and internal approval constraints.

For example, the buyer can say that it has alternative opportunities if terms do not meet the approved threshold.

It can also say that the investment committee has approved the transaction only if price, risk allocation, and closing conditions remain within the agreed framework.

This approach maintains tension without disclosing the exact boundary.

The buyer’s internal team should know the exact number.

The seller should know only that the number exists and that the buyer has authority to walk away.

BATNA and WATNA therefore create two types of discipline.

First, they create internal discipline by preventing the deal team from chasing the transaction beyond the approved return threshold.

Second, they create external discipline by showing the seller that the buyer is not dependent on this one deal.

A Practical Checklist for BATNA and WATNA in M&A

The following checklist can be used before entering a serious post-due diligence negotiation.

- Identify the best alternative target or strategy if the current deal fails.

- Estimate the acquisition cost, integration cost, transaction cost, and execution delay of that alternative.

- Adjust the alternative value for regulatory risk, integration risk, and timing.

- Define the WATNA if both the current deal and the alternative fail.

- Calculate the walk away price from the financial model and minimum return threshold.

- List non-negotiable conditions that no price reduction can replace.

- Separate firm demands from tradeable issues before meeting the seller.

- Prepare language that signals firmness without revealing the exact walk away price.

This checklist turns BATNA and WATNA from academic terms into a practical negotiation control system.

BATNA and WATNA should be visible in the model, the investment committee paper, and the negotiation script.

It also helps junior deal team members understand why professional buyers do not negotiate every issue the same way.

Some terms affect price.

Some terms affect closing certainty.

Some terms affect post-closing risk.

Some terms determine whether the deal should continue at all.

Related Courses

The concepts in this article sit naturally inside a broader M&A learning path.

- The Mergers and Acquisitions Online Course covers the full deal journey from strategy and sourcing to diligence, negotiation, closing, and integration.

- The M&A Deal Negotiation Mastery course goes deeper into price, risk allocation, buyer leverage, seller pushback, and deal protection.

- The M&A Due Diligence: CDD, FDD, LDD, & HRDD course explains how buyers identify and validate the issues that later shape negotiation boundaries.

- The Post-Merger Intergration and Value-Up Strategy course connects closing discipline with post-closing execution and value creation.

Sources

- Program on Negotiation at Harvard Law School, What is BATNA? How to Find Your Best Alternative to a Negotiated Agreement.

- Program on Negotiation at Harvard Law School, What is the Reservation Point in Negotiation?

- Investopedia, Understanding BATNA: Your Best Alternative to a Negotiated Deal.