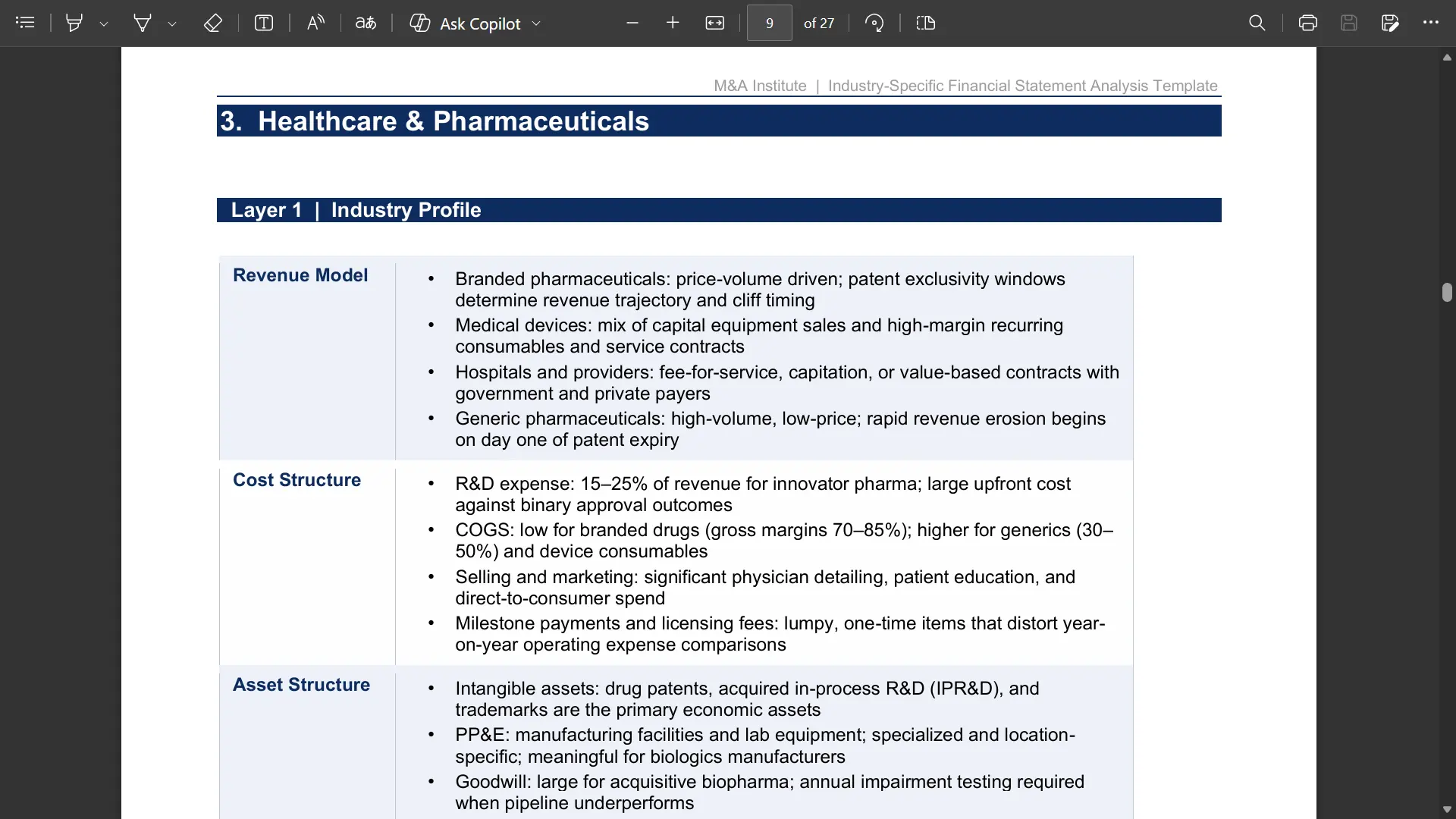

How to Value a Company: 7 Investment Valuation Courses

Most people search how to value a company when they need a formula.

The better question is how to value a company in a way that survives scrutiny from an investment committee, a corporate development team, a portfolio manager, or a client.

A valuation that cannot explain its financial statement inputs, forecast assumptions, discount rate, peer multiples, sensitivity range, and final conclusion is not a valuation yet.

It is only a spreadsheet output.

Professional investment valuation training should therefore teach the full workflow, not only DCF formulas.

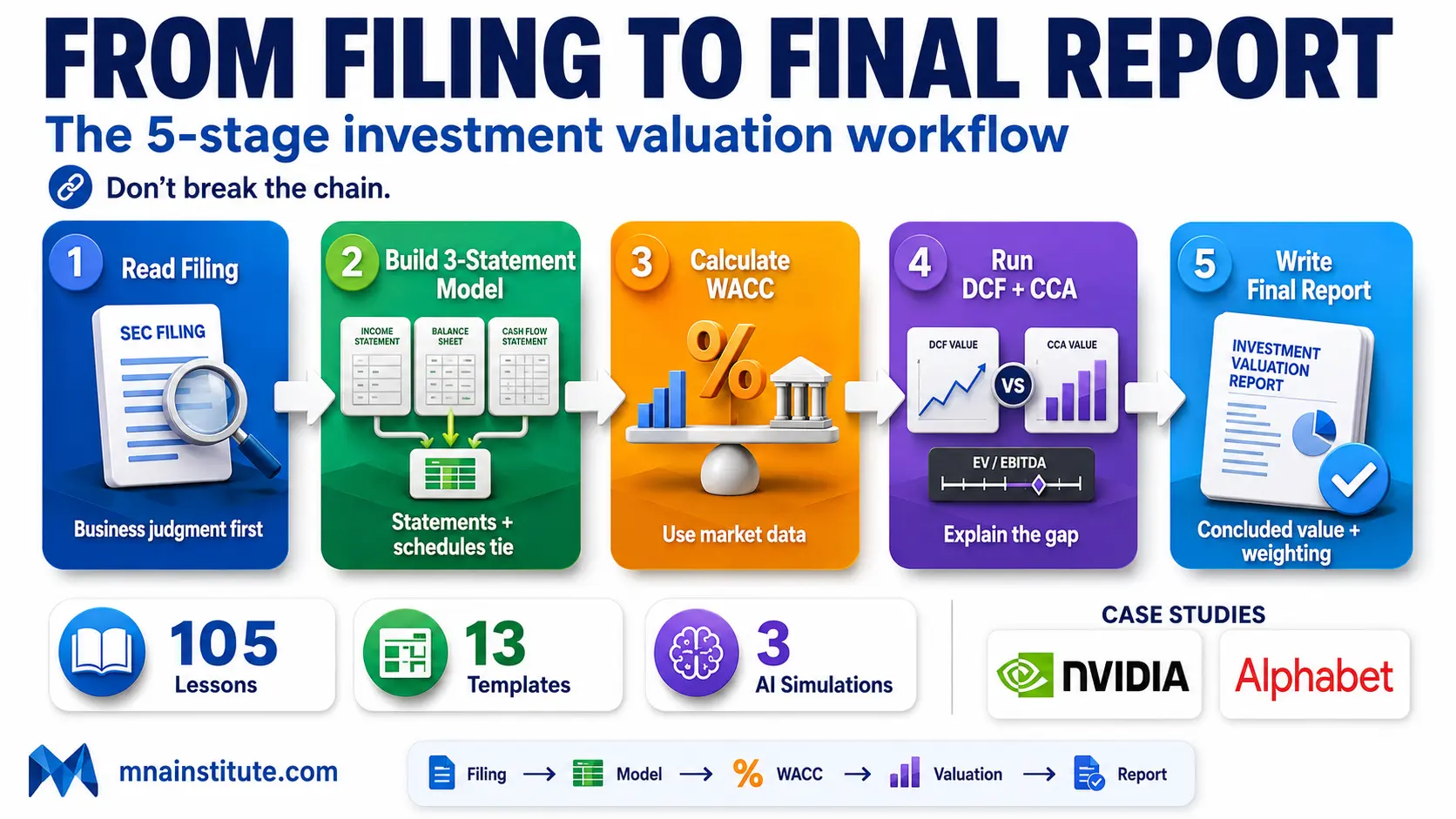

The workflow begins with filings and financial statements, moves into forecasting, calculates WACC, applies a DCF valuation model, cross-checks with comparable company analysis, and ends with valuation report writing.

This is why an investment valuation course must connect reading, modeling, valuation, and communication into one disciplined process.

The goal is not to memorize valuation vocabulary.

The goal is to build a defensible value conclusion from evidence.

That is the practical meaning of how to value a company.

It also explains why how to value a company cannot be reduced to one spreadsheet tab.

Why Most Valuation Training Feels Incomplete

Many learners are shown a DCF valuation model before they know what the forecast cash flows actually mean.

They may learn WACC before they understand why enterprise value differs from equity value.

They may learn comparable company analysis before they can judge whether the peer group is economically comparable.

They may learn valuation report writing after the model is already finished, which turns the report into decoration rather than analysis.

That sequence creates a familiar problem.

The learner can follow the spreadsheet, but cannot defend the conclusion.

A serious answer to how to value a company must start before the model opens.

It starts with the business.

- What does the company sell?

- Who buys it?

- What controls pricing?

- What drives volume?

- How much capital must be reinvested to sustain growth?

- What risks deserve a discount rate adjustment, a forecast haircut, or a scenario case?

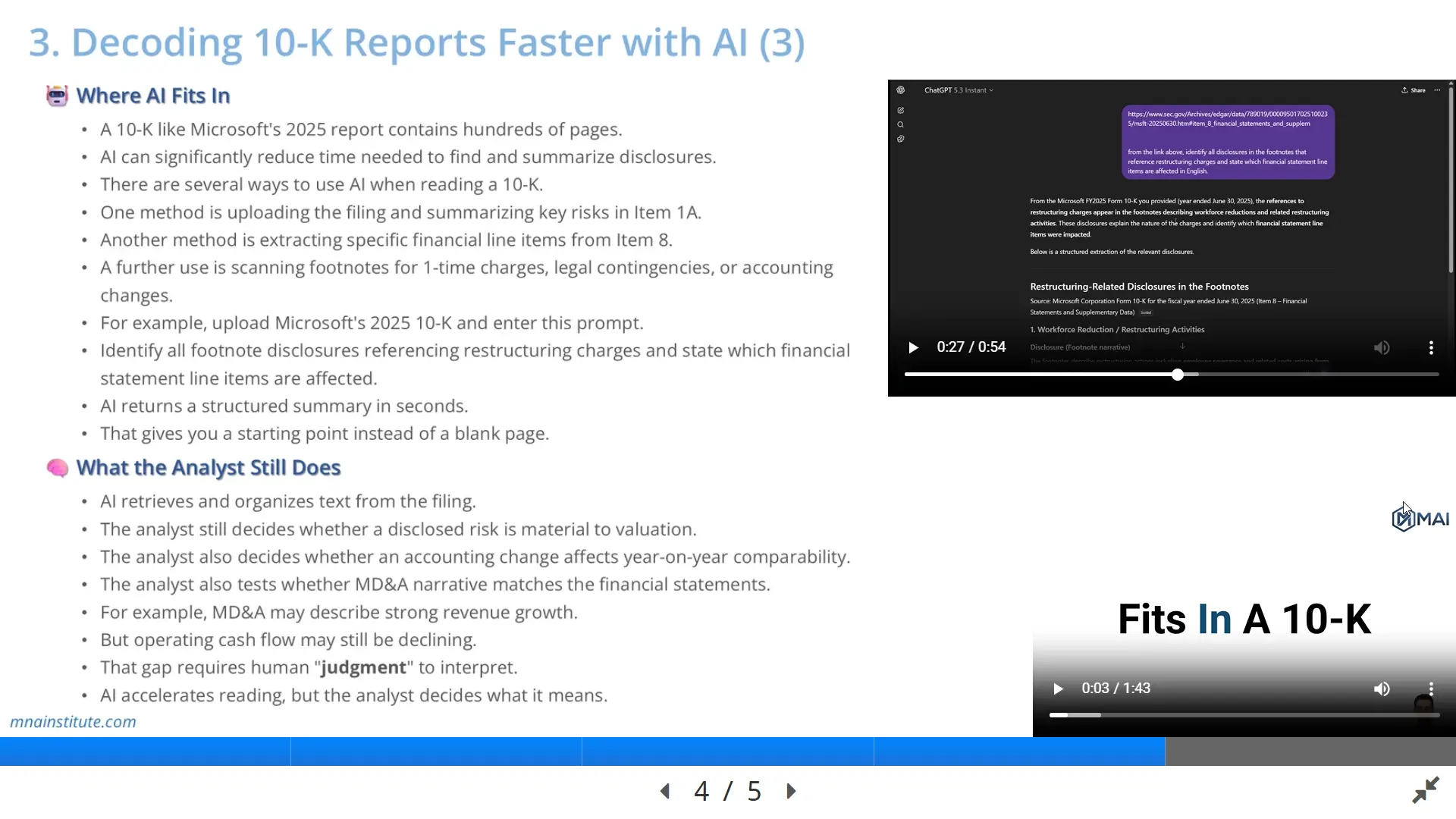

The SEC explains that a Form 10-K gives investors a comprehensive view of a company, including business description, risk factors, management discussion, and audited financial statements.

That means the 10-K is not just regulatory text.

It is the raw material for valuation judgment.

A Cold Comparison: Formula Training vs Analyst Workflow

|

Dimension |

Formula-Only Approach |

Integrated Investment Valuation Training |

|

Starting point |

Starts with DCF mechanics or Excel templates. |

Starts with business model, 10-K reading, financial statement signals, and valuation purpose. |

|

Forecast logic |

Uses generic growth, margin, and terminal assumptions. |

Links products, customers, industry forces, pricing, volume, CapEx, working capital, and management guidance. |

|

Valuation methods |

Teaches DCF, multiples, and WACC as separate topics. |

Connects WACC, FCFF, DCF, CCA, sensitivity, and valuation report writing into one workflow. |

|

AI use |

Uses AI to generate summaries or formula explanations. |

Uses AI to extract, organize, verify, challenge, and explain valuation inputs under analyst control. |

|

Final output |

Ends with an implied value or target price. |

Ends with a concluded value, method weighting, sensitivity range, and investment rationale. |

The difference is practical.

If the training stops at formulas, the learner may know the mechanics but miss the judgment.

If the training follows the analyst workflow, the learner understands why each number enters the model and how each assumption changes the conclusion.

That is the difference between knowing a valuation method and knowing how to value a company.

Step 1: Define the Valuation Question Before Building the Model

The first step in how to value a company is defining the purpose of the valuation.

A valuation for equity research is not identical to a valuation for an acquisition bid.

A valuation for an internal capital allocation decision is not identical to a valuation for fundraising.

The same company can be valued with different emphasis depending on the audience and decision.

An equity research analyst wants to know whether the current share price reflects future earnings and cash flow.

An M&A buyer wants to know the maximum price that still creates value after synergies, financing costs, and integration risk.

A corporate finance team wants to know whether a project or target company clears the firm’s cost of capital.

This framing decides the model structure, the time horizon, the valuation method, and the tone of the final report.

A well-designed investment valuation course should teach this decision logic before teaching formula execution.

Step 2: Read the 10-K and Financial Statements Like a Valuation Analyst

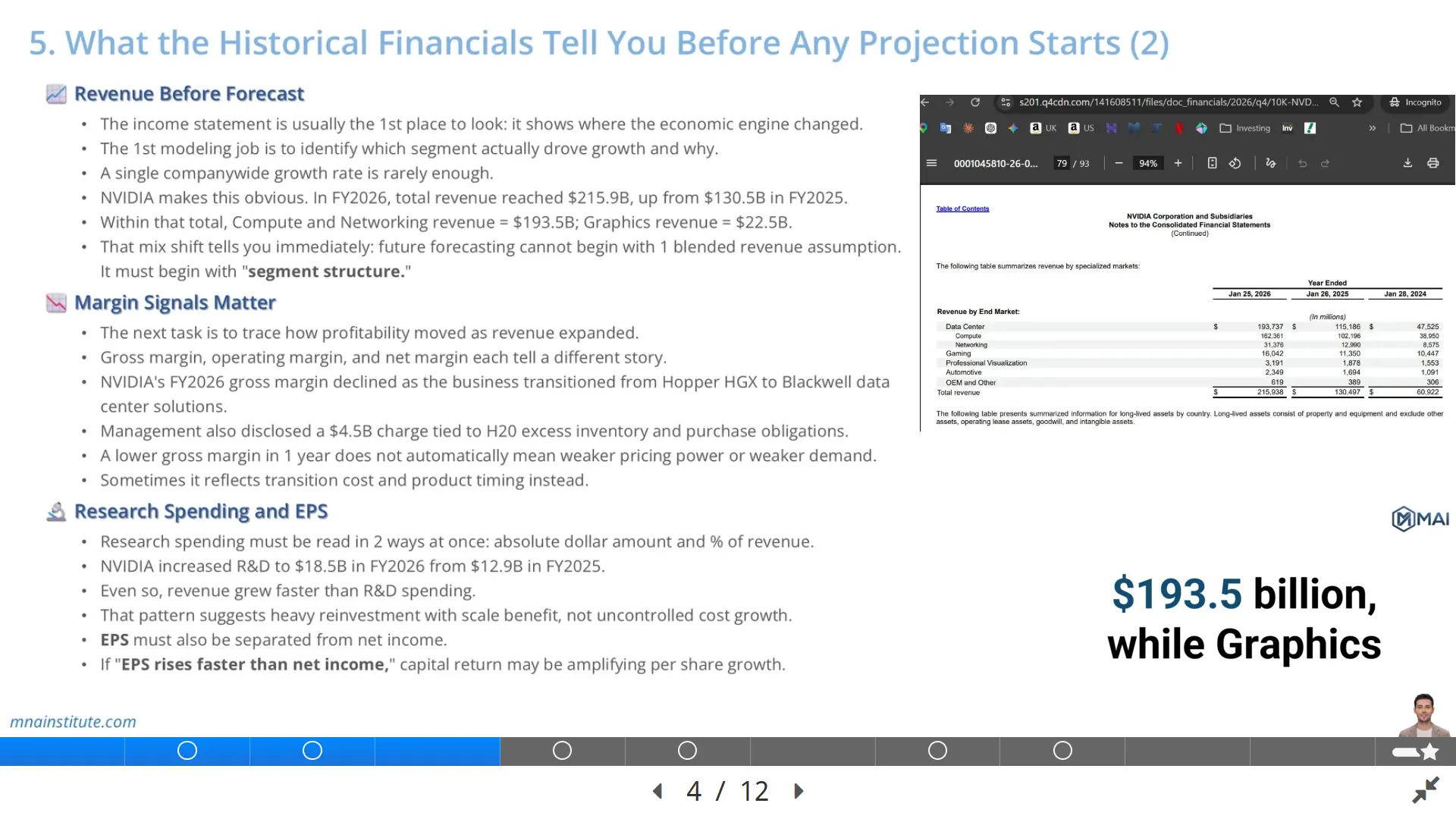

The second step in how to value a company is reading the financial statements for valuation signals.

The income statement explains revenue, margins, cost structure, operating leverage, and tax burden.

The balance sheet explains capital intensity, working capital needs, debt capacity, non-operating assets, and financial flexibility.

The cash flow statement explains whether accounting earnings convert into cash.

A valuation analyst reads these statements together.

Revenue growth that does not convert into cash may require more cautious forecasts.

High EBITDA margins may deserve a lower valuation if CapEx and working capital consume too much cash.

A clean net income trend may still hide weak free cash flow conversion.

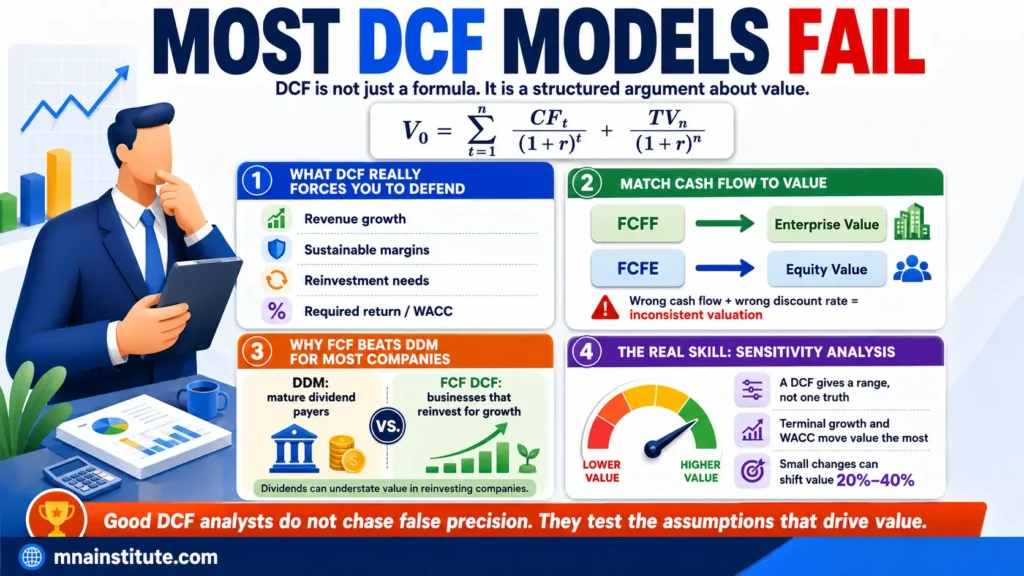

CFA Institute’s free cash flow valuation material emphasizes that FCFF and FCFE help value companies when dividends are not a reliable measure of capacity to distribute cash.

That point matters because valuation is ultimately about cash that can be claimed by capital providers.

A practical investment valuation training workflow therefore teaches ratio analysis, earnings quality, FCFF drivers, and credit signals before the DCF valuation model begins.

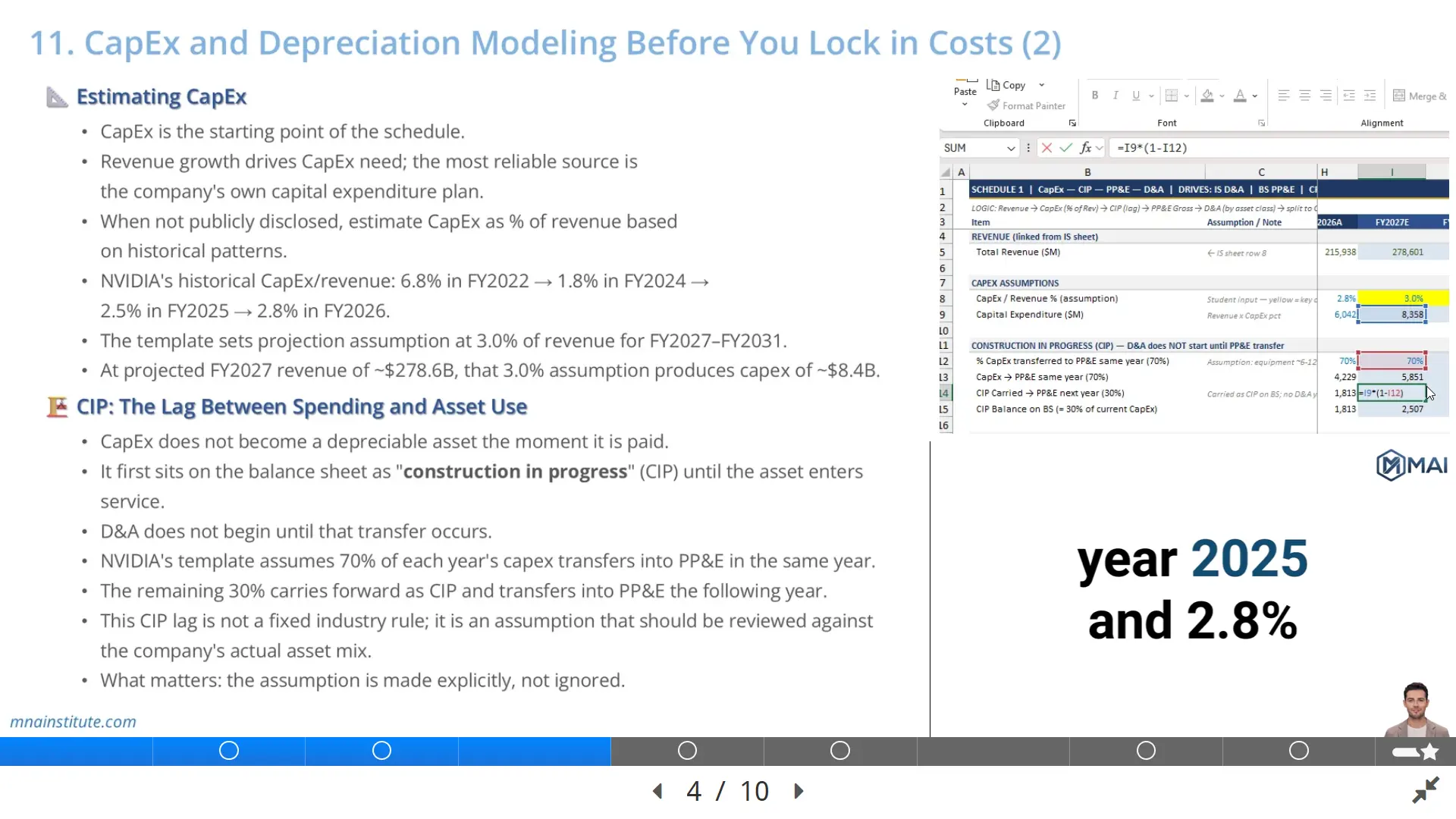

Step 3: Build the 3-Statement Forecast Before Valuation

A DCF model is only as credible as the forecast behind it.

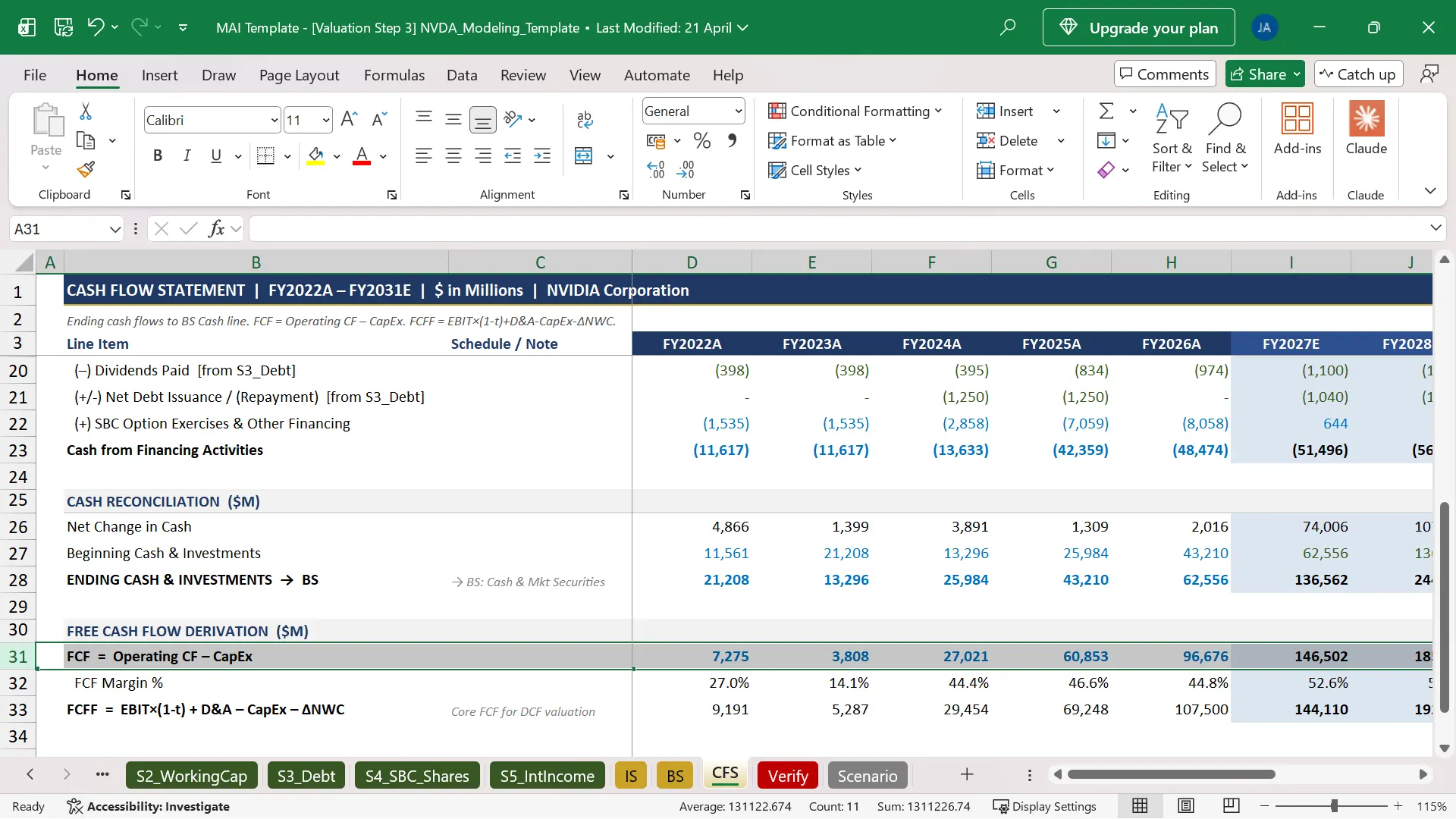

That is why the third step in how to value a company is building a forecast model that connects revenue, expenses, capital expenditure, working capital, debt, interest, tax, EPS, EBITDA, and free cash flow.

A 3-statement model forces discipline because the income statement, balance sheet, and cash flow statement must agree with each other.

For example, revenue growth may require higher receivables, inventory, infrastructure, or capital expenditure.

That means growth does not simply increase profit.

It also affects working capital and free cash flow.

A forecast that ignores this linkage can overstate value.

This is where AI can support the process without replacing judgment.

AI can help extract management guidance, segment data, risk factors, and historical line items from filings.

It can organize revenue drivers and draft assumption commentary.

But the analyst still decides whether those assumptions make business sense.

A serious investment valuation course should make that distinction explicit.

Step 4: Calculate WACC as a Decision Tool

The fourth step in how to value a company is calculating the discount rate.

WACC is not a decorative input.

It is the required return for the capital invested in the business.

In a DCF valuation model, FCFF is discounted at WACC to estimate enterprise value.

That means WACC directly affects whether a company appears undervalued, fairly valued, or overvalued.

A lower WACC increases present value.

A higher WACC reduces present value.

The analyst must therefore understand the cost of equity, cost of debt, capital structure weights, tax shield, beta, equity risk premium, and company-specific risk considerations.

This is not merely technical.

It is judgment about risk.

A company with unstable cash flows, high leverage, or weak competitive position should not be valued with the same discount rate logic as a stable, cash-generative market leader.

When investment valuation training teaches WACC as a decision tool, learners understand why the discount rate can change the entire conclusion.

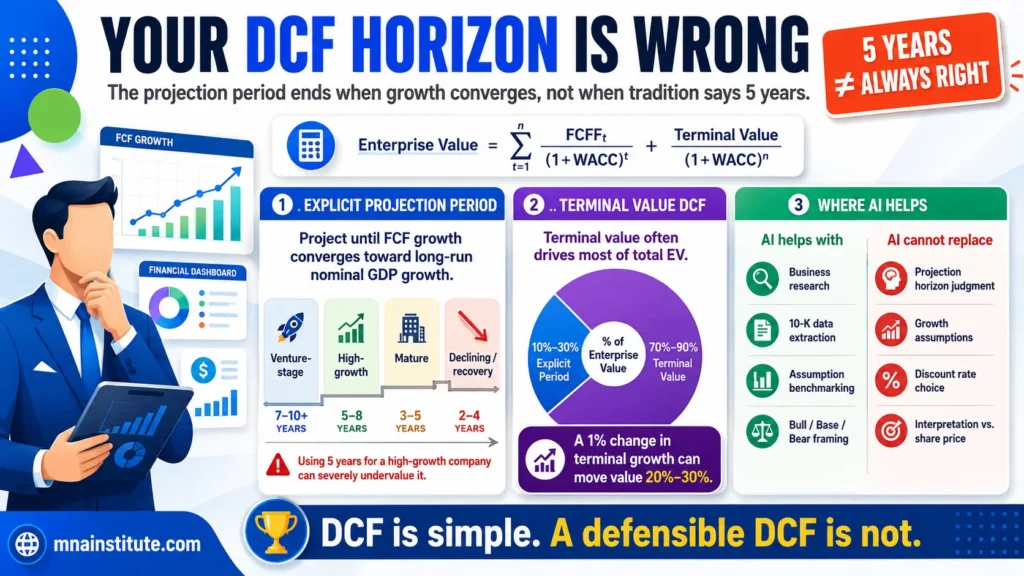

Step 5: Build the DCF Valuation Model

The fifth step in how to value a company is building the DCF valuation model.

The DCF asks a direct question.

What is the present value of the future free cash flow this business can generate?

The basic structure is simple, but the judgment behind it is not.

The analyst must forecast FCFF over an explicit period, estimate terminal value, discount both at WACC, and then bridge enterprise value to equity value.

The enterprise value to equity value bridge matters because debt holders, minority interests, preferred stock, and non-operating assets affect what common shareholders actually own.

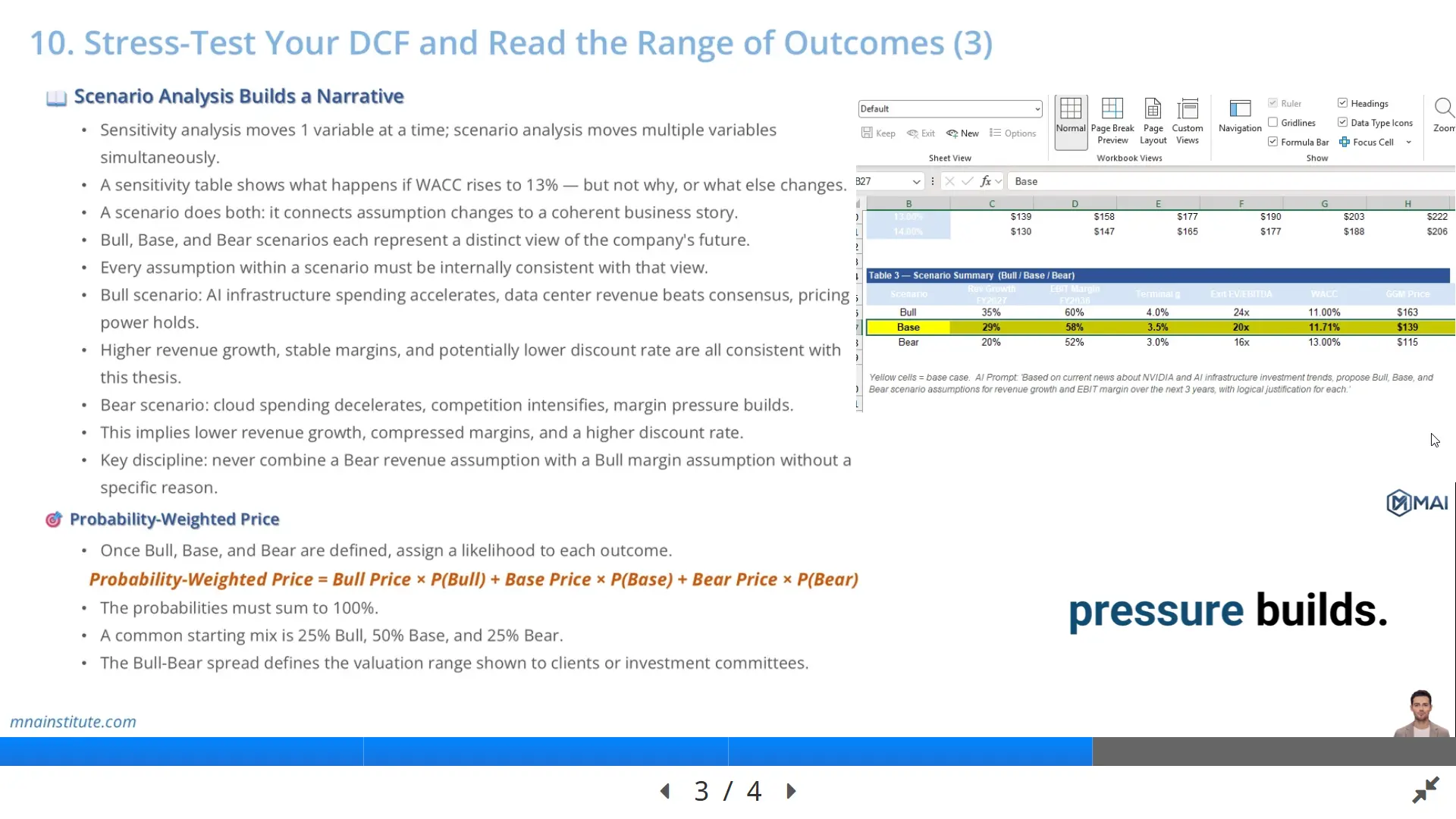

A DCF valuation model also requires sensitivity analysis.

One share price estimate is rarely enough because small changes in WACC, terminal growth, revenue growth, or margin can move value materially.

A defensible model therefore presents a valuation range.

The analyst should be able to explain what drives the low end, the base case, and the high end.

This is where valuation becomes communication, not only calculation.

Step 6: Cross-Check with Comparable Company Analysis

The sixth step in how to value a company is testing the DCF result against market evidence.

Comparable company analysis uses trading multiples from similar public companies to understand how the market prices growth, margins, risk, and capital intensity.

CFA Institute’s market-based valuation material discusses price and enterprise value multiples as tools for relative valuation.

The method is useful because investors rarely look at intrinsic value in isolation.

They compare a company with peers.

If a DCF implies a valuation far above peers, the analyst must explain why.

The company may have better growth, stronger margins, lower risk, higher returns on capital, or a more durable competitive position.

If none of those explanations exists, the DCF assumptions may be too aggressive.

Comparable company analysis is not a replacement for DCF.

It is a market-based cross-check.

The strongest valuation work reconciles intrinsic value and market evidence rather than choosing one blindly.

Step 7: Turn the Model into a Valuation Report

The seventh step in how to value a company is valuation report writing.

This is where many technically capable analysts weaken their work.

They build a model, but fail to explain the conclusion clearly.

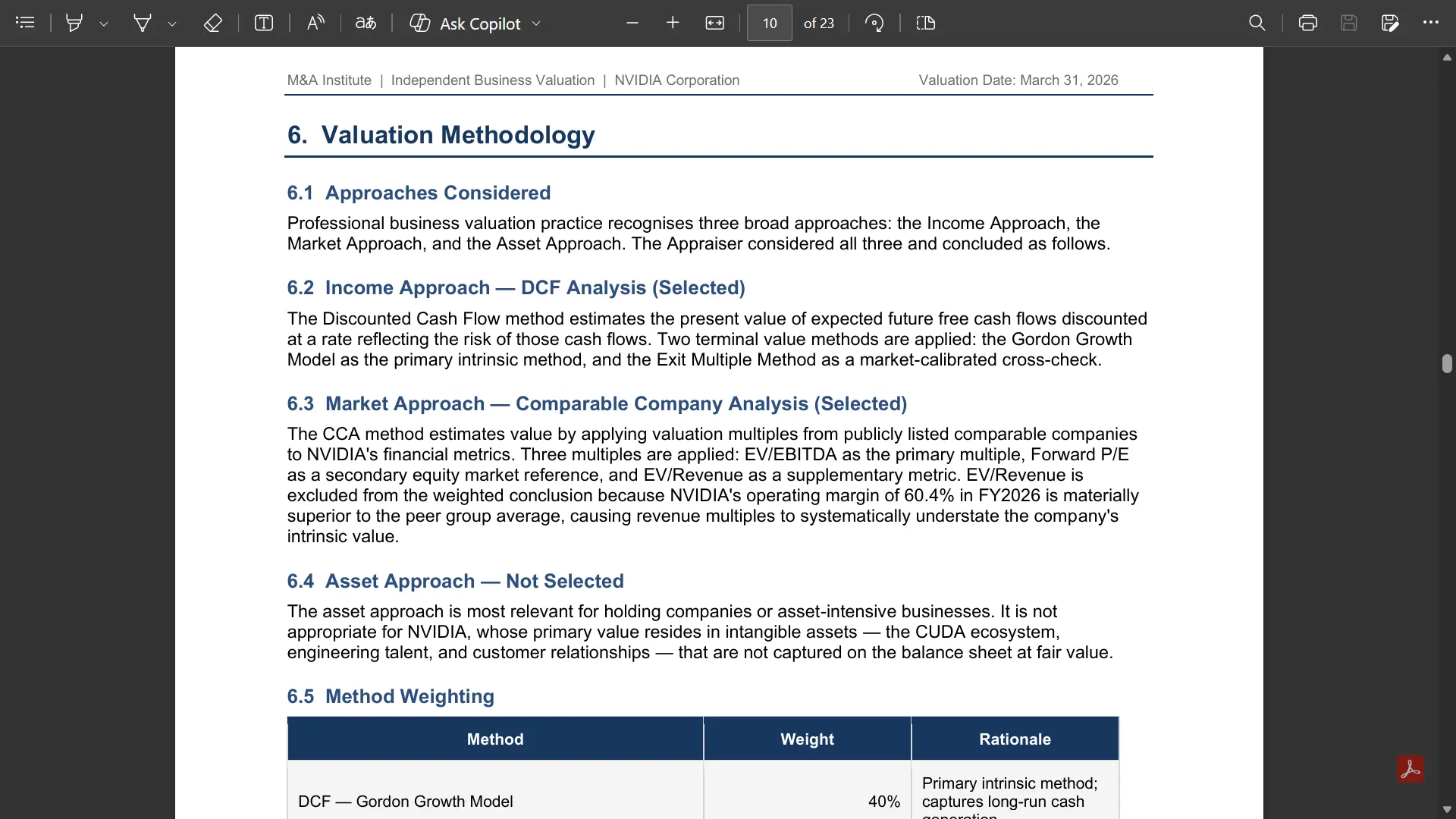

A professional valuation report should not dump spreadsheet outputs into a document.

It should explain purpose, scope, valuation date, methodology, core assumptions, sensitivity, comparable evidence, concluded value, and key risks.

The reader should understand what the analyst believes, why the analyst believes it, and what could change the conclusion.

For example, suppose the DCF valuation model produces an implied share price of $150, while comparable company analysis suggests a range of $130 to $145.

The report should not hide the gap.

It should explain whether the DCF assumes superior growth, higher margins, better capital efficiency, or a lower risk profile than the peer group.

This is why valuation report writing is part of the valuation workflow, not an afterthought.

How AI Fits into the Valuation Workflow

AI changes how fast analysts can collect, structure, and review information.

It does not remove the need for valuation judgment.

Used properly, AI can accelerate several parts of how to value a company.

- Extract revenue, segment, cash flow, debt, and risk factor data from 10-K filings.

- Convert raw tables into model-ready Excel inputs.

- Draft assumption explanations for revenue, margin, CapEx, working capital, WACC, and terminal value.

- Review formulas in a DCF valuation model and flag inconsistencies.

- Organize comparable company data and help draft valuation report writing sections.

The control point is verification.

Every AI output must be checked against source filings, model formulas, and the analyst’s own business understanding.

The value of AI in investment valuation training is therefore speed with audit discipline.

It helps analysts move faster, but it should not decide the valuation conclusion.

What Makes This Investment Valuation Course Different

The course this article is based on includes 7 courses, 105 lessons, 271 learning modules, 353 quizzes, 24 tasks, 13 templates, 3 AI simulations, 3 Excel tasks, and 1 valuation report task.

Those numbers matter because the structure follows the actual valuation workflow from evidence to conclusion.

The sequence moves from valuation fundamentals to financial statement analysis, 3-statement modeling, WACC, DCF, comparable company analysis, and professional report writing.

It also includes applied work using real filings, Excel models, AI prompts, and report outputs.

That is the right structure for anyone asking how to value a company in practice.

The learner does not only read about valuation.

The learner builds the pieces that support a valuation conclusion.

That is what separates investment valuation training from passive finance content.

Example: How the Workflow Converts Data into Value

Consider a simplified example of how to value a company from evidence rather than from a fixed template.

A software company reports revenue growth of 22 percent, but its operating cash flow grows only 8 percent.

A formula-only model might push the historical revenue growth rate forward and produce a high valuation.

A better analyst asks why the cash conversion is weaker than the income statement suggests.

The answer may be rising receivables, customer payment delays, implementation costs, or aggressive revenue recognition.

That finding changes the forecast.

Revenue may still grow, but working capital assumptions become more demanding and FCFF may grow more slowly than EBIT.

The DCF valuation model then reflects lower cash conversion, not only lower accounting profit.

Comparable company analysis adds another test.

If peers with stronger cash conversion trade at 18x EBITDA, the subject company may not deserve the same multiple even if reported growth looks similar.

Valuation report writing then explains the chain clearly.

The report does not simply say the company is worth less.

It explains that the valuation discount comes from weaker cash conversion, higher working capital needs, and lower confidence in forecast free cash flow.

This example shows why investment valuation training must connect accounting, forecasting, DCF, CCA, and writing.

The practical skill is not only knowing how to value a company, but knowing which evidence should change the value.

How to Use the 13 Templates Without Becoming Template-Dependent

Templates are valuable when they teach structure.

They are dangerous when they become substitutes for thinking.

The right way to use a valuation template is to ask what each sheet is trying to prove.

A financial statement analysis template should reveal revenue quality, cost structure, working capital pressure, cash conversion, leverage, and valuation signals.

A 3-statement model template should show how assumptions flow into schedules, statements, EPS, EBITDA, and FCF.

A WACC template should expose the cost of capital logic rather than hide it in one cell.

A DCF valuation model should make FCFF, terminal value, sensitivity, and the enterprise value bridge transparent.

A comparable company analysis template should force peer selection discipline instead of simply copying a peer list.

A valuation report template should help organize the conclusion, not write the conclusion for the analyst.

That is why the best investment valuation course uses templates as training assets, not as shortcuts.

The learner should be able to explain every row, every assumption, and every conclusion.

When that happens, the question how to value a company becomes practical rather than theoretical.

What Good Investment Valuation Training Should Produce

Good investment valuation training should produce three outputs.

- A model that links business analysis to forecast assumptions and valuation outputs.

- A valuation range that explains upside, base case, downside, and sensitivity.

- A written conclusion that a decision maker can understand without opening the spreadsheet.

Those outputs matter because valuation is used to make decisions.

A portfolio manager must decide whether to buy, hold, or sell.

A corporate development team must decide whether to bid, renegotiate, or walk away.

A credit analyst must decide whether cash flow supports debt service.

A founder or CFO must decide whether a valuation argument can be defended to investors.

Each decision requires more than a model.

It requires reasoning.

That is why how to value a company is ultimately a judgment question supported by financial modeling.

The investment valuation course structure should therefore move from data to model, from model to valuation range, and from valuation range to report.

When that chain is clear, valuation becomes a professional skill rather than an Excel routine.

Related Courses

- The main program for this workflow is the Financial Modeling and Valuation Course with AI and Excel, which connects financial statements, forecasting, WACC, DCF, CCA, sensitivity, and valuation report writing.

- The Financial Statement Analysis Course with AI for Equity Research is useful when the learner wants deeper training in 10-K reading, ratio analysis, earnings quality, financial red flags, and AI-assisted financial analysis.

- The 3-Statement Financial Modeling Course with AI is useful when the learner wants to focus on forecast model construction before valuation.

- The Mergers and Acquisitions Online Course, M&A Due Diligence Course, and Post Merger Integration Course are relevant when valuation must be applied to deal screening, diligence, acquisition decisions, and post-deal value creation.

Sources

- SEC Investor Bulletin: How to Read a 10-K – SEC guidance on reading 10-K filings and using business, risk, MD&A, and financial statement disclosure as investor information.

- CFA Institute: Free Cash Flow Valuation – Free cash flow valuation reference covering FCFF and FCFE approaches to company and equity valuation.

- CFA Institute: Market-Based Valuation, Price and Enterprise Value Multiples – Reference for using price and enterprise value multiples in relative valuation and peer comparison.

- Aswath Damodaran: Discounted Cash Flow Valuation – Academic valuation reference covering DCF logic, cash flow forecasting, discount rates, terminal value, and value bridges.