DCF Model Formula: 3 AI for Financial Modelling Parts

Why the DCF Model Formula Must Be Understood Before Excel Opens

Many analysts begin valuation by opening a spreadsheet and projecting revenue before they have understood the architecture of the model.

That is where many discounted cash flow mistakes begin.

The DCF model formula looks compact, but it contains several linked judgments about free cash flow, WACC, terminal value, projection horizon, capital intensity, and the bridge from enterprise value to equity value.

If those pieces are not understood before the model is built, the spreadsheet can become mechanically correct but economically weak.

A serious valuation starts by asking what the business must look like before the terminal value assumption becomes defensible.

That question matters especially for companies like NVIDIA, where current growth and returns can be exceptional, but long-run growth must eventually converge toward a more sustainable level.

The purpose of this article is to explain the DCF model formula as a structure, not as a memorized equation.

It also explains where AI for financial modelling can help an analyst move faster and where the analyst must still make the final judgment.

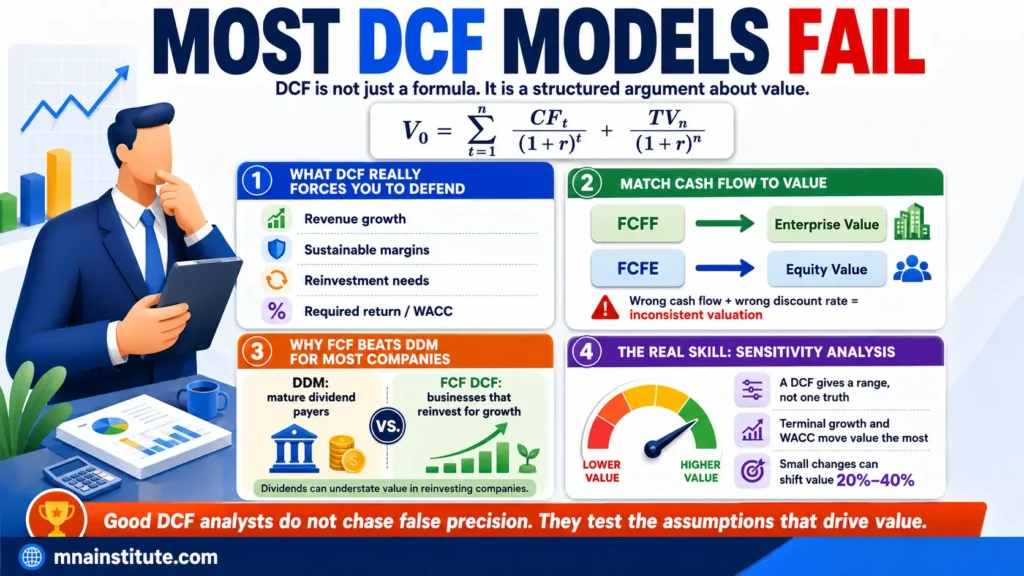

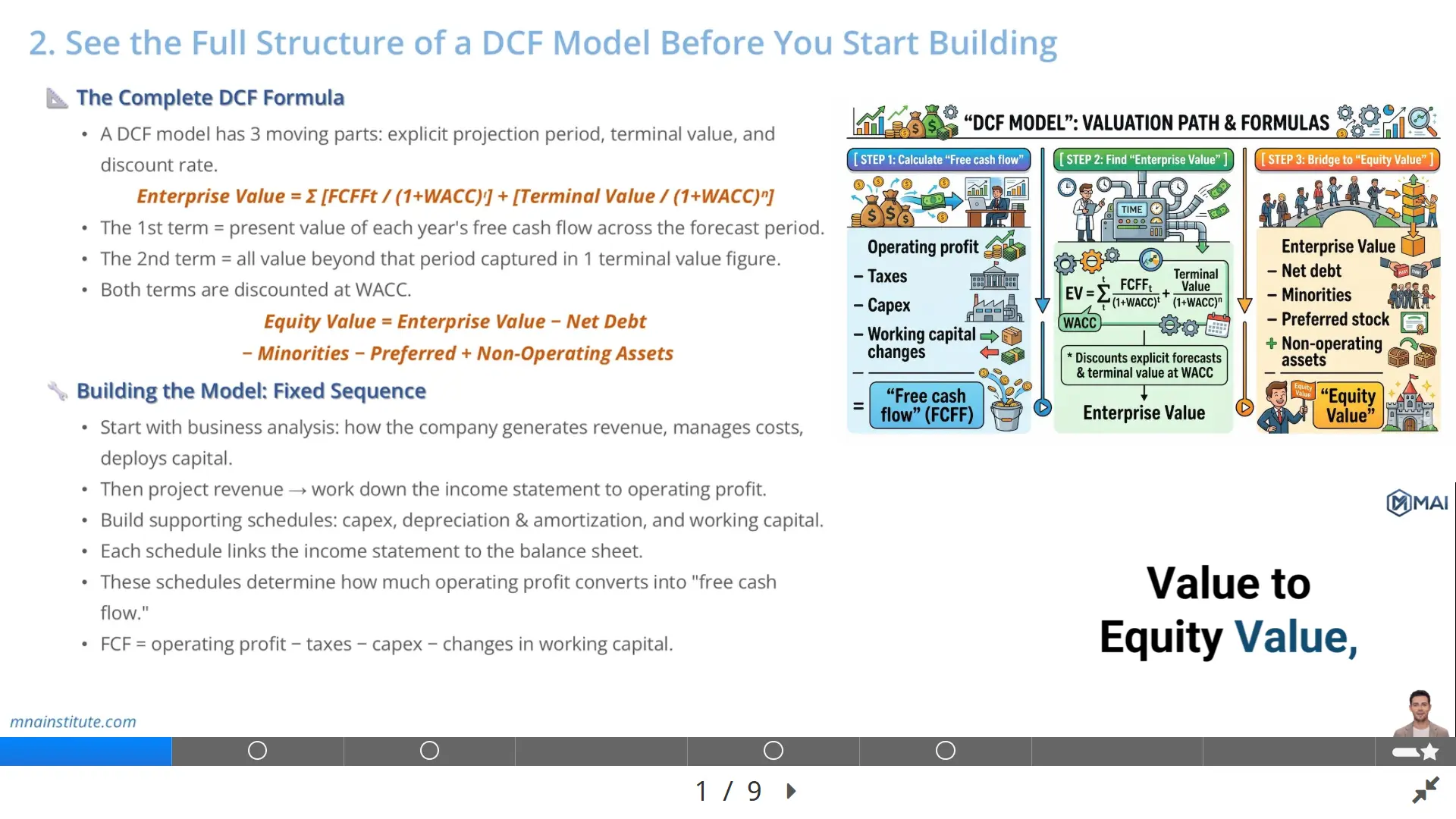

The Complete DCF Model Formula

A DCF model has three moving parts: the explicit projection period, the terminal value, and the discount rate.

The discounted cash flow formula for an enterprise value DCF can be written as follows.

Enterprise Value = Sum of FCFF in year t divided by 1 plus WACC raised to year t, plus Terminal Value divided by 1 plus WACC raised to year n

The first part captures the present value of each year of free cash flow to the firm during the explicit forecast period.

The second part captures all cash flows beyond the explicit forecast period in one terminal value figure.

Both parts are discounted back to today using WACC, because FCFF belongs to all capital providers, including debt and equity investors.

The DCF model formula is therefore not only a math formula.

It is a disciplined way to connect operating forecasts to enterprise value.

CFA Institute describes discounted cash flow valuation as valuing a security based on the present value of expected future cash flows, including FCFF and FCFE approaches for company valuation.

That framing is useful because it reminds analysts that DCF begins with future economic benefits, not accounting earnings alone.

The enterprise value output is not yet the value of the common equity.

To move from enterprise value to equity value, the analyst adjusts for financing claims and non-operating assets.

The bridge can be written as follows.

Equity Value = Enterprise Value – Net Debt – Minority Interests – Preferred Stock + Non-Operating Assets

This bridge prevents a common beginner mistake: assuming that enterprise value and equity value are interchangeable.

For example, suppose a company has an enterprise value of 100 billion dollars, net debt of 12 billion dollars, minority interests of 2 billion dollars, preferred stock of 1 billion dollar, and excess cash or non-operating investments of 3 billion dollars.

Its equity value would be 88 billion dollars.

The implied share price would then depend on diluted shares outstanding, not enterprise value alone.

This is why a DCF model formula must be understood as a full valuation chain from operating cash flow to shareholder value.

How the Model Is Built in Sequence

Building the model follows a fixed economic sequence even when the Excel layout differs by firm or analyst style.

First, the analyst studies the business model.

This means understanding how the company generates revenue, which products drive growth, which customers matter, how gross margin behaves, and how much capital must be reinvested to sustain growth.

Second, the analyst projects revenue and moves down the income statement to operating profit.

Third, the analyst builds supporting schedules for capital expenditure, depreciation and amortisation, and working capital.

These schedules connect the income statement to the balance sheet.

They also determine how much operating profit converts into free cash flow.

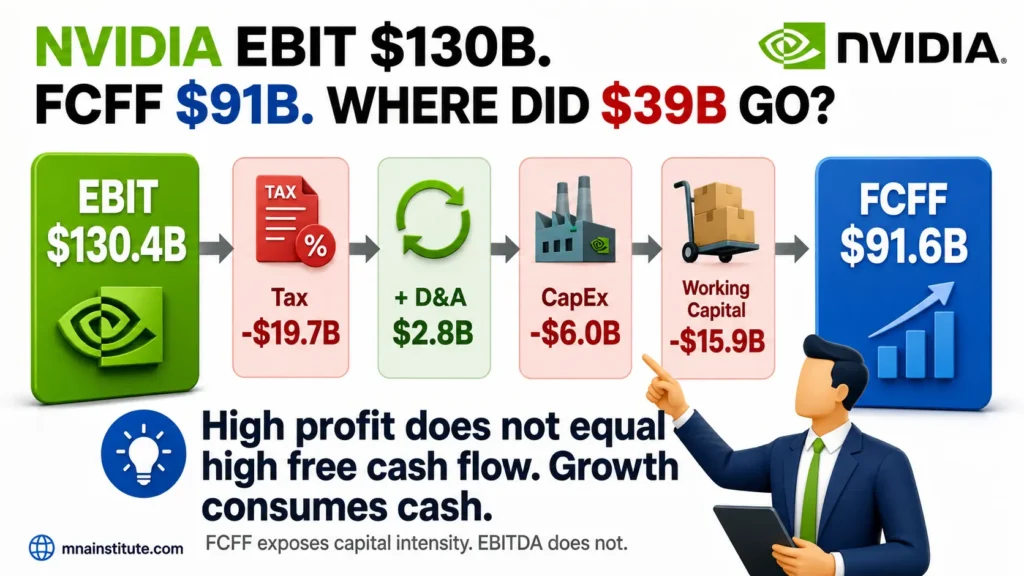

Free cash flow to the firm is usually built from after-tax operating profit, then adjusted for depreciation and amortisation, capital expenditure, and changes in working capital.

The concept is simple: a company is valuable because it can generate cash after paying taxes and reinvesting enough to maintain and grow the business.

The DCF model formula converts that future cash into present value.

The Three Core Parts of the DCF Model Formula

|

Part |

What it does |

Main judgment |

|

Explicit forecast period |

Models yearly FCFF directly. |

How long the business needs to reach sustainable growth. |

|

Terminal value DCF |

Captures value beyond the explicit forecast period. |

Whether the company is mature enough for a stable long-run assumption. |

|

Discount rate |

Discounts FCFF and terminal value to present value. |

Whether WACC reflects the risk of the operating cash flows. |

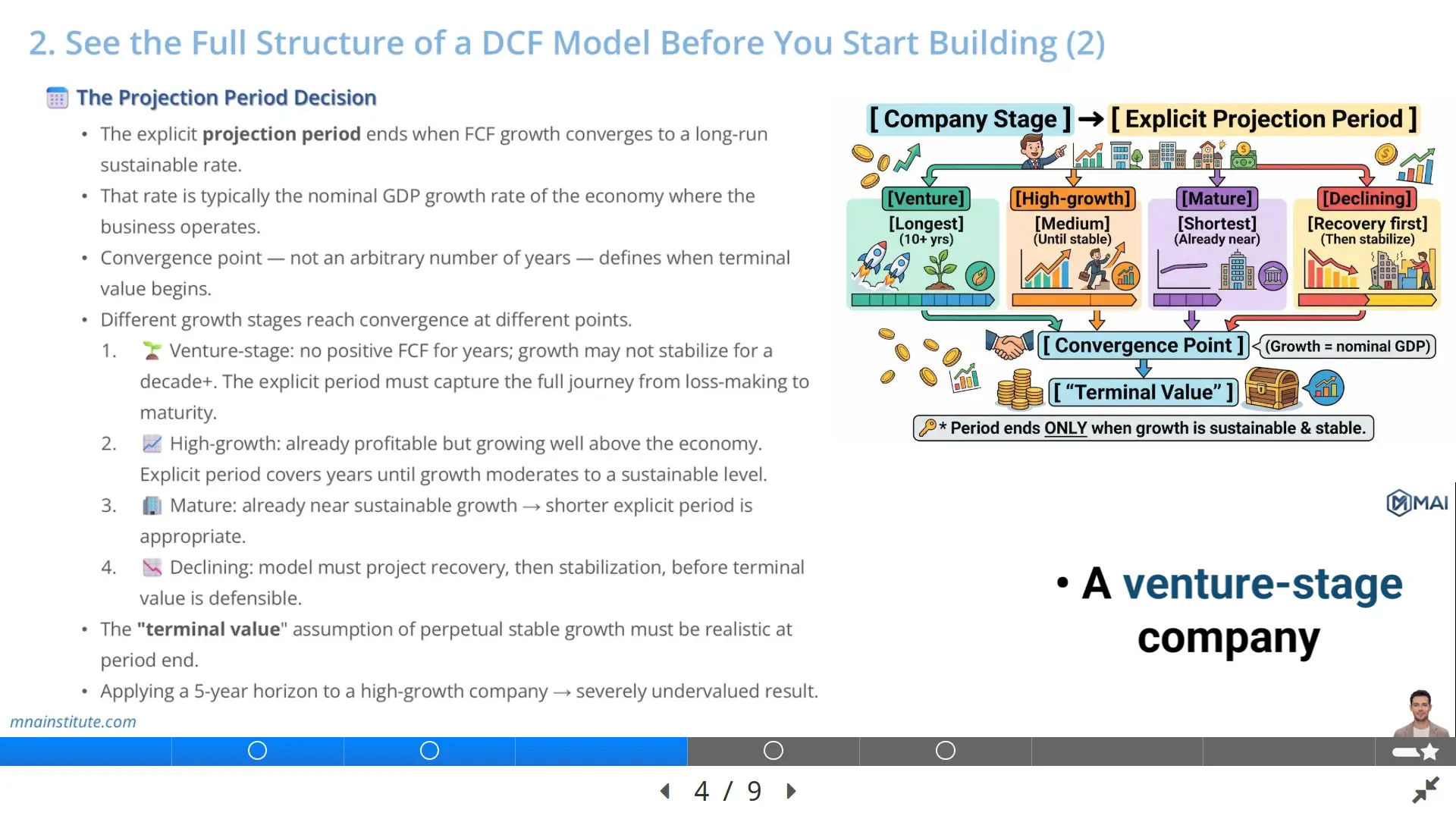

The Projection Period Decision

The projection period is one of the most underestimated decisions in DCF modelling.

Many beginners use five years because a template uses five years.

That is not valuation logic.

The explicit projection period should extend until free cash flow growth converges toward a long-run sustainable rate.

That sustainable rate is often anchored around the nominal GDP growth rate of the economy in which the business operates, adjusted for the company, sector, and market context.

The convergence point, not an arbitrary number of years, defines when the explicit period ends and terminal value begins.

This point is essential to the terminal value DCF because terminal value assumes the company has reached a stable phase.

If the company has not reached a stable phase, the terminal value assumption becomes a shortcut rather than a valuation conclusion.

Damodaran explains that terminal value in a discounted cash flow model should be estimated using a liquidation value or a stable growth model, which reinforces the need to think carefully about what stable growth means.

Why One Projection Period Does Not Fit All Companies

A venture-stage company may not generate positive free cash flow for several years.

Its explicit period may need to capture revenue scaling, margin expansion, capital investment, and eventual cash flow stabilization.

A high-growth company may already be profitable but still grow well above the economy.

Its explicit period should cover the period during which growth moderates from extraordinary growth toward a sustainable long-run level.

A mature company may already operate close to sustainable growth.

A shorter explicit forecast period can be appropriate because the business is already near its steady-state economics.

A declining company requires a different approach.

The analyst may need to model a recovery phase, a restructuring phase, and then a stabilization phase before the terminal value assumption becomes credible.

This distinction is central to the DCF model formula because terminal value is not a plug number.

It is the mathematical expression of a long-run business state.

A Simple Example of Projection Period Logic

Assume two companies both generate 1 billion dollars of current free cash flow.

Company A is a regulated utility growing close to inflation and GDP.

Company B is an AI infrastructure supplier growing revenue far above the broader economy while reinvesting heavily in capacity and research.

A five-year forecast may be reasonable for Company A if cash flow growth is already close to a stable level.

The same five-year forecast may be too short for Company B if growth, margin, and reinvestment are still far from steady state.

Using an early terminal value for Company B could undervalue the business if the model cuts off the high-growth transition too soon.

It could also overvalue the business if the terminal value assumes high growth can continue forever.

The correct answer is not automatically longer or shorter.

The correct answer depends on when the company reaches economics that can support a stable terminal value DCF assumption.

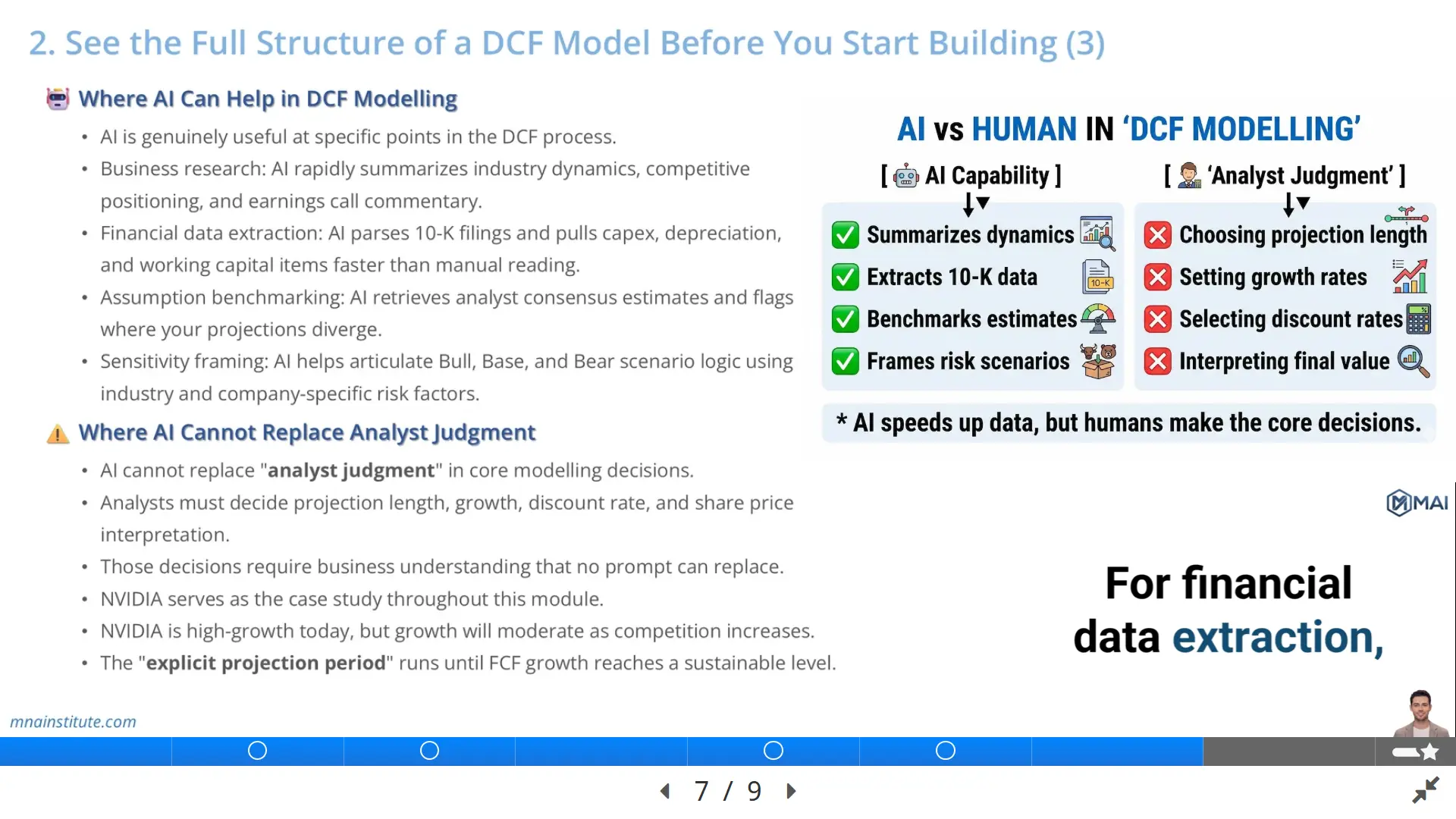

Where AI Can Help in DCF Modelling

AI for financial modelling is useful when the analyst knows exactly what task should be delegated to the tool.

The strongest use cases are research acceleration, data extraction, assumption benchmarking, and scenario framing.

AI can summarize industry dynamics, competitive positioning, customer demand trends, and recent management commentary from earnings calls.

This research helps anchor revenue growth, margin direction, and reinvestment assumptions.

AI can also parse 10-K filings and pull specific line items such as capital expenditure, depreciation schedules, lease commitments, segment revenue, and working capital components.

This saves time when the analyst needs to populate historical inputs before building a forecast.

IBM describes AI financial modeling as using AI-powered tools to transform how financial data is analyzed and forecasts are produced.

That is the right framing for valuation work, because AI can support the workflow but should not own the valuation conclusion.

AI in Business Research and Assumption Benchmarking

In business research, AI can quickly summarize product segments, market growth, competitive pressure, supply chain constraints, and management guidance.

For a company like NVIDIA, AI can help organize commentary on data center demand, gaming cycles, cloud capex, supply constraints, export controls, and competition in accelerator chips.

The analyst can then decide which points are relevant to revenue growth, gross margin, operating leverage, and capital intensity.

For assumption benchmarking, AI can compare analyst forecasts against consensus estimates or recent management guidance.

It can flag when the analyst forecast is far above or below market expectations.

A flagged assumption is not automatically wrong.

It simply tells the analyst where the investment thesis must be explicit.

For example, if consensus expects revenue growth to decline sharply after three years but the model assumes growth remains elevated for seven years, the analyst must explain why.

That explanation may come from product cycle analysis, customer contracts, capacity constraints, market share assumptions, or pricing power.

AI in Sensitivity and Scenario Framing

AI for financial modelling can also help build the narrative around Bull, Base, and Bear cases.

The tool can summarize risks that support the Bear case, such as margin compression, customer concentration, regulatory restrictions, slower AI infrastructure spending, or rising competition.

It can also organize upside drivers for the Bull case, such as stronger demand, faster adoption, higher pricing, improved supply, or broader product penetration.

The analyst still chooses the assumptions.

AI helps make the scenarios structured, internally consistent, and easier to explain.

This is particularly useful in valuation memos where the investment committee needs to understand not only the base case output but also the risk range around that output.

Where AI Cannot Replace Analyst Judgment

AI cannot decide the core valuation judgments inside the DCF model formula.

It cannot decide how long the explicit projection period should be.

It cannot decide whether a terminal growth rate is defensible.

It cannot decide whether WACC reflects the real risk of the cash flows.

It cannot decide whether the implied share price creates enough margin of safety against the current market price.

Those decisions require business judgment, investment judgment, and valuation judgment.

A prompt can produce an assumption, but it cannot own the responsibility for that assumption.

The NVIDIA Case Logic

NVIDIA is a useful case because it forces the analyst to separate current excellence from long-run valuation discipline.

A high-growth company can generate exceptional returns today and still require a careful convergence assumption.

The AI infrastructure build-out cycle may support strong demand for several years.

At the same time, competition, customer bargaining power, export restrictions, supply constraints, and cloud capex cyclicality can eventually moderate growth.

A DCF model for NVIDIA therefore cannot jump from current high growth directly into a stable terminal value unless the explicit forecast period shows that transition.

The model must cover the years between today’s high growth and the point where free cash flow growth converges toward a sustainable long-run rate.

That is the practical meaning of seeing the full structure before building.

How to Use AI Without Losing Control of the Model

A disciplined analyst can use AI in four steps.

First, ask AI to summarize the business and industry drivers that could affect revenue, margins, and reinvestment.

Second, ask AI to extract historical data from filings, then verify every line item against the source document.

Third, ask AI to compare assumptions against consensus or peer patterns, then decide whether the divergence is justified.

Fourth, ask AI to help write the valuation narrative, but only after the model logic has been reviewed.

This approach keeps AI for financial modelling in the right place.

It accelerates research and communication while preserving analyst control over the valuation decision.

A Practical Checklist Before You Build the DCF Model

Before opening Excel, the analyst should be able to answer the following questions.

- What business drivers will determine revenue growth.

- Which margins are structurally sustainable and which reflect temporary conditions.

- How much reinvestment is required to support the forecast.

- When free cash flow growth is likely to converge toward a sustainable long-run rate.

- What terminal value DCF method fits the company’s maturity and stability.

- What WACC should discount the operating cash flows.

- How enterprise value will bridge to equity value.

- Where AI can help with research, extraction, benchmarking, and scenario framing.

- Which valuation judgments must remain human decisions.

This checklist turns the DCF model formula from a memorized expression into a practical valuation workflow.

If the change comes from WACC or FCFF, the DCF model formula directs the review back to risk, reinvestment, and operating assumptions.

If the change comes mainly from terminal value, the analyst should test whether the terminal value DCF assumption is doing too much work.

If enterprise value moves sharply, the analyst should check which part of the DCF model formula caused the movement.

The DCF model formula also gives the analyst a review sequence for model auditing.

It also reduces the risk that AI outputs become unverified assumptions inside a sensitive valuation model.

That is why the best valuation process starts with business logic, then model structure, then Excel execution.

The DCF model formula protects against these errors only when the analyst understands what each component represents.

The fourth error is moving from enterprise value to share price without adjusting for net debt, minority interests, preferred stock, and non-operating assets.

That mismatches the cash flow with the capital provider whose required return is being used.

The third error is discounting FCFF at the cost of equity instead of WACC.

This can make terminal value DCF either too aggressive or too conservative.

The second error is ending the forecast period before the company has reached a stable economic profile.

A company can report strong operating profit while consuming cash through working capital, capital expenditure, or tax payments.

The first error is using accounting profit as if it were free cash flow.

A structured view of DCF helps prevent several valuation errors.

Common Errors the Structure Helps Prevent

When the analyst understands the DCF model formula first, AI becomes a productivity tool rather than a hidden source of modelling risk.

The better approach is to let AI for financial modelling handle repetitive research and organization while the analyst controls the valuation logic.

AI may also summarize analyst consensus, but it cannot tell you whether consensus is too optimistic or too conservative without a business thesis.

For example, AI may extract capital expenditure from a 10-K correctly but misunderstand whether a one-time purchase should be treated as recurring reinvestment.

The analyst still needs to check whether the source data is correct, whether the assumptions are economically consistent, and whether the resulting enterprise value makes sense against market evidence.

AI for financial modelling can speed up this example by extracting historical FCFF inputs, summarizing WACC assumptions, or drafting a sensitivity table.

What the DCF Formula Looks Like in Practice

The DCF model formula becomes easier to understand when each number is tied to an operating question.

Assume a company is expected to generate FCFF of 100 million dollars next year, then 120 million dollars in year two, and 140 million dollars in year three.

Assume the WACC is 10 percent and the terminal value at the end of year three is 1.8 billion dollars.

The discounted cash flow formula does not add those figures directly.

It discounts each yearly free cash flow and the terminal value back to present value.

Year one FCFF is divided by 1.10.

Year two FCFF is divided by 1.10 raised to the second year.

Year three FCFF and the terminal value are divided by 1.10 raised to the third year.

The sum of those present values becomes enterprise value before the bridge to equity value.

After that bridge, net debt, minority interests, preferred stock, and non-operating assets determine how much value belongs to common shareholders.

This simple example shows why the discount rate and terminal value DCF assumption can move valuation more than one extra forecast year.

It also shows why the projection period decision cannot be separated from the terminal value assumption.

How AI for Financial Modelling Should Be Checked

AI for financial modelling can speed up the example by extracting historical FCFF inputs, summarizing WACC assumptions, drafting a sensitivity table, and organizing source evidence.

That support is useful only when the analyst checks the output against the DCF model formula and the company economics.

A model can look polished while still using an unrealistic projection period, an unsupported terminal growth rate, or a WACC that does not match the risk of the cash flows.

AI may extract capital expenditure from a 10-K correctly but misunderstand whether a one-time purchase should be treated as recurring reinvestment.

AI may summarize analyst consensus, but it cannot decide whether consensus is too optimistic or too conservative without a business thesis.

The analyst still needs to check whether the source data is correct, whether the assumptions are economically consistent, and whether the resulting enterprise value makes sense against market evidence.

When the analyst understands the DCF model formula first, AI becomes a productivity tool rather than a hidden source of modelling risk.

The better approach is to let AI for financial modelling handle repetitive research and organization while the analyst controls the valuation logic.

Related Courses

These courses connect naturally to the modelling and valuation workflow discussed above.

- Financial Modeling and Valuation Course with AI and Excel: A complete valuation learning path covering financial statement analysis, three-statement modelling, WACC, DCF, CCA, and valuation report writing.

- Financial Modeling Course with AI for Equity Research: A practical foundation for analyzing filings, extracting financial signals, and preparing the inputs needed for valuation models.

- 3-Statement Financial Modeling Course with AI: A modelling course focused on turning business analysis into income statement, balance sheet, cash flow, EPS, EBITDA, and FCF forecasts.

- Mergers and Acquisitions Online Course: A broader M&A workflow course for deal screening, due diligence, valuation, negotiation, and integration logic.

Sources

- CFA Institute, Free Cash Flow Valuation

- Aswath Damodaran, Estimating Terminal Value

- IBM, What is AI financial modeling?