Weighted Average Cost of Capital WACC Formula: 2 Weights

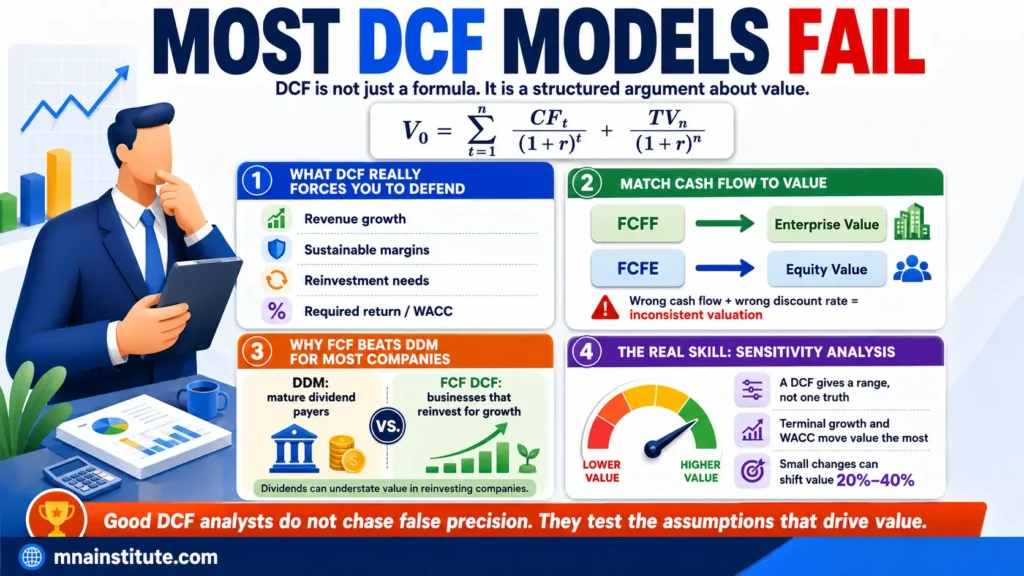

A valuation model can look precise while using the wrong discount rate.

That is why the weighted average cost of capital WACC formula deserves attention before an analyst starts building a DCF model.

WACC is the rate that connects expected future free cash flow to present company value.

It also functions as a hurdle rate when management decides whether a project earns more than the capital required to fund it.

The formula looks simple, but the interpretation is where many valuation mistakes begin.

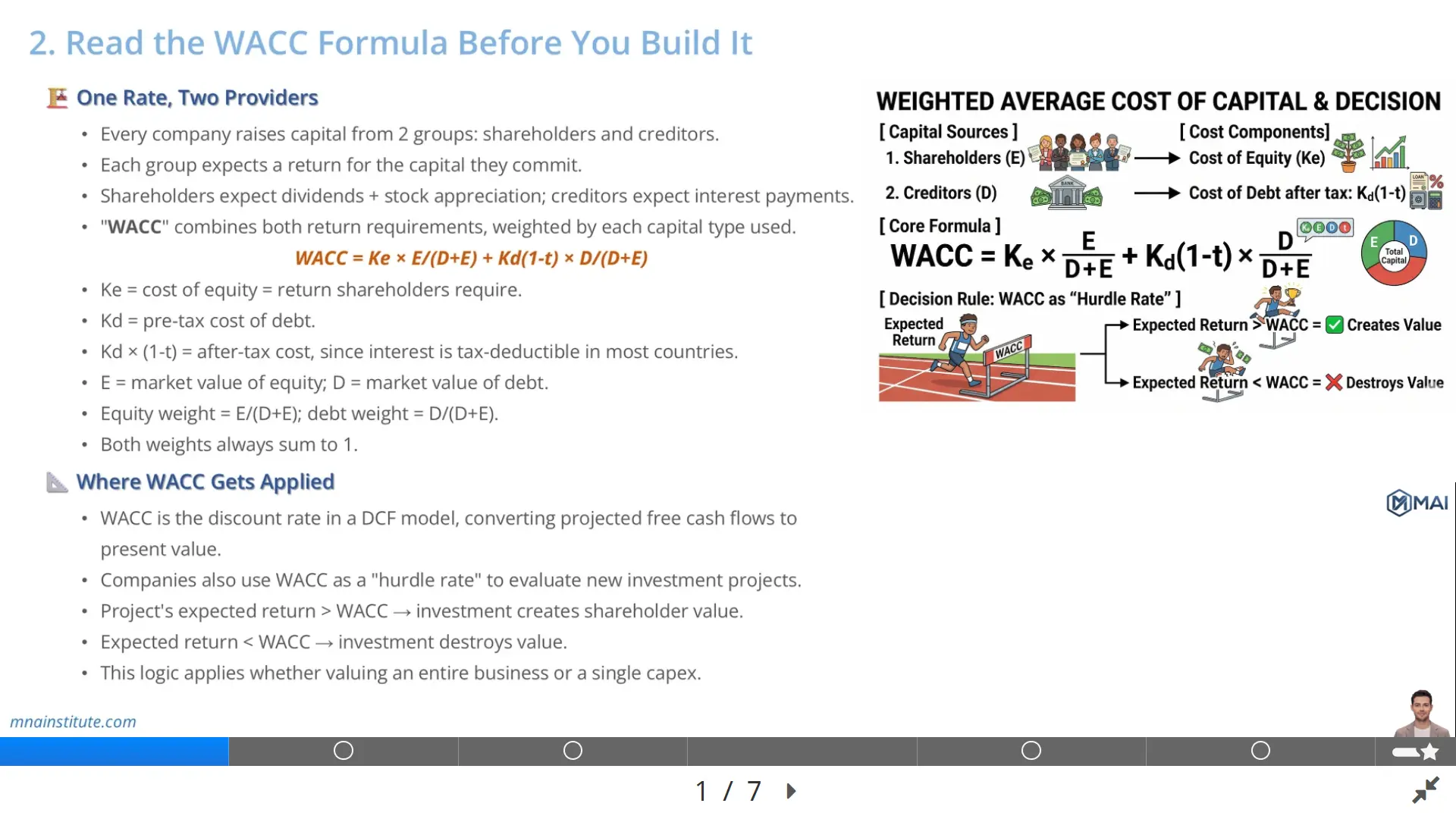

A company is not funded by one capital provider.

It is funded by shareholders who provide equity and creditors who provide debt.

Each group expects a return, and the WACC calculation blends those required returns according to the company’s capital structure weights.

The most practical lesson is that the weights should normally come from market value, not book value.

A DCF valuation asks what the business is worth today, so the discount rate should reflect what capital costs today, not what it cost historically.

This article walks through the WACC equation, explains the two weights, applies the logic to NVIDIA, and shows where analyst judgment still matters.

Quick Comparison: Formula Knowledge vs Analyst-Ready WACC Judgment

|

Question |

Basic Formula Answer |

Analyst-Ready Answer |

|

What is WACC? |

A weighted average of equity and debt costs. |

The discount rate for FCFF and the hurdle rate for capital allocation. |

|

Which weights matter? |

Equity weight and debt weight. |

Market value weights that reflect current financing costs and target capital structure. |

|

What makes it risky? |

The formula can be calculated incorrectly. |

The input choices can be economically inconsistent with the business risk and forecast horizon. |

Why the Weighted Average Cost of Capital WACC Formula Starts with Two Providers

The weighted average cost of capital WACC formula begins with a basic financing reality.

Every operating business uses capital, and that capital usually comes from equity holders and debt holders.

Shareholders provide equity capital and expect compensation through dividends, retained value creation, and stock price appreciation.

Creditors provide debt capital and expect compensation through scheduled interest payments and repayment of principal.

Those two groups do not hold the same type of claim on the business.

Creditors are paid before shareholders and their claim is contractual.

Shareholders receive residual value after the obligations to creditors and other stakeholders have been satisfied.

That difference explains why the cost of equity is normally higher than the cost of debt.

Equity investors absorb more uncertainty, so they demand a higher expected return.

Debt investors accept lower upside because they receive fixed payments and have seniority in the capital structure.

The weighted average cost of capital WACC formula combines these required returns into one rate.

It does not say that debt and equity are economically identical.

It says that the company-level discount rate must reflect how much of each funding source the company uses.

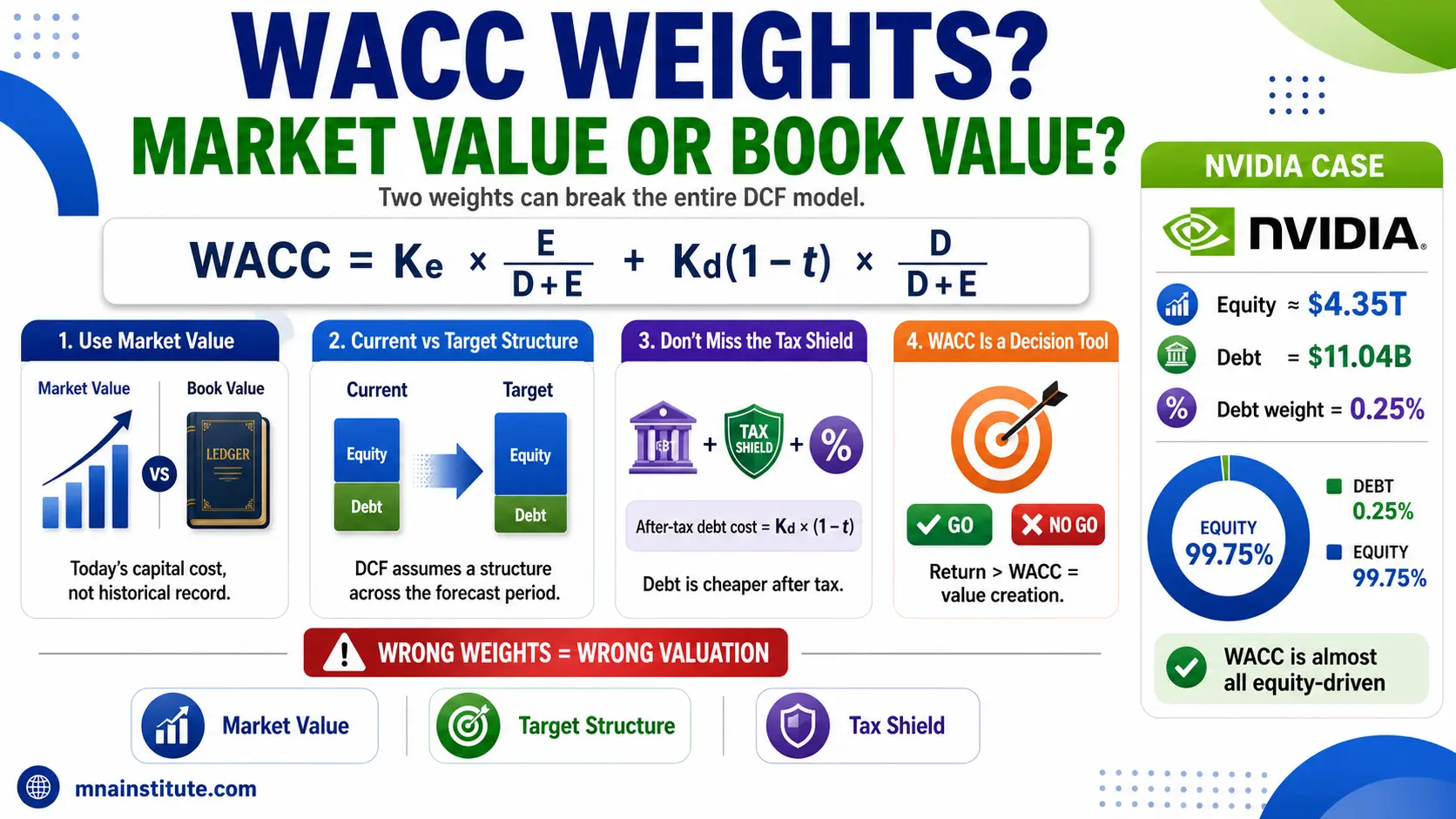

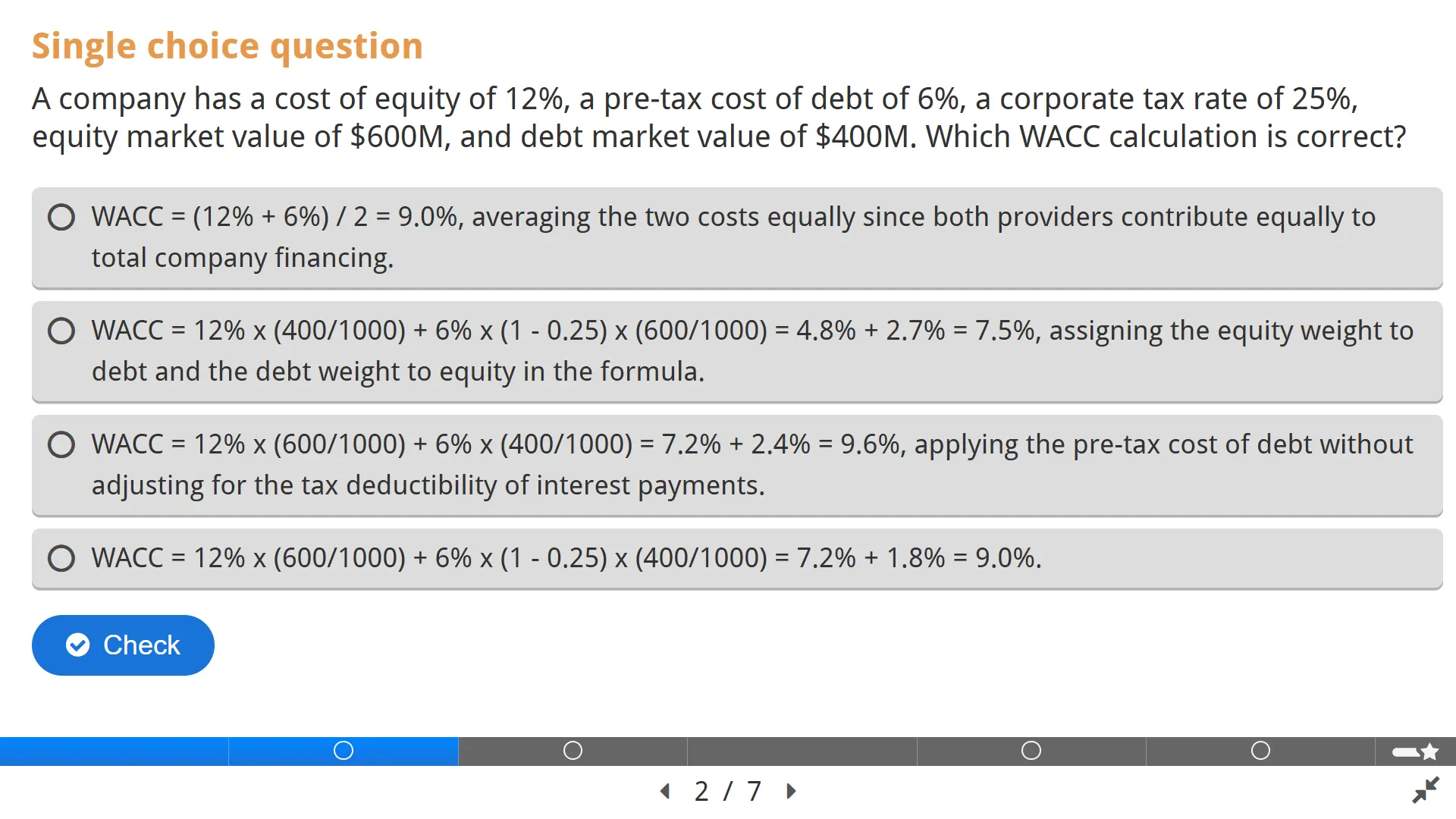

The standard WACC equation is simple.

WACC = Ke × E / (D + E) + Kd × (1 – t) × D / (D + E)

Ke is the cost of equity, which represents the return shareholders require.

Kd is the pre-tax cost of debt, which reflects the return creditors require before tax effects.

E is the market value of equity and D is the market value of debt.

Equity weight = E / (D + E)

Debt weight = D / (D + E)

Together, the two capital structure weights sum to 100 percent.

If the company is almost entirely equity funded, the cost of equity drives the final WACC.

If the company uses significant debt, the after-tax cost of debt becomes more influential.

The formula therefore gives structure to a judgment that analysts must make carefully.

Where WACC Gets Applied in Valuation and Capital Budgeting

The weighted average cost of capital WACC formula is most visible in DCF valuation.

A discounted cash flow model forecasts FCFF and discounts each forecast period back to the present.

WACC is the discount rate used because FCFF belongs to all capital providers before the cash flow is split between shareholders and creditors.

If WACC is too low, the DCF valuation will overstate enterprise value.

If WACC is too high, the valuation will understate enterprise value.

The sensitivity is especially strong when terminal value represents a large share of total enterprise value.

A small movement in WACC can shift implied share price meaningfully because terminal value is discounted through that rate.

WACC also appears outside valuation models.

Companies use WACC as a hurdle rate for capital allocation.

A project that earns less than WACC does not cover the required return of the capital used to fund it.

A project that earns more than WACC can create shareholder value because it generates returns above the blended cost of financing.

For example, suppose a business is considering a new data center investment requiring 500 million dollars of upfront capital.

If the project’s expected return is 13 percent and the company’s WACC is 9 percent, the project appears value creating before considering execution risk.

If the expected return is 6 percent and WACC is 9 percent, the project consumes capital without earning the required return.

This is why WACC is not only a spreadsheet input.

It is a decision rule for whether a company should accept or reject investment opportunities.

The same logic applies in M&A valuation.

If an acquisition’s expected return falls below the acquirer’s cost of capital after including price, integration costs, and risk, the transaction destroys value even if it looks strategically attractive.

That is why serious valuation work links WACC calculation to the business case, not just to formula mechanics.

The formula is the starting point, but the judgment is whether the rate matches the cash flow risk being discounted.

Why Capital Structure Weights Drive the Final Rate

The WACC formula requires two weights: the share of equity in total capital and the share of debt in total capital.

Equity weight = E / (D + E)

Debt weight = D / (D + E)

These capital structure weights determine how strongly the cost of equity and the after-tax cost of debt affect the final discount rate.

The practical question is which capital structure the analyst should use.

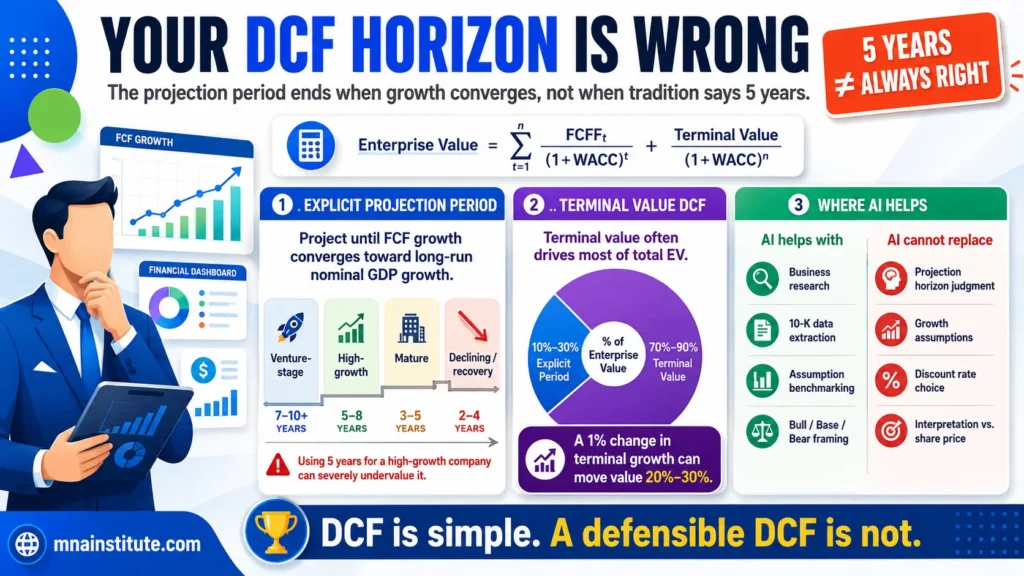

A DCF model often projects free cash flow for five to ten years and then estimates terminal value beyond that period.

If the analyst uses today’s capital structure, the model implicitly assumes that today’s mix of debt and equity remains appropriate for the entire forecast horizon.

For a mature, stable company, that may be a reasonable simplifying assumption.

For a high-growth company, it may be misleading.

A business that is almost entirely equity funded today may use more debt later as cash flows become more predictable.

A company under temporary stress may have a debt weight today that should not represent its long-run steady-state structure.

This is why analysts often think in terms of target capital structure.

Target capital structure means the financing mix the company is expected to settle into over time.

It may be based on management policy, industry averages, credit rating targets, peer leverage, or the company’s long-run business risk.

Capital structure weights also affect interpretation of the tax shield.

Debt can lower WACC because interest is tax-deductible in many jurisdictions.

However, adding debt also raises financial risk and may increase both the cost of debt and the cost of equity.

A simplistic assumption that more debt always lowers WACC is dangerous.

The analyst must consider whether the company can sustain that debt without increasing distress risk.

A disciplined WACC calculation therefore treats the weights as a capital structure judgment, not a mechanical lookup.

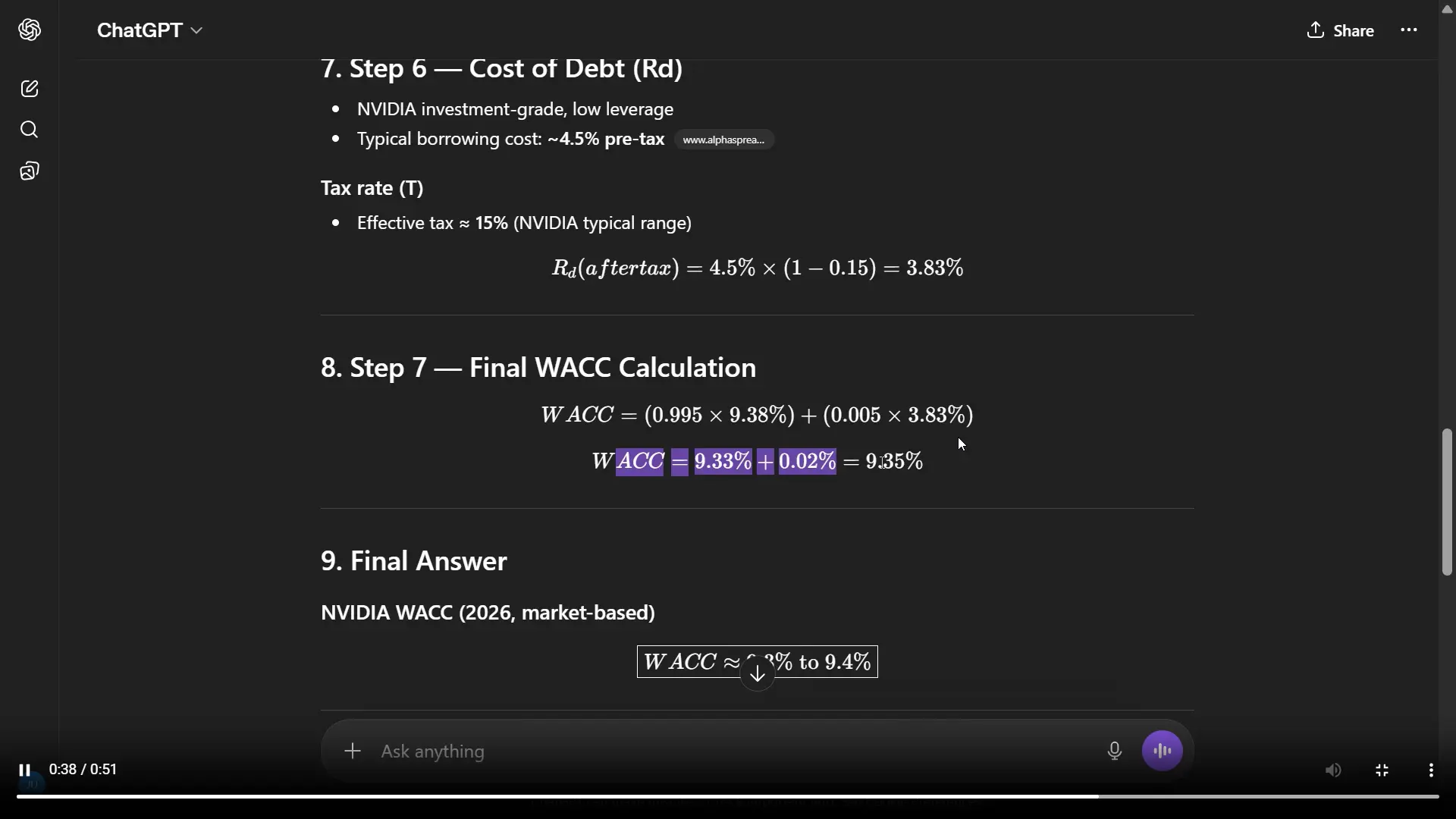

NVIDIA Example: Market Value Weights WACC in Practice

NVIDIA illustrates why market value weights WACC can look very different from book-based thinking.

Using the figures provided in this module, NVIDIA’s share price is 178.71 dollars and shares issued are 24,304 million.

That implies a market value of equity of approximately 4.345 trillion dollars.

The module uses total debt of approximately 11.04 billion dollars.

The debt-to-equity ratio is therefore roughly 0.25 percent based on those market value inputs.

This means the current market value capital structure is almost entirely equity funded.

In that situation, the weighted average cost of capital WACC formula will be driven primarily by the cost of equity.

Even if NVIDIA has a positive cost of debt, the debt weight is so small that the after-tax debt component has limited influence on final WACC.

The analyst should not stop there.

The harder question is whether this capital structure represents NVIDIA’s long-run financing mix.

A fast-growing technology company can have a very large equity value during a market cycle and relatively modest debt usage.

If the company matures, generates more predictable cash flows, and chooses to optimize its balance sheet differently, the future debt weight may rise.

That does not mean the analyst should automatically impose a high debt ratio.

It means the analyst should test whether the current structure, industry peer structure, or a target structure is more reasonable for the valuation purpose.

For a base case valuation, one approach is to start with current market value weights and then review industry averages.

For a more rigorous forecast, the model can allow capital structure weights to change gradually as the company matures.

This year-by-year approach is more complex, but it may better reflect a company transitioning from exceptional growth to a steadier stage.

The NVIDIA example also shows why WACC calculation cannot be separated from business analysis.

A spreadsheet can compute the ratio in seconds.

Only the analyst can decide whether the ratio is economically representative.

Market Value, Not Book Value

Capital structure weights should generally be based on market values, not book values.

The reason is straightforward.

Companies raise new capital at market prices.

When a company issues new shares, the relevant price is the market price investors are willing to pay today.

When a company issues debt, the relevant cost is based on current credit market conditions and the return demanded by lenders or bond investors today.

Book value records historical accounting amounts.

It may be useful for financial reporting, but it does not necessarily describe what capital would cost now.

For equity, market value is usually market capitalization.

Market capitalization = Share Price × Shares Outstanding

For debt, market value can be more difficult because some debt instruments do not trade actively.

For investment-grade companies, analysts sometimes use book debt as a practical approximation when the gap between book value and market value is not material.

For distressed companies or companies with large rate-sensitive debt positions, that shortcut may be inaccurate.

Market value weights WACC therefore requires judgment about data quality.

The analyst should identify whether debt is traded, whether bond prices are available, and whether book debt is a reasonable proxy.

For equity, the analyst should consider whether a single day’s share price is representative.

A volatile stock can produce a very different equity weight depending on the market snapshot used.

Some analysts use an average market capitalization over a recent period to reduce point-in-time noise.

That approach is especially useful when the valuation date is close to an unusual market event.

The broader principle is simple.

The WACC calculation should use inputs that reflect economic reality at the valuation date and the expected financing mix over the forecast period.

Why WACC Has Real Limits and How AI Should Be Used

The weighted average cost of capital WACC formula is necessary, but it has limits.

The first limit appears when one company operates several businesses with different risk profiles.

A semiconductor design business and a financial services business may sit inside the same corporate group, but their cash flow risks are not the same.

Using one blended WACC across both divisions can overvalue the riskier division and undervalue the more stable division.

A sum-of-the-parts analysis may require division-specific discount rates.

The second limit appears when a company’s risk changes over time.

A company may be high growth today and more mature ten years from now.

A single fixed WACC may not capture that transition.

A more advanced DCF can use different discount rates by period or adjust capital structure over time.

That approach should be used carefully because it introduces more assumptions and more room for inconsistency.

The third limit is false precision.

A WACC of 11.71 percent looks precise, but the inputs behind it may contain estimation uncertainty.

Beta, equity risk premium, cost of debt, tax rate, and target capital structure are all judgmental to some degree.

This is where AI can be useful as an accelerator.

Before calculating each input manually, an analyst can ask AI to generate an initial estimate and show each step.

For example, the analyst can request a WACC estimate for NVIDIA using recent fiscal data, market value weights, the current 10-year US Treasury yield, Damodaran’s implied equity risk premium, and an adjusted beta.

The AI output should not be accepted as final.

It should be used as a benchmark against the analyst’s own calculation.

The analyst should verify market capitalization, debt, tax rate, risk-free rate, beta source, and peer leverage before using the result.

AI can help collect evidence and expose missing inputs.

It cannot decide whether the final WACC is appropriate for the specific business, forecast horizon, and valuation purpose.

Worked NVIDIA Snapshot Used in the Module

The table below summarizes the market value weight logic used in the NVIDIA example from the lesson.

The purpose is not to claim a permanent capital structure, but to show how market value weights can dominate the WACC calculation when equity value is very large relative to debt.

|

Input |

Module Figure |

Analytical Meaning |

|

Share price |

$178.71 |

Market price used to estimate equity value |

|

Shares issued |

24,304 million |

Share count used in market capitalization |

|

Market value of equity |

About $4.345 trillion |

Dominant funding source in current weights |

|

Total debt |

About $11.04 billion |

Small relative to market equity value |

|

D/E |

About 0.25% |

Current capital structure is almost entirely equity funded |

Related Courses

A complete valuation workflow connects WACC to the cash flows and decisions it is meant to support.

- The Financial Modeling and Valuation Course with AI and Excel covers financial statement analysis, 3-statement modeling, WACC, DCF, CCA, sensitivity, and valuation report writing as one connected process.

- The Financial Statement Analysis Course with AI for Equity Research is useful before WACC because it trains the analyst to read filings and identify the cash flow drivers that later enter the DCF.

- The 3-Statement Financial Modeling Course with AI shows how business research becomes revenue assumptions, schedules, EPS, EBITDA, and free cash flow.

- The Mergers and Acquisitions Online Course and M&A Due Diligence Course connect valuation judgment to deal screening, risk review, and transaction decision-making.

- The Post Merger Integration Course is relevant when the valuation depends on whether a buyer can actually deliver the operating improvements assumed in the model.

Sources

- CFA Institute, Cost of Capital: Advanced Topics

- Aswath Damodaran, Cost of Equity and Capital data

- Aswath Damodaran, Finding the Right Financing Mix: The Capital Structure Decision

- NVIDIA Investor Relations, Annual Reports and Proxies