Build a Discounted Cash Flow Model | #1 DCF Modeling Course

A discounted cash flow model is not a spreadsheet trick.

It is a disciplined way to convert business performance into economic value.

When an analyst builds a valuation, the first serious question is not what the market says today.

The first serious question is how much cash the asset can generate for investors over time and what that cash is worth today.

That is why the discounted cash flow model remains the foundation of serious valuation work across corporate finance, investment banking, private equity, infrastructure investing, and capital budgeting.

A listed company, a new factory, a software launch, a toll road, or an acquisition target can all be analysed with the same logic.

The asset may change, but the valuation question remains the same.

Can future cash flow justify the price being paid today.

This article explains what the discounted cash flow model really measures, how the DCF model formula works, which cash flow belongs in the model, and why discounted cash flow analysis is different from relative valuation.

It also shows why a serious DCF modeling course should teach the business logic behind the model, not only the Excel mechanics.

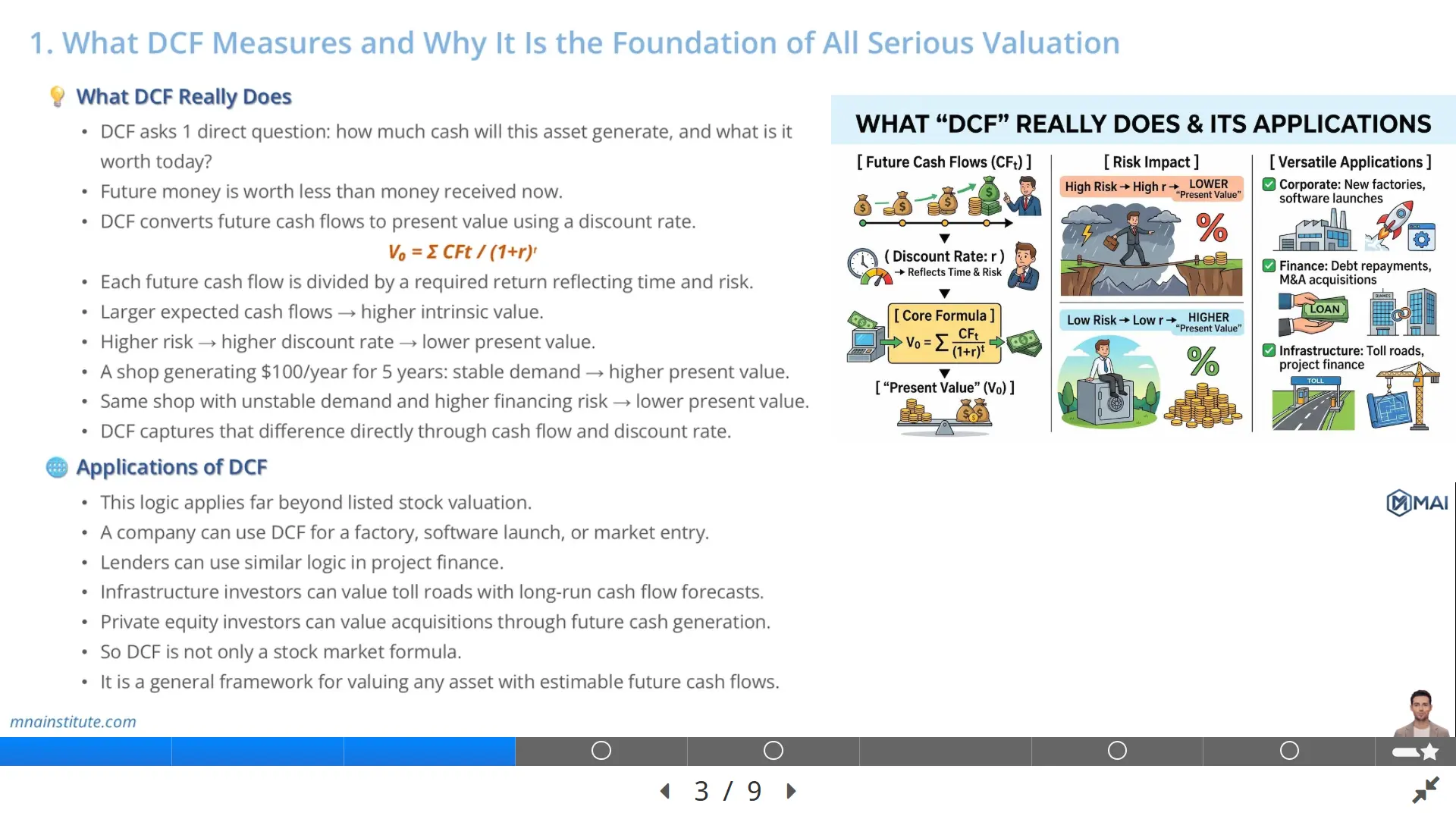

What DCF Really Does

A discounted cash flow model measures the present value of future cash flows.

The concept begins with the time value of money.

Money received today is worth more than the same amount received in the future because today’s money can be invested, used, or protected from risk immediately.

A cash flow expected five years from now must therefore be converted into today’s value before it can be compared with today’s price.

The basic DCF model formula is simple.

V0 = Σ CFt / (1+r)^t

V0 means the value today.

CFt means the cash flow expected in a future period.

r means the discount rate, which reflects required return, time, and risk.

The formula says that each expected cash flow is divided by a discount factor before it is added to the value today.

This is why the discounted cash flow model responds directly to both business performance and risk.

If the business can generate larger cash flows, the value rises.

If the business becomes riskier, the discount rate rises and the present value falls.

For example, imagine a small shop that generates $100 of cash flow every year for five years.

If the shop has stable customers, low rent risk, and predictable operating costs, an investor might use a lower discount rate.

The present value of those future cash flows would be relatively high.

If the same shop depends on a few seasonal customers, faces rising rent, and needs new financing, the investor would require a higher return.

The same $100 annual cash flow would then be worth less today.

The discounted cash flow model captures this difference without needing a peer multiple.

It asks whether the cash flow itself is attractive enough after considering time and risk.

This is also why a DCF can look precise but still be wrong.

The model will always produce a number once inputs are entered.

The quality of the valuation depends on whether the forecast, cash flow definition, and discount rate reflect the business reality.

|

Input |

What the analyst is really claiming |

|

Revenue growth |

The business can sell more volume, charge better prices, or expand into new markets. |

|

Operating margin |

The business can protect profitability after competition, inflation, and scale effects. |

|

Reinvestment |

The business needs a certain amount of working capital and capital expenditure to generate growth. |

|

Discount rate |

Investors require a return that compensates for the risk of those cash flows. |

|

Terminal value |

The business will reach a sustainable long-term cash flow profile after the forecast period |

Applications of DCF Beyond Stock Valuation

Many beginners think the discounted cash flow model is only used for listed equity valuation.

That is too narrow.

Discounted cash flow analysis is a general framework for valuing any asset whose future cash flows can be estimated with reasonable logic.

A corporate development team can use DCF to evaluate whether a new factory creates value.

The forecast would include construction cost, expected production volume, operating margin, maintenance capital expenditure, working capital, and taxes.

If the present value of future free cash flow exceeds the investment required, the project may create value.

A software company can use the same logic to evaluate a new product launch.

The model would forecast subscription revenue, churn, server cost, customer support cost, development spend, and marketing investment.

The question is not simply whether the product grows revenue.

The question is whether the cash flow generated after investment and risk is worth more than the capital committed.

A lender can use similar cash flow logic in project finance.

The lender is not trying to own the entire project forever.

The lender wants to know whether future project cash flow can service debt, interest, and repayment obligations under conservative assumptions.

An infrastructure investor can value a toll road by forecasting traffic volume, toll pricing, operating costs, maintenance spend, concession life, and regulatory risk.

A private equity investor can use a discounted cash flow model to evaluate an acquisition target after operational improvements.

The model might include margin expansion, working capital discipline, cost reduction, pricing initiatives, and a possible exit value.

These examples show why the discounted cash flow model is not only a finance exam topic.

It is a business decision tool.

In a practical DCF modeling course, the analyst should learn to connect the model to real strategic questions.

Will this project return enough cash.

Will this acquisition justify the premium.

Will this business survive the investment required to grow.

Will the risk profile destroy the value that revenue growth appears to create.

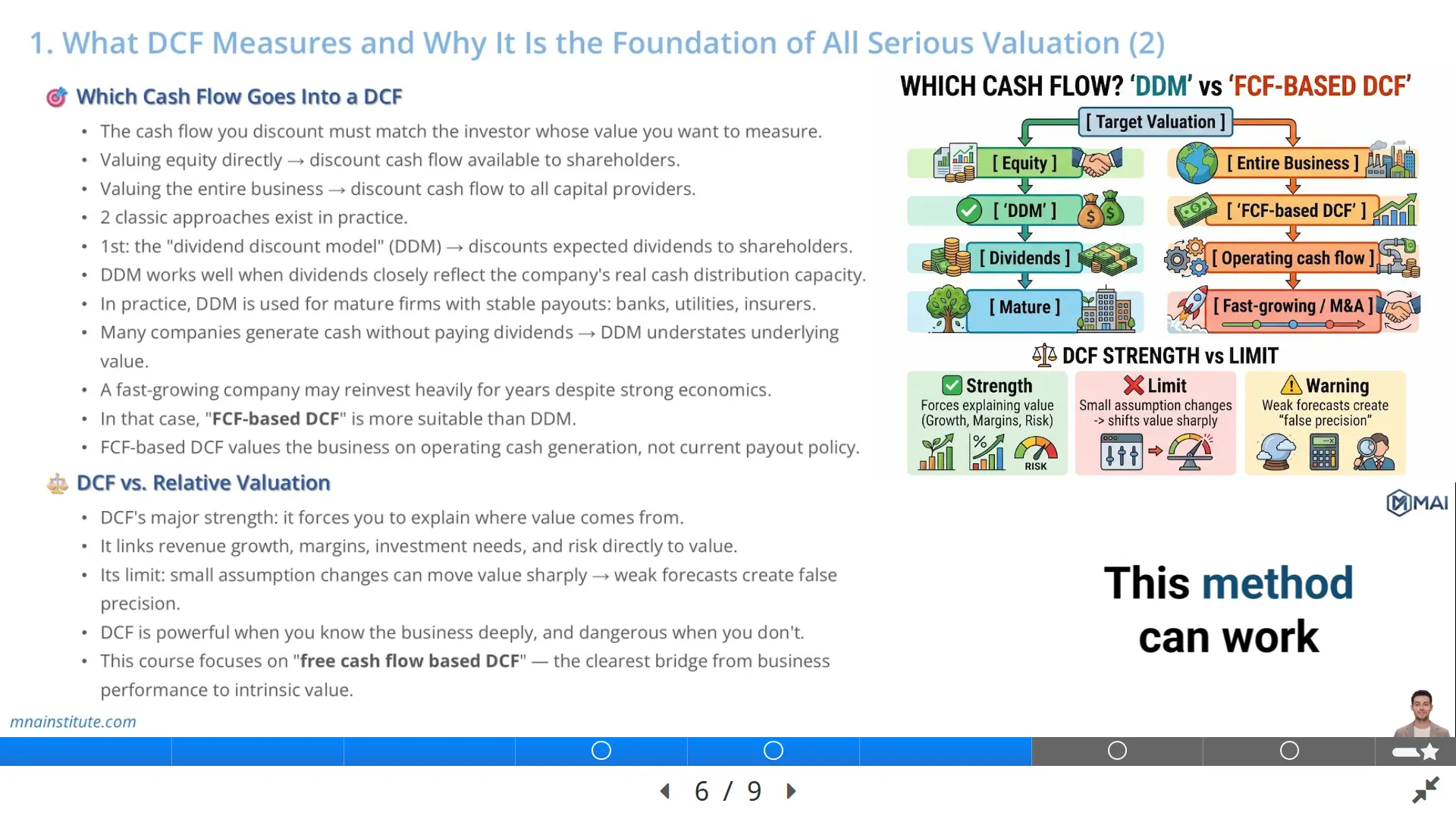

Which Cash Flow Goes Into a DCF

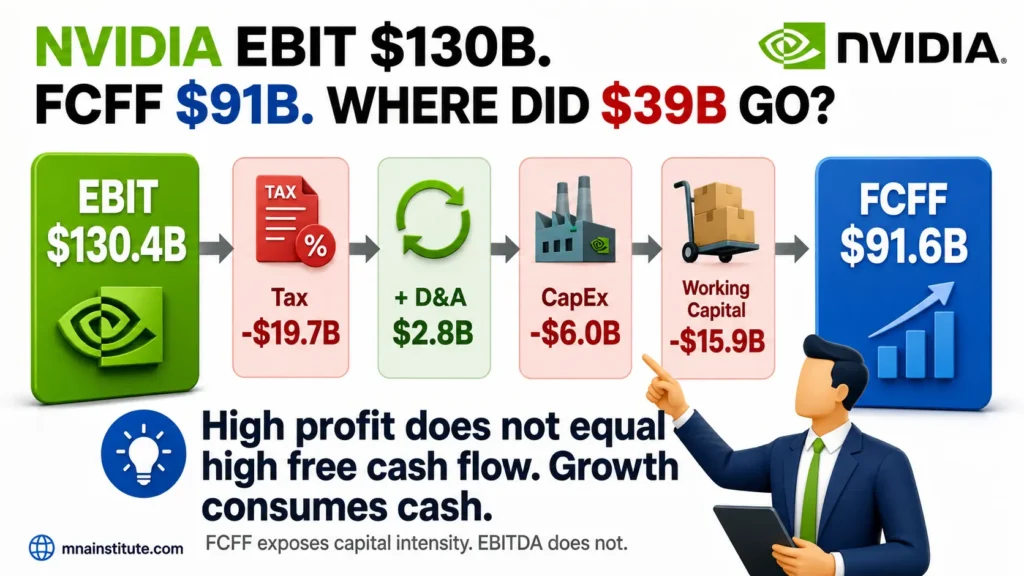

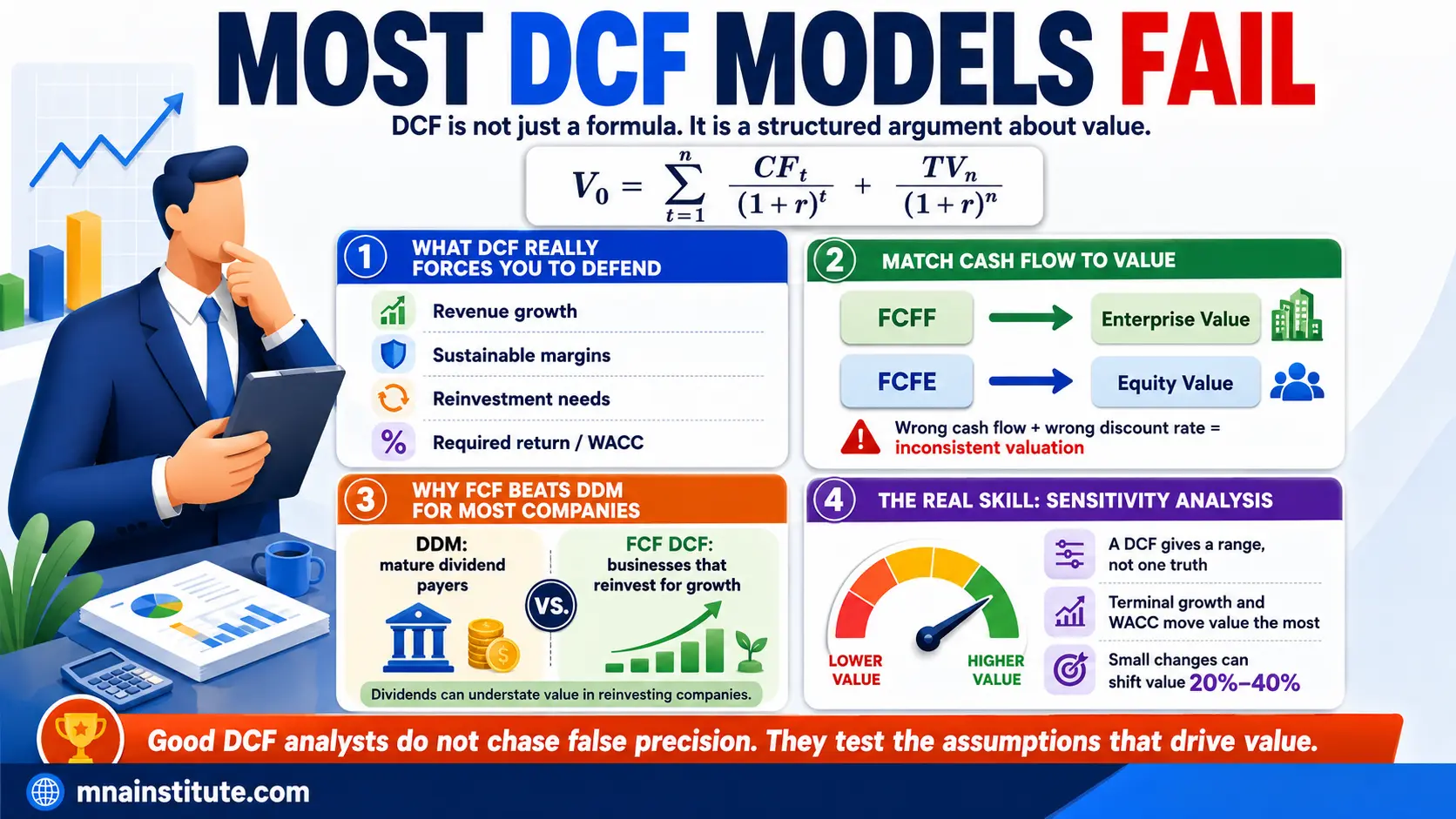

A discounted cash flow model is only as useful as the cash flow definition inside it.

The cash flow being discounted must match the investor whose value is being measured.

If the analyst wants to value equity directly, the model should discount cash flow available to shareholders.

If the analyst wants to value the entire operating business, the model should discount cash flow available to all capital providers.

This distinction explains why two classic approaches appear in valuation practice.

The first approach is the dividend discount model.

The second approach is free cash flow based valuation, which many practitioners informally call DCF.

Dividend Discount Model

The dividend discount model values equity by discounting expected dividends to shareholders.

It can work when dividends closely reflect the company’s real capacity to distribute cash.

This approach can be relevant for mature companies with stable payout policies, such as certain banks, utilities, or insurers.

The logic is clean when the cash paid to shareholders is a good proxy for economic ownership value.

However, dividends are not always a reliable measure of value creation.

A company may generate strong cash flow but retain it for reinvestment.

A fast-growing business may pay no dividend for years even though its economics are attractive.

A company may also pay dividends for policy or signalling reasons even when reinvestment needs are changing.

In those cases, dividend-based valuation may understate or distort the underlying business value.

Free Cash Flow Based Valuation

Free cash flow based valuation focuses on operating cash generation rather than current payout policy.

This is the approach most relevant to corporate acquisitions.

An acquirer does not buy a business only to receive the next declared dividend.

The acquirer wants access to the operating cash flow that the business can generate after paying operating costs, taxes, working capital needs, and reinvestment requirements.

This is why many practitioners focus on free cash flow to the firm when valuing an entire business.

Free cash flow to the firm is the cash flow available to both debt and equity capital providers.

When that cash flow is discounted at a cost of capital, it produces enterprise value.

Equity value can then be derived by adjusting for net debt and other claims.

Free cash flow to equity takes a different ownership perspective.

It measures the cash flow available to common shareholders after debt-related cash flows.

The relevant discount rate is then the cost of equity.

The practical rule is simple.

Cash flow to the firm should be discounted using a firm-level required return.

Cash flow to equity should be discounted using an equity-level required return.

Mixing the wrong cash flow with the wrong discount rate creates a valuation mismatch.

|

Valuation question |

Cash flow to discount |

Typical value measured |

|

What is the entire operating business worth |

Free cash flow to the firm |

Enterprise value |

|

What is the equity worth directly |

Free cash flow to equity or dividends |

Equity value |

|

What is a project worth |

Project free cash flow |

Project value or net present value |

|

Can debt be serviced |

Cash flow available for debt service |

Debt capacity and credit support |

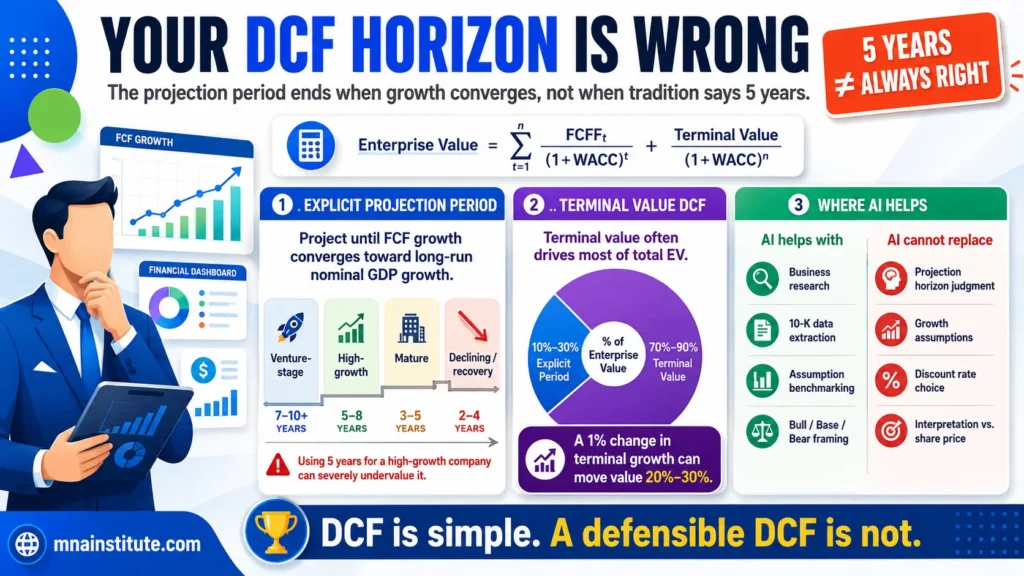

How the DCF Model Formula Connects Cash Flow, Risk, and Value

The DCF model formula looks simple, but each input carries a business judgment.

The numerator is the expected cash flow.

The denominator is the discount factor that converts that future cash flow into present value.

For a one-year cash flow, the formula is easy to see.

Present value equals next year’s cash flow divided by 1 plus the discount rate.

For cash flows across many years, each year is discounted separately and then added together.

This structure matters because time changes value.

A cash flow expected next year is not treated the same as a cash flow expected ten years from now.

The further away the cash flow is, the more sensitive it becomes to the discount rate.

That is why terminal value can become a large part of a DCF valuation.

If most value comes from distant cash flows, small changes in long-term growth or discount rate can move valuation sharply.

A simple numerical example makes the logic clear.

Assume a business will generate $100 of free cash flow next year and the required return is 10%.

The present value of that one-year cash flow is $90.91.

If the same cash flow arrives five years from now, its present value at 10% is about $62.09.

The cash flow amount is unchanged, but the timing is different.

That is why discounted cash flow analysis forces analysts to think about when cash arrives, not only how much cash arrives.

Risk also changes value.

If the required return rises from 10% to 15%, the five-year present value of the same $100 falls to about $49.72.

The business did not generate less nominal cash.

The investor simply required a higher return for bearing greater uncertainty.

This is why the discounted cash flow model is a bridge between operations and capital markets.

Revenue growth, margins, reinvestment, and tax affect cash flow.

Business risk, financing risk, market risk, and investor alternatives affect the discount rate.

A good analyst does not treat these as mechanical inputs.

A good analyst explains why each input belongs in the model.

DCF vs. Relative Valuation

Relative valuation estimates value by comparing a company with similar companies or transactions.

Common metrics include enterprise value to EBITDA, enterprise value to revenue, price to earnings, and price to book value.

Relative valuation is useful because it reflects current market pricing and can be completed quickly when comparable data is available.

It also helps analysts test whether a DCF output is far away from the market’s view of similar assets.

However, relative valuation does not fully explain where intrinsic value comes from.

A company may trade at 12 times EBITDA because the market likes its growth profile, margin stability, asset quality, or capital efficiency.

The multiple itself does not explain the economics.

The discounted cash flow model forces the analyst to build that explanation directly.

It asks how revenue will grow, what margin the business can sustain, how much reinvestment is required, and what risk investors must be compensated for.

This is the main strength of discounted cash flow analysis.

It does not simply ask what others are paying.

It asks whether the asset can generate enough cash to justify the value.

That strength is also a weakness when the forecast is poor.

Small changes in revenue growth, margin, reinvestment, discount rate, or terminal value can create large changes in output.

A weak forecast can create false precision.

The spreadsheet may appear professional even when the assumptions are not defensible.

That is why the discounted cash flow model is powerful in the hands of someone who understands the business and risky in the hands of someone who only knows the formula.

For M&A, the difference matters.

An acquisition price often includes a control premium, synergy expectations, financing constraints, and integration risk.

A relative valuation may show what similar companies trade for today.

A discounted cash flow model can test whether the buyer’s specific plan for cash generation supports the actual price being paid.

That is why a serious valuation process usually uses both methods.

Relative valuation gives a market reference point.

The discounted cash flow model gives a cash-flow-based view of intrinsic value.

|

Method |

Main question |

Strength |

Weakness |

|

Discounted cash flow model |

What are future cash flows worth today |

Links value to business performance and risk |

Highly sensitive to assumptions |

|

Relative valuation |

What do similar companies trade for |

Fast market-based reference |

Can hide weak business logic behind market multiples |

|

Dividend discount model |

What are expected dividends worth today |

Clear for stable dividend payers |

Less useful when payout policy understates economic value |

How to Build a DCF Model From Business Logic

Many people search for how to build a DCF model and expect an Excel template.

A template helps, but the real work starts before the spreadsheet.

The analyst must first understand the business model.

How does the company make money.

What drives volume, price, customer retention, and market share.

Which costs are fixed, which costs are variable, and which costs scale with revenue.

How much capital must the business reinvest to support growth.

What risks could reduce future cash flow or increase the required return.

Only after answering those questions should the analyst build the model.

A practical build sequence looks like this.

- Define the valuation perspective, such as enterprise value or equity value.

- Forecast revenue using business drivers rather than a blind growth percentage.

- Forecast operating costs and margins based on competitive position and operating leverage.

- Estimate taxes, working capital, and capital expenditure needed to support the forecast.

- Calculate free cash flow using a consistent definition.

- Choose a discount rate that matches the cash flow being discounted.

- Estimate terminal value based on a sustainable long-term business profile.

- Run sensitivity analysis to test which assumptions drive value.

This sequence keeps the discounted cash flow model connected to economics.

For example, suppose a software company grows revenue from $100 million to $150 million over five years.

That growth alone does not prove value creation.

If sales and marketing spend must rise faster than revenue, if customer churn worsens, or if hosting costs increase, free cash flow may not improve.

The discounted cash flow model should capture those operating realities.

Now suppose the same company grows from $100 million to $150 million while improving gross margin, reducing customer acquisition cost, and keeping capital expenditure light.

The same revenue growth becomes much more valuable because the business converts more revenue into cash.

This is the analytical mindset behind a strong DCF modeling course.

The objective is not to fill cells.

The objective is to explain how business performance becomes intrinsic value.

Common Mistakes in Discounted Cash Flow Analysis

The first mistake is using an accounting profit measure when the valuation requires cash flow.

Net income is useful, but it includes non-cash expenses and may not reflect working capital and capital expenditure needs.

The second mistake is mismatching cash flow and discount rate.

A firm-level cash flow should not be discounted using only the cost of equity.

An equity-level cash flow should not be discounted using a firm-level capital cost without adjustment.

The third mistake is treating terminal value as a plug number.

Terminal value should reflect a mature business profile, not a way to force the model to reach a desired output.

The fourth mistake is ignoring reinvestment.

Growth usually requires working capital, capital expenditure, product development, or customer acquisition spend.

Revenue growth without reinvestment logic often creates overstated free cash flow.

The fifth mistake is presenting one valuation number without sensitivity analysis.

DCF output depends heavily on assumptions.

A professional valuation should show how value changes when discount rate, terminal growth, margins, or reinvestment assumptions change.

These mistakes explain why the discounted cash flow model can be both useful and dangerous.

It is useful because it forces explicit assumptions.

It is dangerous because weak assumptions can still produce a precise number.

Where This Fits in M&A Institute Courses

The discounted cash flow model sits at the center of practical valuation training.

It connects financial statement analysis, forecasting, WACC, free cash flow, terminal value, and investment decision-making.

- In the Financial Modeling and Valuation Course with AI and Excel, learners build the valuation logic from business performance and translate it into a professional model.

- The Financial Modeling Course with AI for Equity Research helps connect accounting data, ratio analysis, and investment conclusions.

- The 3-Statement Financial Modeling Course with AI develops the financial statement mechanics that feed into free cash flow forecasts.

- The Mergers and Acquisitions Online Course applies valuation logic to deal rationale, acquisition pricing, due diligence, and post-closing value creation.

- The M&A Due Diligence Course helps analysts test whether the assumptions inside a valuation model are supported by evidence.

- The Post Merger Integration Course connects acquisition valuation with execution, because a deal only creates value if the forecasted cash flow improvements can actually be delivered.

These courses are linked by one practical idea.

Valuation is not only about knowing a formula.

It is about proving whether a business can generate enough cash, at an acceptable level of risk, to justify the capital committed today.

Sources

The following external references were used to support the valuation concepts discussed in this article.

- CFA Institute, Free Cash Flow Valuation

- Aswath Damodaran, Discounted Cash Flow Valuation

- Investopedia, Discounted Cash Flow Explained With Formula