Revenue Recognition ASC 606 & IFRS 15: 5-Step Quality Test with AI

A revenue model can look precise while the revenue behind it is weak.

The company may report growth, but the footnotes may show aggressive timing, heavy judgment, weak cash conversion, or revenue that does not repeat.

That is why revenue recognition ASC 606 is not only a technical accounting topic.

For analysts, revenue recognition ASC 606 is the starting point for testing whether reported revenue deserves to be forecast, valued, and trusted.

This article explains revenue recognition ASC 606 and IFRS 15 revenue recognition through a practical quality lens.

It uses Microsoft as the main example because its fiscal year 2025 disclosures show product revenue, service revenue, cloud subscriptions, Office 365 ratable recognition, payment terms, net income, and operating cash flow in one reporting package.

The goal is not to memorize accounting terminology.

The goal is to read the revenue note, connect it to the income statement, test it against the balance sheet and cash flow statement, and then use AI to speed up the review without handing judgment to AI.

Revenue Recognition ASC 606 and IFRS 15 Start with Economic Substance

A revenue number looks simple on the income statement, but it is the result of contract analysis, accounting judgment, billing timing, and customer behavior.

That is why analysts do not begin a revenue review by asking whether sales increased.

They begin by asking whether the reported sales faithfully reflect what the company has actually delivered to customers.

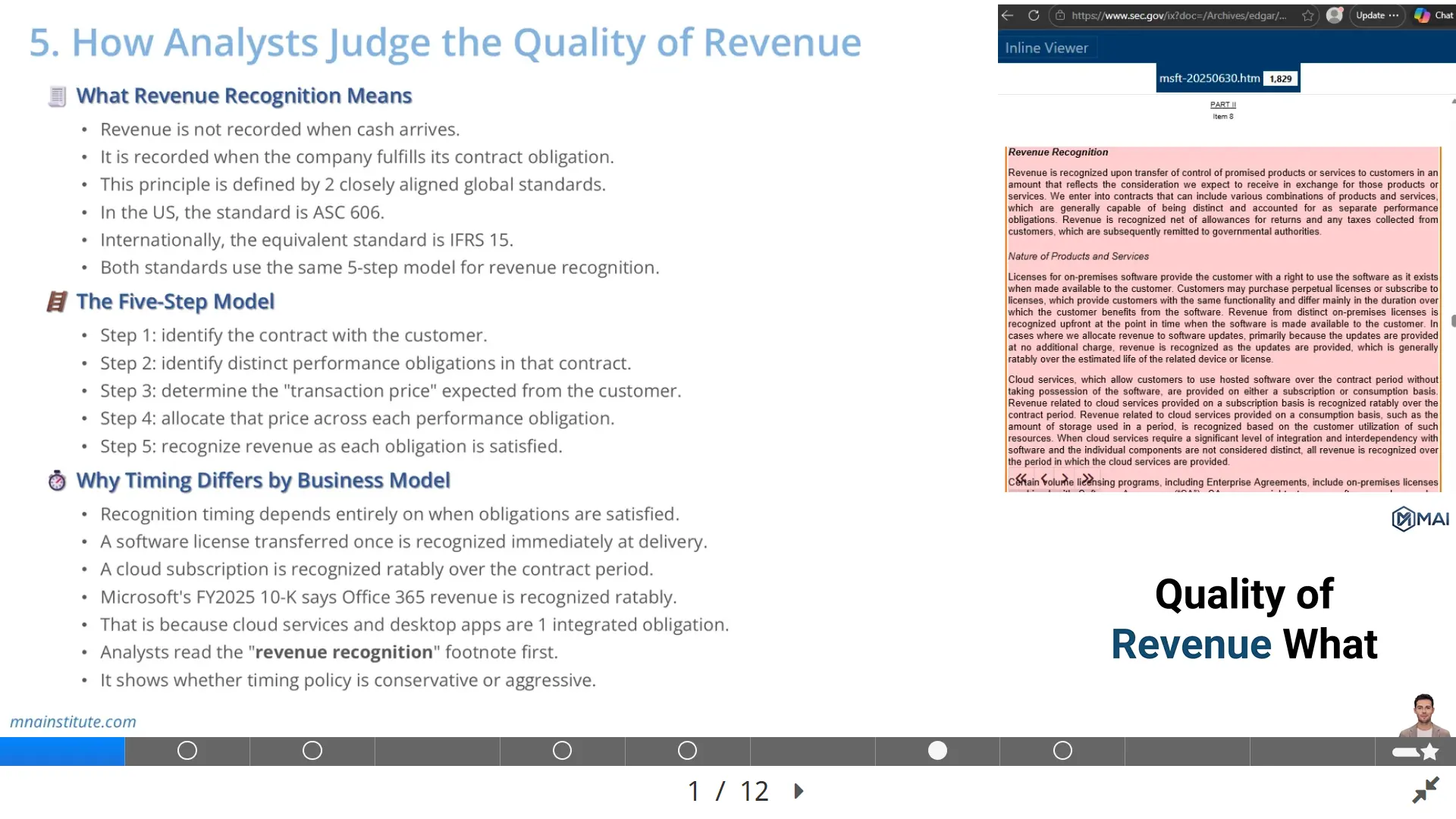

Revenue recognition ASC 606 in the United States and IFRS 15 revenue recognition internationally both start from the same core idea.

Revenue is recognized when control of promised goods or services transfers to the customer, in an amount that reflects the consideration the company expects to receive.

That principle sounds clean, but the practical work can be complex when contracts include software licenses, cloud services, implementation work, support, discounts, renewal options, usage-based fees, and multi-year billing terms.

For a simple product sale, the question may be whether the customer has obtained control of the product.

For a cloud subscription, the question is whether the service is delivered continuously over the contract period.

For a bundled enterprise software contract, the analyst must understand whether each promise is distinct or whether several promises function together as one obligation.

This is where revenue quality begins.

High reported revenue does not automatically mean high-quality revenue, and revenue recognition ASC 606 does not remove the need for analyst judgment.

The analyst must decide whether recognition timing, contract structure, cash collection, and disclosure detail support the reported number.

A professional review therefore treats revenue recognition ASC 606 as both an accounting framework and an analytical test.

The standard tells the company when revenue can be recorded.

The analyst uses the same framework to judge whether that revenue is sustainable, collectible, recurring, and supported by cash.

The Five-Step Quality Test Behind Reported Revenue

The five steps can be translated into the following analyst questions.

1. Contract: Is there an enforceable customer arrangement that supports the revenue?

2. Performance obligations: What exactly did the company promise to deliver?

3. Transaction price: How much consideration does the company expect to receive?

4. Allocation: How is that price split across distinct obligations?

5. Recognition: Has the company satisfied the obligation at a point in time or over time?

Revenue recognition ASC 606 and IFRS 15 use a five-step model.

The revenue recognition ASC 606 model is not just a compliance checklist.

For analysts, it is a practical way to locate where judgment enters the revenue number.

Step 1 is to identify the contract with the customer.

This sounds basic, but contract existence matters because revenue cannot be analyzed properly unless enforceable rights and obligations are clear.

A signed enterprise agreement, a purchase order, and a usage-based cloud arrangement can create different revenue patterns.

Step 2 is to identify the distinct performance obligations in that contract.

This is often the most analytical part of the review because one contract may include several promises.

A software vendor may sell a license, cloud access, installation support, technical support, and future updates in one commercial package.

If each promise is distinct, revenue may be allocated and recognized separately.

If the promises are highly integrated, revenue may be recognized over time as one combined service.

Step 3 is to determine the transaction price.

This requires attention to discounts, rebates, usage-based fees, refunds, credits, and variable consideration.

The number on the invoice is not always the number that can be recognized as revenue immediately.

Step 4 is to allocate the transaction price to the performance obligations based on relative standalone selling price.

This is where the analyst looks for judgment in pricing allocation.

If standalone selling prices are not directly observable, management must estimate them.

Step 5 is to recognize revenue when each performance obligation is satisfied.

That can happen at a point in time or over time.

The quality test is to ask where management has discretion at each step and whether the disclosures explain that discretion clearly.

A clean revenue policy is not one with no judgment.

A clean policy is one where the judgment is visible, consistent, and tied to contract economics.

Why Revenue Timing Changes by Business Model

The timing under revenue recognition ASC 606 depends on how the customer receives value.

That is why the same company can have several revenue recognition patterns across its business lines.

A perpetual software license may transfer control at the moment the license is made available to the customer.

In that case, revenue may be recognized upfront if the license is distinct and the customer can benefit from it when delivered.

A cloud subscription is different because the customer receives value continuously as the service is provided.

Revenue is therefore recognized ratably over the contract period when the subscription service is delivered evenly over time.

A consulting engagement may be recognized as services are performed.

A usage-based cloud service may be recognized based on customer consumption during the period.

Microsoft provides a useful real-world example because its business includes product revenue, cloud services, Office 365 subscriptions, gaming, LinkedIn, advertising, support, and consulting.

Microsoft states in its fiscal year 2025 annual report that revenue is recognized when control of promised products or services transfers to customers.

It also explains that cloud services provided on a subscription basis are recognized ratably over the contract period.

For Office 365, Microsoft discloses that certain desktop applications and cloud services are accounted for together as one performance obligation, with revenue recognized ratably over the period in which cloud services are provided.

This disclosure matters because it explains why cash collection, billing, and revenue recognition may not occur on the same date.

A customer may pay at the beginning of an annual subscription period.

The company records cash and unearned revenue first.

Then it recognizes revenue over the service period as it satisfies the obligation.

A customer may also receive a product before paying cash.

In that case, revenue may be recognized before cash is collected, creating accounts receivable.

This is why timing is the first revenue quality question.

The issue is not whether early or deferred recognition is automatically wrong.

The issue is whether recognition follows the actual transfer of value to the customer.

Product, Service, and Recurring Revenue Cannot Be Read as One Line

The revenue line on the income statement often combines different revenue streams with different risk profiles, which is why revenue recognition ASC 606 must be read with business model context.

A useful revenue review separates product revenue, service revenue, recurring revenue, and non-recurring revenue before forecasting future performance.

Product revenue often includes one-time sales such as perpetual software licenses, devices, gaming hardware, or other delivered goods.

Service revenue often includes cloud subscriptions, hosted software, support, advertising, consulting, and platform services.

Recurring revenue is attractive to analysts because it repeats across periods when customers renew subscriptions, continue using cloud services, or remain under multi-year contracts.

Non-recurring revenue is less predictable because it depends on one-time transactions that may not repeat.

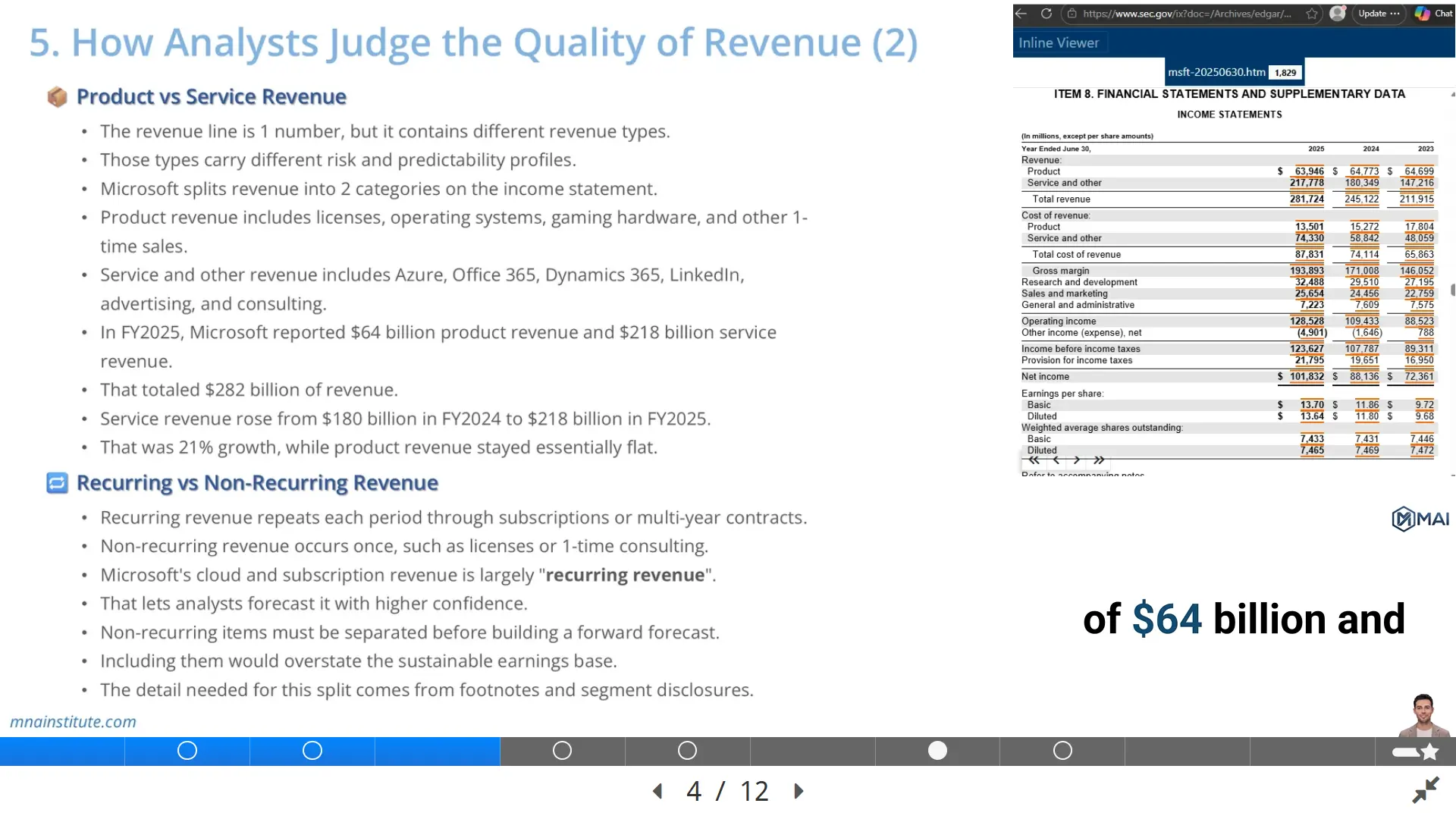

Microsoft reported $281.724 billion of total revenue in fiscal year 2025.

Its product revenue was $63.946 billion, while service and other revenue was $217.778 billion.

Service and other revenue also increased from $180.349 billion in fiscal year 2024 to $217.778 billion in fiscal year 2025.

That mix tells the analyst something that the total revenue number alone cannot show.

A company with a larger subscription and cloud services base may have more visibility into future revenue than a company dependent on one-time license sales.

That does not mean all service revenue is automatically high quality.

The analyst still needs to examine churn, contract duration, renewal pricing, customer concentration, billing terms, and usage behavior.

The phrase recurring revenue should therefore be tested, not accepted as a label.

A reported category may include both genuinely recurring subscription revenue and less predictable consulting or advertising revenue.

That is why the revenue footnote, segment disclosure, and management discussion must be read together.

A beginner may look at the top-line growth rate and stop.

An analyst asks what kind of revenue grew, whether it will repeat, and whether the cash conversion pattern supports it.

Accrual Earnings vs Cash Earnings: Where Quality of Earnings Starts

Revenue recognition ASC 606 is based on accrual accounting, not cash accounting.

Revenue is recognized when earned under the contract, not simply when cash arrives in the bank.

This creates a natural gap between reported earnings and actual cash generation, even when revenue recognition ASC 606 has been applied correctly.

That gap is not automatically a problem.

It becomes a quality of earnings question when the gap persists, widens, or cannot be explained by the business model.

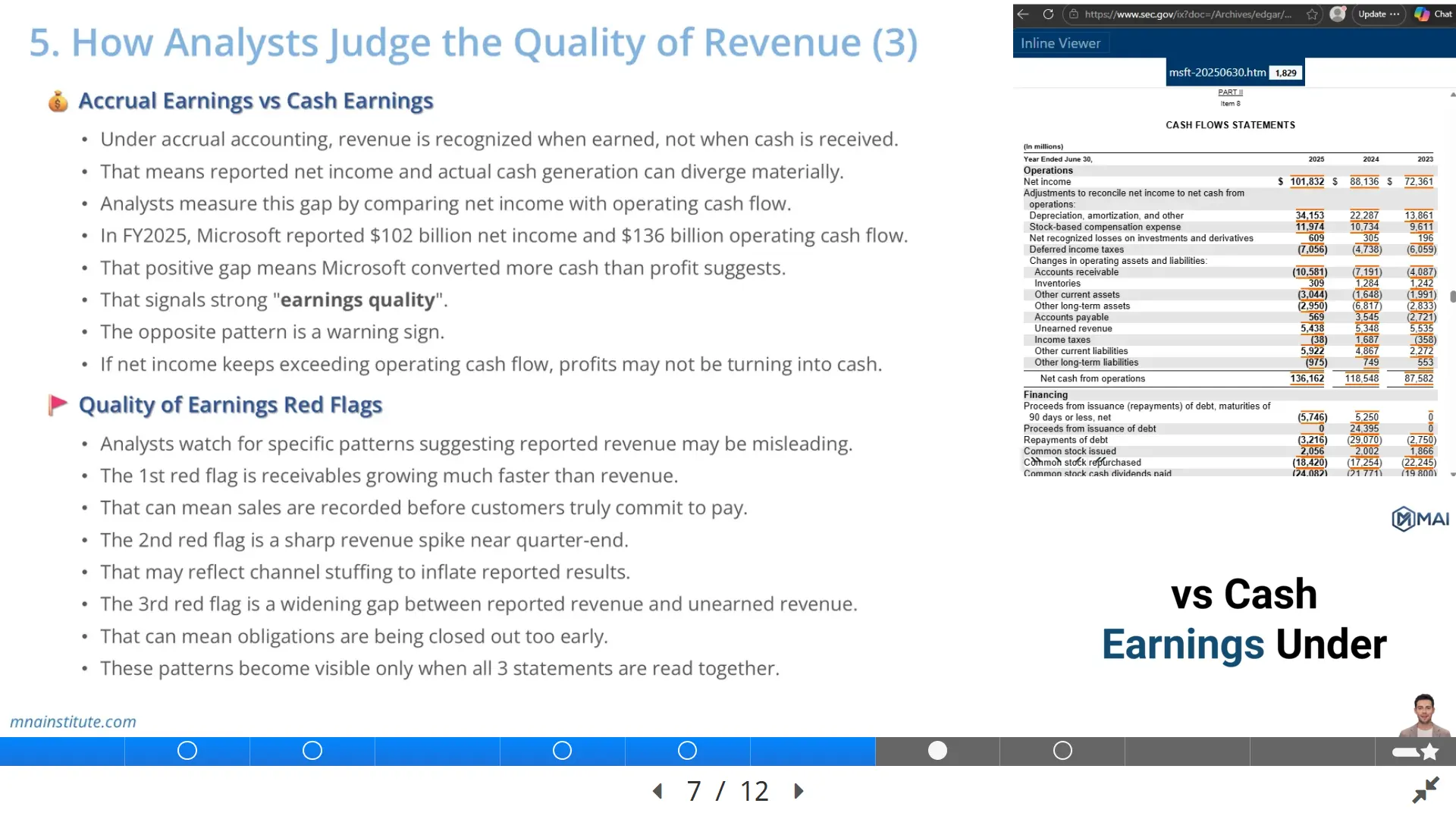

A strong first test is to compare net income with operating cash flow.

Microsoft reported fiscal year 2025 net income of $101.832 billion.

Its operating cash flow was $136.163 billion for the same period.

That positive relationship means Microsoft generated more operating cash than reported profit in that year.

A major reason is that non-cash charges are added back in the operating cash flow reconciliation.

Microsoft reported $34.153 billion of depreciation, amortization, and other adjustments, plus $11.974 billion of stock-based compensation expense in fiscal year 2025.

These items reduced accounting profit but did not require cash to leave the business in the same way during the period.

The reverse pattern deserves attention.

If net income consistently exceeds operating cash flow, the analyst should ask why earnings are not converting into cash.

One possible reason is rising accounts receivable.

Another is aggressive revenue timing.

Another is a working capital build caused by genuine growth.

The point is not to assume manipulation.

The point is to connect the income statement to the cash flow statement before accepting reported growth.

Quality of earnings analysis asks whether profit is supported by recurring operations and real cash conversion.

For revenue quality, this comparison is one of the fastest ways to move from accounting presentation to economic substance.

Revenue Recognition Red Flags Across the Three Statements

A simple red flag matrix is useful before reviewing the detailed footnotes.

|

Pattern |

Where It Appears |

Analyst Question |

|

Receivables grow faster than revenue |

Balance sheet and cash flow statement |

Are customers paying on normal terms? |

|

Revenue jumps near period end |

Quarterly revenue and management commentary |

Was revenue pulled forward? |

|

Deferred revenue moves inconsistently |

Contract liability footnote |

Does subscription billing support reported growth? |

|

Heavy judgment in allocation |

Revenue recognition footnote |

Is the standalone selling price estimate clear? |

The table does not prove anything by itself, but it tells the analyst where to look next.

Revenue recognition ASC 606 red flags are rarely visible in one statement alone.

They usually appear when the income statement, balance sheet, cash flow statement, and footnotes are read together.

The first red flag is accounts receivable growing much faster than revenue.

This pattern can mean that sales are being booked before cash collection keeps pace.

It can also reflect a legitimate shift toward enterprise contracts with longer billing terms.

The analyst must investigate the cause rather than treat the ratio as an automatic verdict.

The second red flag is a sharp end-of-period revenue spike.

This may indicate discounting, pull-forward sales, channel stuffing, or unusual customer incentives near quarter-end.

The third red flag is a mismatch between recurring revenue claims and deferred revenue movement.

If customers pay in advance for subscriptions, unearned revenue should generally provide useful evidence about future service obligations.

If reported recurring revenue rises but unearned revenue does not move in a consistent way, the analyst should ask whether the business mix has changed.

The fourth red flag is significant judgment language in the revenue recognition footnote without enough explanation.

Management judgment is normal when contracts include multiple performance obligations or estimated standalone selling prices.

The concern is not the existence of judgment.

The concern is whether the disclosure allows investors to understand how that judgment affects timing and amount.

The fifth red flag is a widening gap between revenue growth and operating cash flow growth.

A business can grow revenue while consuming cash if working capital expands rapidly.

That may be acceptable during a transition period, but it needs to be modeled explicitly.

A professional revenue recognition ASC 606 review does not rely on one red flag in isolation.

It builds a chain of evidence across disclosures, balance sheet movements, and cash conversion.

Using AI for Revenue Quality Review

AI can make revenue recognition ASC 606 quality review faster because the evidence is scattered across long filings.

A 10-K may contain the income statement in one section, revenue policy in another section, segment revenue in another section, and contract balance disclosures in the footnotes.

AI is useful when it is forced into a structured analyst workflow.

A weak prompt asks AI to summarize revenue recognition.

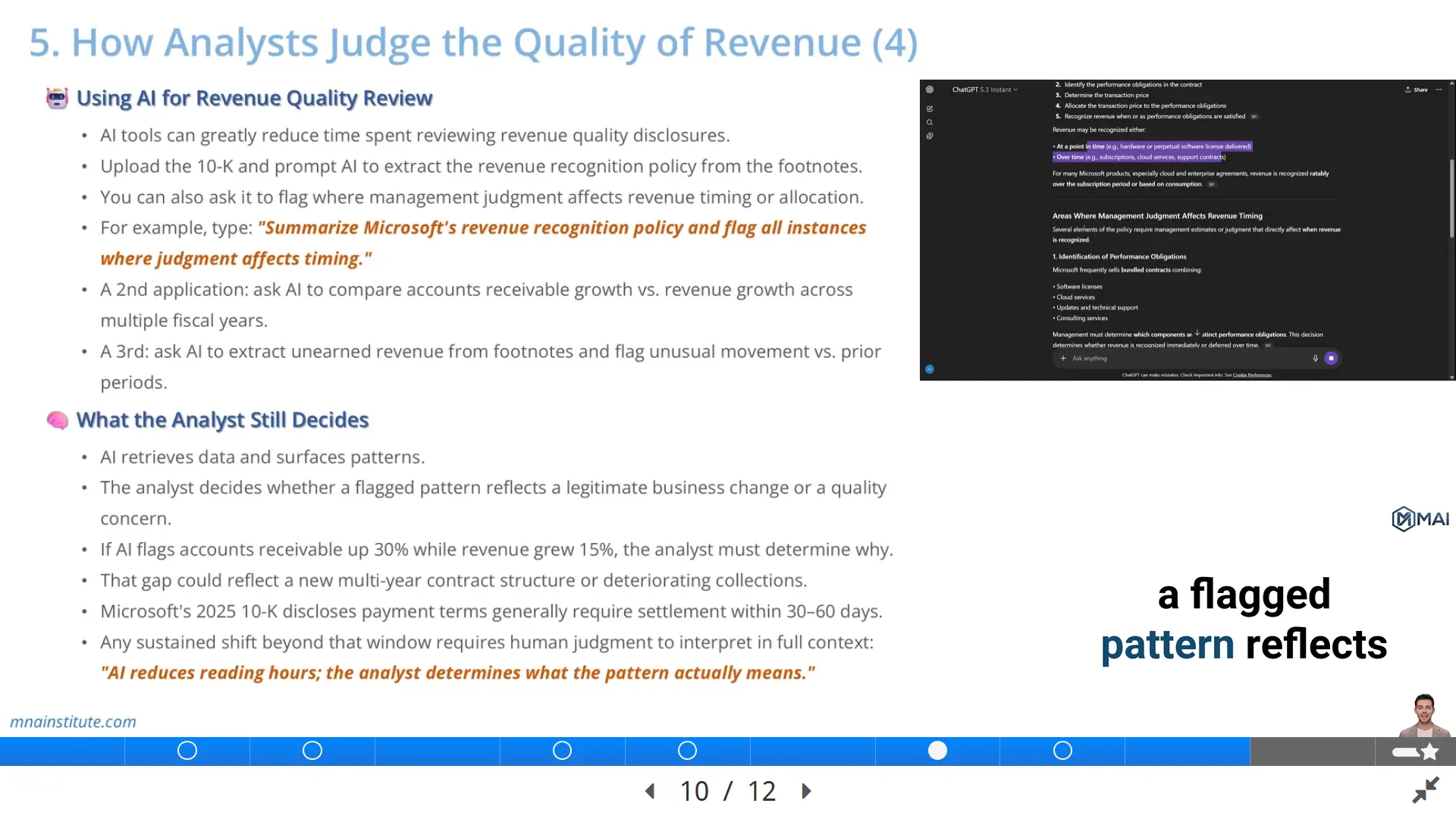

A stronger prompt asks AI to extract the exact revenue recognition policy, identify performance obligations, locate management judgment language, and compare the policy with revenue categories.

For example, an analyst could upload the annual report and ask AI to identify all passages where revenue recognition depends on determining whether products and services are distinct.

The output should not be treated as a conclusion.

It should be treated as a map of where the analyst needs to read.

AI can also compare accounts receivable growth with revenue growth across multiple years.

It can extract unearned revenue balances and compare them with subscription revenue commentary.

It can summarize changes in operating cash flow, stock-based compensation, depreciation, and working capital.

It can identify whether the company discusses payment terms and whether those terms changed.

The value is speed and consistency.

AI reduces the manual search burden, especially when multiple companies must be reviewed in equity research, M&A due diligence, or credit analysis.

The risk is false confidence.

AI may miss a nuance in contract language, misread a table, or treat a management explanation as sufficient when it still needs challenge.

That is why the workflow should keep the analyst in control.

Use AI to extract, compare, and flag.

Use human judgment to decide whether the pattern changes the forecast, valuation, or diligence conclusion.

What the Analyst Still Decides After AI Flags the Pattern

The analyst still makes the economic judgment after revenue recognition ASC 606 analysis is complete.

Suppose AI finds that accounts receivable grew 30% while revenue grew 15%.

That pattern is worth investigating, but it is not a final answer.

It could indicate aggressive recognition, slower collection, customer credit stress, or sales booked before cash commitment became strong.

It could also reflect a new enterprise customer mix, more annual billing, a large contract signed late in the year, or a shift from consumer sales to corporate contracts.

The next step is to read the payment terms, contract balance disclosure, management discussion, and cash flow reconciliation.

Microsoft discloses that payment terms generally require settlement within 30 to 60 days, although terms vary by contract type.

If a future analyst observed a sustained receivables shift outside that expected window, the question would not be whether Microsoft broke a rule.

The question would be whether customer payment behavior, contract structure, or revenue mix had changed enough to affect forecast confidence.

That is the difference between mechanical screening and professional analysis.

A screen flags the variance.

An analyst explains the cause.

A valuation model then reflects the answer through revenue growth, working capital assumptions, margin confidence, or discount rate judgment.

Revenue recognition ASC 606 gives the accounting architecture.

IFRS 15 revenue recognition provides a comparable global architecture.

Quality of earnings analysis tests whether reported results are supported by recurring operations and cash conversion.

AI helps locate the questions faster.

The analyst decides what those questions mean for the business.

That is the revenue quality review discipline this article is designed to teach.

Related Courses

Revenue recognition ASC 606 quality work sits at the intersection of accounting, valuation, and diligence.

It requires analysts to understand the accounting standard, read the footnotes, connect revenue with receivables and unearned revenue, and test whether profit converts into cash.

- That is why this topic naturally connects with the Financial Modeling and Valuation Course with AI and Excel.

- The same workflow also supports the Financial Statement Analysis Course with AI for Equity Research when analysts need to read 10-K disclosures and assess earnings quality.

- For learners building integrated models, the 3-Statement Financial Modeling Course with AI helps connect revenue, working capital, cash flow, and balance sheet movement inside one model.

- For transaction work, revenue quality review is also a core diligence habit in the M&A Due Diligence Course because reported revenue affects normalized EBITDA, purchase price, and deal risk.

The broader lesson is simple: revenue is not just a top-line figure.

It is a contract-based, cash-tested, judgment-sensitive input that drives forecast credibility.

Sources

- FASB ASU 2014-09, Revenue from Contracts with Customers

- PwC IFRS 15 Revenue from Contracts with Customers overview

- Microsoft 2025 Annual Report

- CFA Institute, Evaluating Quality of Financial Reports