Demystifying the Roles of M&A Advisors on the Sell-side and Buy-side

Navigating M&A Advisor Roles: Unveiling the Key Players in Financial Transactions

In this exploration, we will delve into the world of M&A advisor roles, shedding light on their significance and the responsibilities they shoulder.

What is an M&A Advisor?

M&A advisors or IB advisors (Investment Banking firms) are the linchpin of financial transactions, facilitating critical deals in the intricate landscape of mergers and acquisitions. Their expertise spans from raising capital to structuring deals and conducting meticulous due diligence. M&A advisors act in the best interests of their clients, which range from multinational corporations to governments.

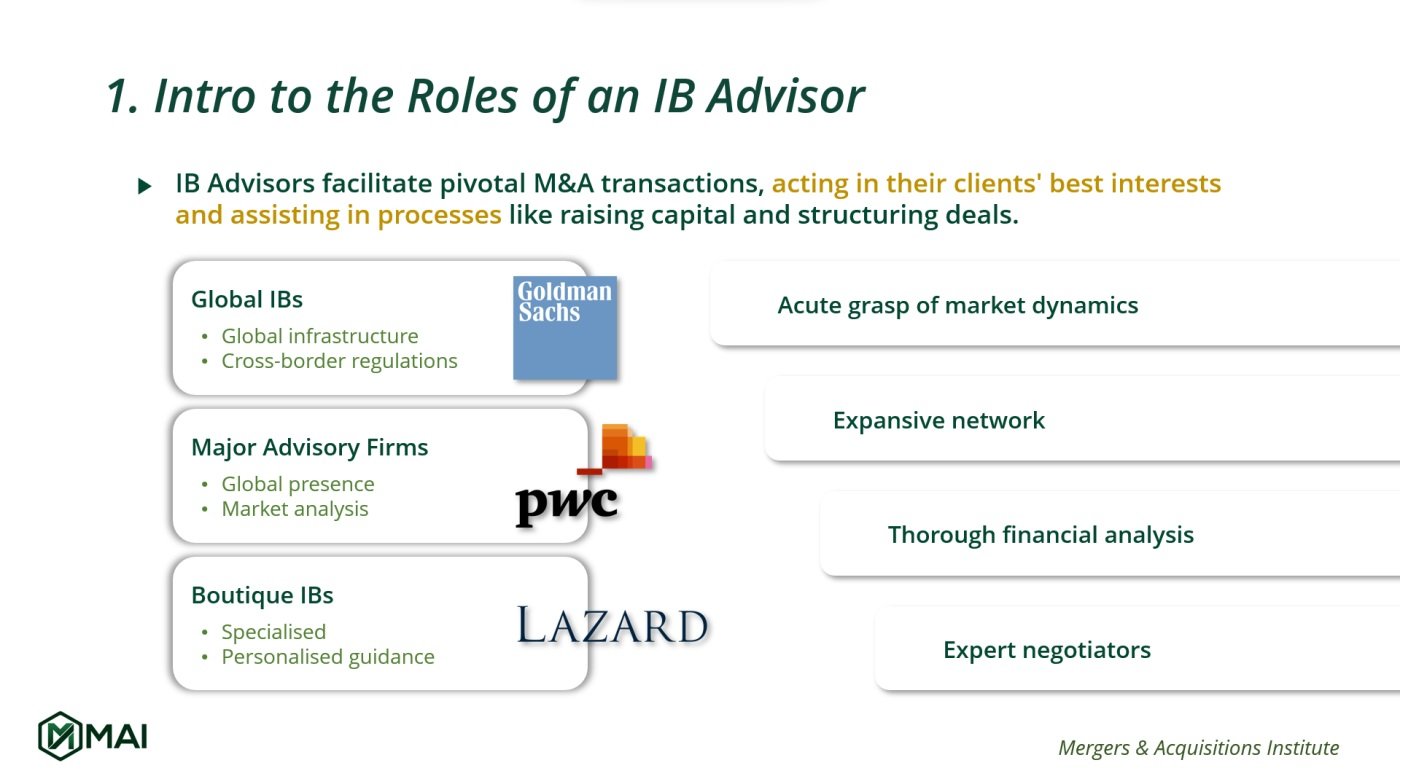

Categories of Advisory Firms

M&A advisory firms can be broadly categorized into three tiers based on their operational scale and specialization:

Top-tier Global Investment Banks:

Notable giants like Goldman Sachs, J.P. Morgan, and Barclays are renowned for their global infrastructure and industry influence. They excel in M&A advisory, leveraging their extensive networks for swift target identification and navigating complex cross-border regulations.

Major Consultancy and Advisory Firms:

Firms like PwC, Deloitte, EY, and KPMG have made a mark in M&A advisory. Their global presence ensures seamless cross-border consultations, offering diverse services, from due diligence to market analysis.

Boutique Investment Banks:

Smaller in scale but equally impactful, banks like Lazard, Evercore, and Rothschild & Co specialize in M&A. They provide tailored solutions and deep expertise in specific sectors or deal types.

The Importance of M&A Advisors in Transactions

Some M&A advisor roles and qualities include the following:

- Market Expertise: Possess an acute understanding of market dynamics, identifying trends and fluctuations that might elude others.

- Expansive Networks: M&A advisors have extensive networks that help them find potential buyers or targets quickly.

- Financial Analysis: Offer comprehensive financial analysis, crucial for setting valuations, structuring deals, and ensuring favourable outcomes.

- Expert Negotiators: These advisors are expert negotiators, ensuring that the agreed-upon terms align with their clients’ best interests.

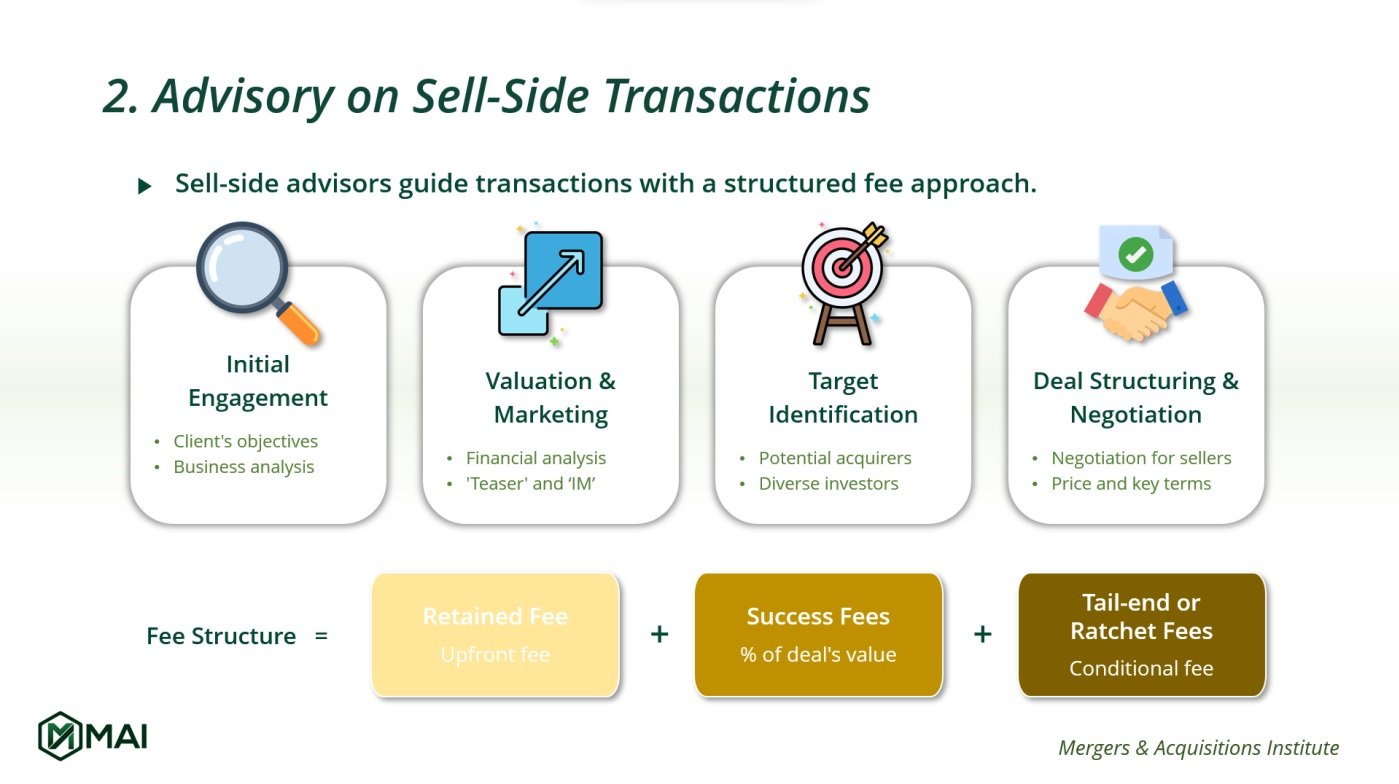

Sell-Side Advisory: An In-Depth Look

Sell-side M&A advisors represent sellers in transactions, managing everything from target identification to intricate deal negotiations.

Key M&A Advisor Roles and Responsibilities

- Initial Engagement and Preparation: Advisors start by understanding the client’s objectives, whether it’s divesting a segment or selling the entire company.

- Valuation and Marketing: They value the selling entity using financial models and market benchmarks, attracting potential buyers through teasers and Information Memorandums.

- Target Identification: Advisors identify potential acquirers, including strategic buyers, competitors, or financial entities.

- Deal Structuring and Negotiation: They manage negotiations, ensuring a favourable and secure deal structure for their clients.

Fee Structure for Sell-Side Advisory

Retained Fee: An upfront fee secures the advisor’s commitment, typically ranging from £100,000 to £500,000.

Success Fees: A percentage of the deal’s total value, paid upon successful completion. The exact fee structure can be complex and depends on the deal’s size and complexity.

Case Study: Dell’s Acquisition of EMC Corporation (2015)

In one of the most significant tech mergers, Dell acquired EMC Corporation for a staggering $67 billion. JP Morgan served as the primary sell-side M&A advisor for EMC in this transaction.

Sell Side Advisors’ Roles

- Upon engagement, JP Morgan conducted a rigorous evaluation of EMC’s assets, including the noteworthy VMware, ensuring they were clearly and effectively positioned for potential acquirers. This involved not only assessing the individual value of each asset but also how they fit into the broader tech marketplace.

- When identifying potential buyers, JP Morgan considered various entities. However, Dell, with its complementary services and intent to expand its enterprise offerings, became the preferred choice.

- The negotiation phase was intricate. The enormity of the deal meant that both sides had to engage in multiple discussions, addressing valuation, structural components, and the role of EMC’s existing leadership post-merger. JP Morgan’s adeptness in presenting EMC’s strategic value and navigating complex deal dynamics was vital in bringing the deal to fruition.

Advisory Fees

- For a transaction as significant, the retainer fee, while not typically disclosed, would often be substantial, reflecting both the deal’s complexity and the advising firm’s reputation.

- In terms of success fees, while exact numbers for JP Morgan’s earnings from the EMC deal aren’t publicly disclosed, it’s typical for investment banks to earn success fees ranging from 0.5% to 1.5% of the deal’s value, especially for mega-deals. This percentage often operates on a sliding scale, where the fee percentage decreases as the deal size surpasses certain thresholds.

- For context, let’s use industry norms to create an illustrative scenario:

- On the first $10 billion: 0.8% = $80 million

- On the next $20 billion (given the decreasing rate for larger deal sizes): 0.6% = $120 million

- On the remaining $37 billion: 0.3% = $111 million

- This would total an estimated advisory fee of $311 million.

However, this estimation is based on industry norms and practices for mega-deals. The exact fee might vary based on the specifics of the EMC and JP Morgan agreement.

Advisory on Buy-Side Transactions

In the world of M&A, buy-side advisors play an important part by representing the buyer. They take on a series of responsibilities, guiding the process from target identification to post-acquisition integration.

Key M&A Advisor Roles and Responsibilities

- Strategy Formulation and Target Identification: Buy-side M&A advisors work closely with the buyer to define a meticulous strategy that aligns with the buyer’s long-term goals and competitive position. They utilize advanced tools and industry insights to pinpoint potential acquisition targets, evaluating their strategic fit, financial health, and potential synergies with the buyer.

- Initial Evaluation and Outreach: After shortlisting potential targets, buy-side advisors conduct a comprehensive financial and operational evaluation. Armed with this knowledge, they initiate the first round of talks, emphasizing the mutual advantages of a prospective partnership.

- Due Diligence: The entire business spectrum of the target, from financial health to legal compliance, undergoes meticulous scrutiny. The aim is to provide the buyer with a transparent view of potential risks and opportunities associated with the acquisition.

- Deal Structuring and Negotiation: Following thorough due diligence, buy-side advisors delve into the specifics of the deal, including pricing and terms. Additionally, they lay the groundwork for post-acquisition integration, planning for a seamless confluence of operations and cultures.

- Post-Merger Integration (PMI): This phase focuses on melding operations and cultures to realize the envisaged value from the acquisition. Activities may encompass talent retention, tech integration, and possible divestitures. In some cases, the PMI process might be outsourced to specialists to ensure optimal results.

Fee Structure for Buy-Side Advisory

The compensation structure for buy-side advisory differs from that of sell-side advisory, reflecting the unique challenges and complexities of scouting, vetting, and executing acquisitions. Here’s a breakdown:

- Retained Fee: In buy-side engagements, the retained fee serves as a testament to the buyer’s earnestness. Given the emphasis on proactive target identification, this fee may exceed those in sell-side transactions. For major deals, considering the firm’s stature, retainers could range from $200,000 to $1 million.

- Transaction Fee: Buy-side advisors might charge higher rates due to the intricacies involved in scouting and executing acquisitions. To illustrate, let’s consider a hypothetical $60 billion deal:

- On the first $10 billion: 1.0% = $100 million

- On the next $20 billion: 0.8% = $160 million

- On the remaining $30 billion: 0.5% = $150 million

- Thus, an estimated total fee for this example stands at around $410 million. However, actual rates can vary significantly based on deal-specific nuances.

- Performance-based Bonuses: These bonuses are notably more prevalent on the buy-side and serve to reward post-acquisition success. For instance, if a purchased entity outperforms revenue targets by $200 million in the first year, a 5% bonus on this excess could yield an additional $10 million.

Case Study: Facebook’s Acquisition of WhatsApp (2014)

M&A advisors often shine in high-stakes acquisitions, and the case of Facebook’s acquisition of WhatsApp for a staggering $19 billion exemplifies the critical role of buy-side advisors.

Buy Side Advisors’ Roles

In 2014, Morgan Stanley played a significant role as Facebook’s buy-side advisor in this landmark acquisition. WhatsApp, with its massive user base, had yet to adopt a monetization strategy. Morgan Stanley’s contributions were instrumental:

- Crafting a Future-focused Valuation Model: The advisor incorporated prospective monetization avenues and synergistic benefits with Facebook’s ecosystem, emphasizing the strategic importance of WhatsApp.

- Navigating Intense Competition: Morgan Stanley faced fierce competition from other tech giants vying for WhatsApp. They ensured that Facebook’s bid was not only financially competitive but also presented a compelling vision for WhatsApp’s future within the Facebook ecosystem.

- Augmenting Facebook’s Stature: The successful acquisition significantly bolstered Facebook’s position in the tech space. While WhatsApp’s direct monetization remains a work in progress, its strategic importance in data and user engagement has grown exponentially.

Advisory Fees

While specific fees for this high-profile deal aren’t disclosed, industry norms provide some insights:

- Retainer Fee: Morgan Stanley’s expertise likely commanded a substantial retainer fee, possibly around $5 million.

- Transaction Fee: Given the $19 billion deal size, the transaction fee was likely substantial, estimated to be near $28 million.

- Success Fee: A success bonus, possibly around $7 million, could be considered based on the deal’s successful completion.

Summing these components, it suggests a total fee of around $40 million for Morgan Stanley’s invaluable contributions, although actual figures may vary based on the agreement between Facebook and Morgan Stanley.

Understanding the multifaceted M&A advisor roles on both the sell-side and buy-side is crucial in comprehending the intricate world of investment banking and its significance in driving successful acquisitions.