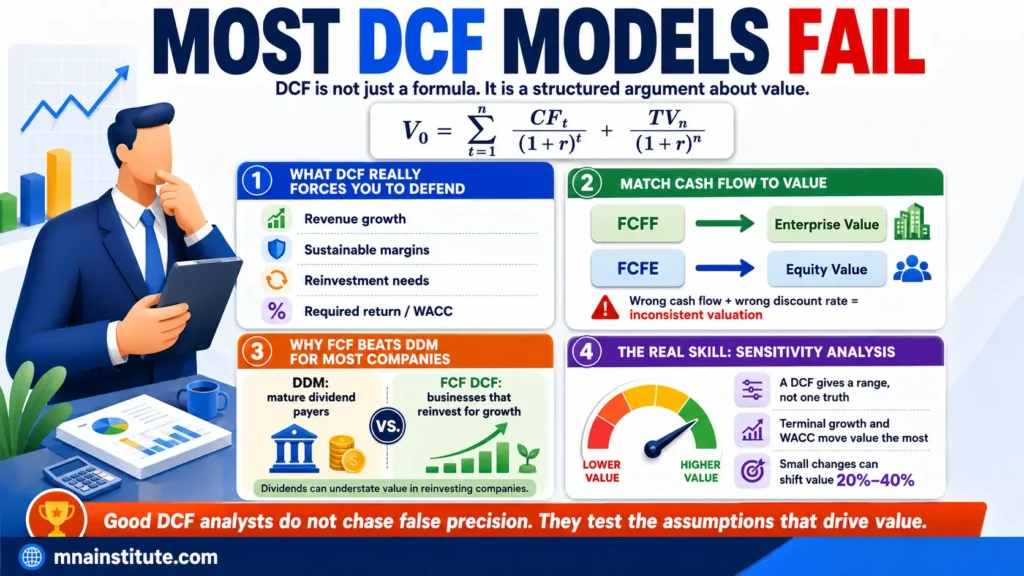

FCFF vs FCFE: Free Cash Flow to Equity in 2 Steps

Many valuation mistakes start with a simple ownership question.

Who does the cash flow belong to?

That question is the practical core of FCFF vs FCFE.

FCFF measures cash flow before the business is split between shareholders and creditors.

FCFE measures the cash left for shareholders after creditor claims and net borrowing have been reflected.

This difference changes the valuation output.

When an analyst discounts FCFF at WACC, the output is Enterprise Value.

When an analyst discounts free cash flow to equity at the cost of equity, the output is Equity Value directly.

That is why FCFE is not just another free cash flow label.

It is a shareholder cash flow measure with a different discount rate, a different ownership perspective, and a different use case.

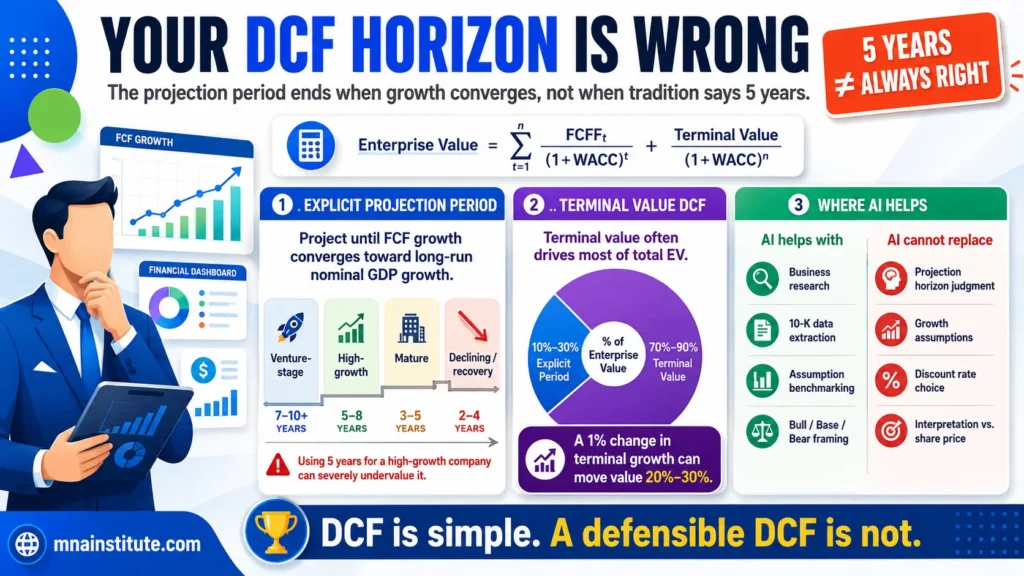

This article explains FCFF vs FCFE by teaching free cash flow to equity through two practical adjustments from FCFF.

It also shows why the FCFE formula is simple, why the FCFE calculation changes with leverage, and why FCFF remains the standard in most corporate valuation work.

By the end, FCFF vs FCFE should feel less like a textbook distinction and more like a practical choice about which claim, which cash flow, and which valuation output the analyst is actually measuring.

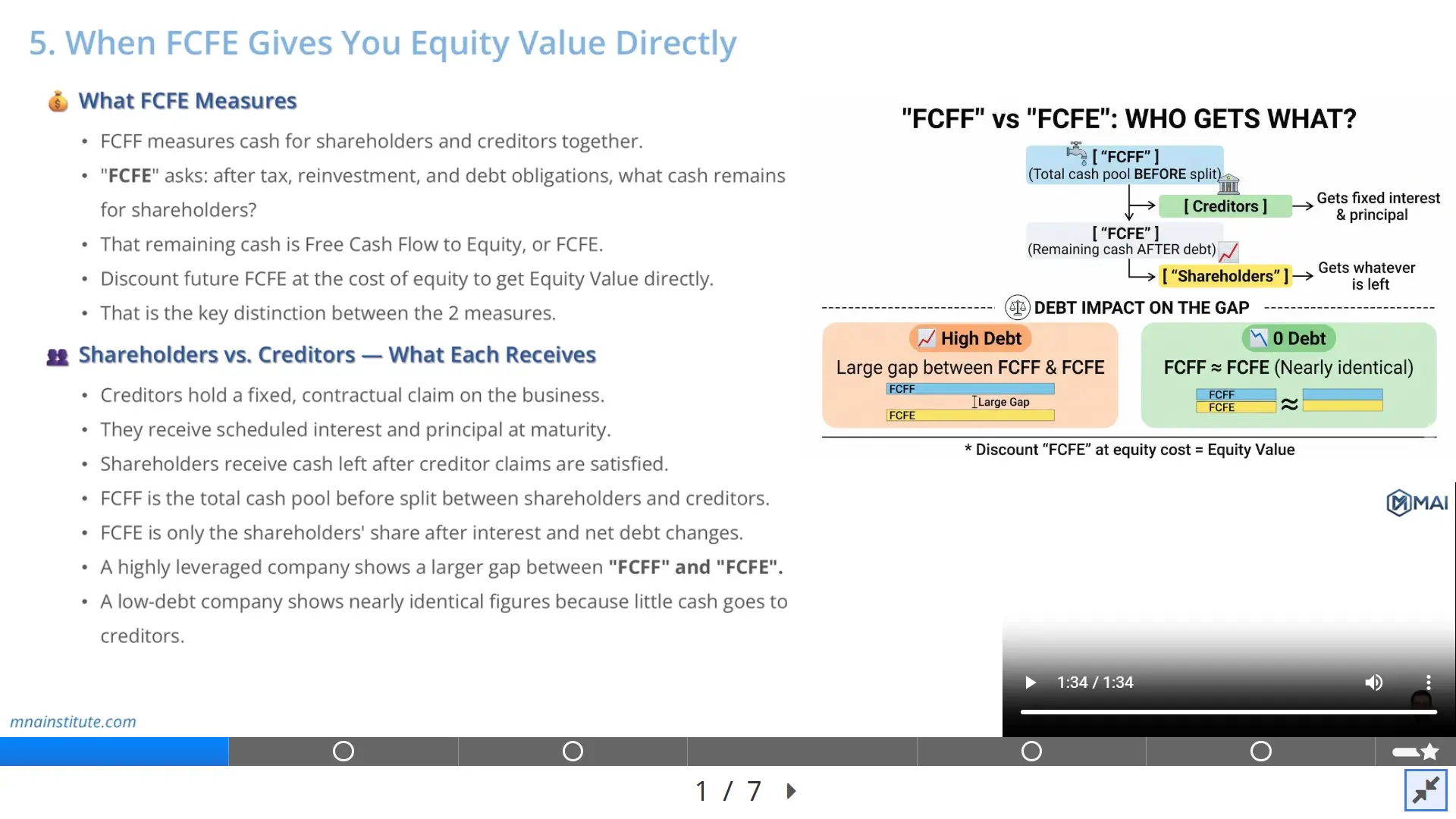

What FCFE Measures

Free cash flow to equity asks a narrower question than FCFF.

After a company pays operating costs, pays taxes, reinvests in the business, and satisfies creditor obligations, how much cash remains for shareholders?

That remaining cash is FCFE.

The FCFE meaning is therefore shareholder-specific.

It is not the full operating cash pool of the business.

It is the portion of cash flow that remains after lenders have received their contractual share through interest payments and debt repayments.

This is the first distinction in FCFF vs FCFE.

FCFF is cash flow available to all capital providers.

FCFE is cash flow available only to equity holders.

That difference is why the two cash flow measures connect to different values.

FCFF is discounted at WACC because WACC represents the blended required return of debt and equity capital providers.

The result is Enterprise Value, which reflects the value of the operating business before separating debt and equity claims.

FCFE is discounted at the cost of equity because only shareholders receive this cash flow.

The result is Equity Value directly, with no enterprise value bridge required.

This is useful when the analyst wants to value the common equity claim without separately subtracting net debt, preferred stock, or minority interests from Enterprise Value.

However, that convenience comes with a condition.

The company must have a financing structure that can be forecast with reasonable confidence.

If debt levels, interest costs, and refinancing assumptions are unstable, the FCFE calculation becomes more difficult to forecast than FCFF.

FCFF vs FCFE at a Glance

The easiest way to understand FCFF vs FCFE is to compare what each number includes and what valuation result it produces.

|

Question |

FCFF |

FCFE |

Valuation Output |

|

Who receives it? |

Shareholders and creditors |

Shareholders only |

Enterprise Value for FCFF, Equity Value for FCFE |

|

Where does it sit? |

Before financing costs |

After creditor payments and net borrowing |

Different ownership claim |

|

Discount rate |

WACC |

Cost of equity |

Rate must match the cash flow |

|

Best use case |

Operating business valuation |

Direct equity valuation |

Depends on leverage and forecast reliability |

The table shows why free cash flow to equity is not interchangeable with FCFF.

The two measures may look similar for a low-debt company, but they can diverge sharply when leverage is high.

The reason is not accounting complexity.

The reason is capital structure.

Debt creates a prior claim on business cash flow before shareholders receive anything.

Interest expense is the cost of that claim, and debt repayment reduces cash available to equity holders.

New debt issuance has the opposite effect because it increases cash available to shareholders, at least in the period when the borrowing occurs.

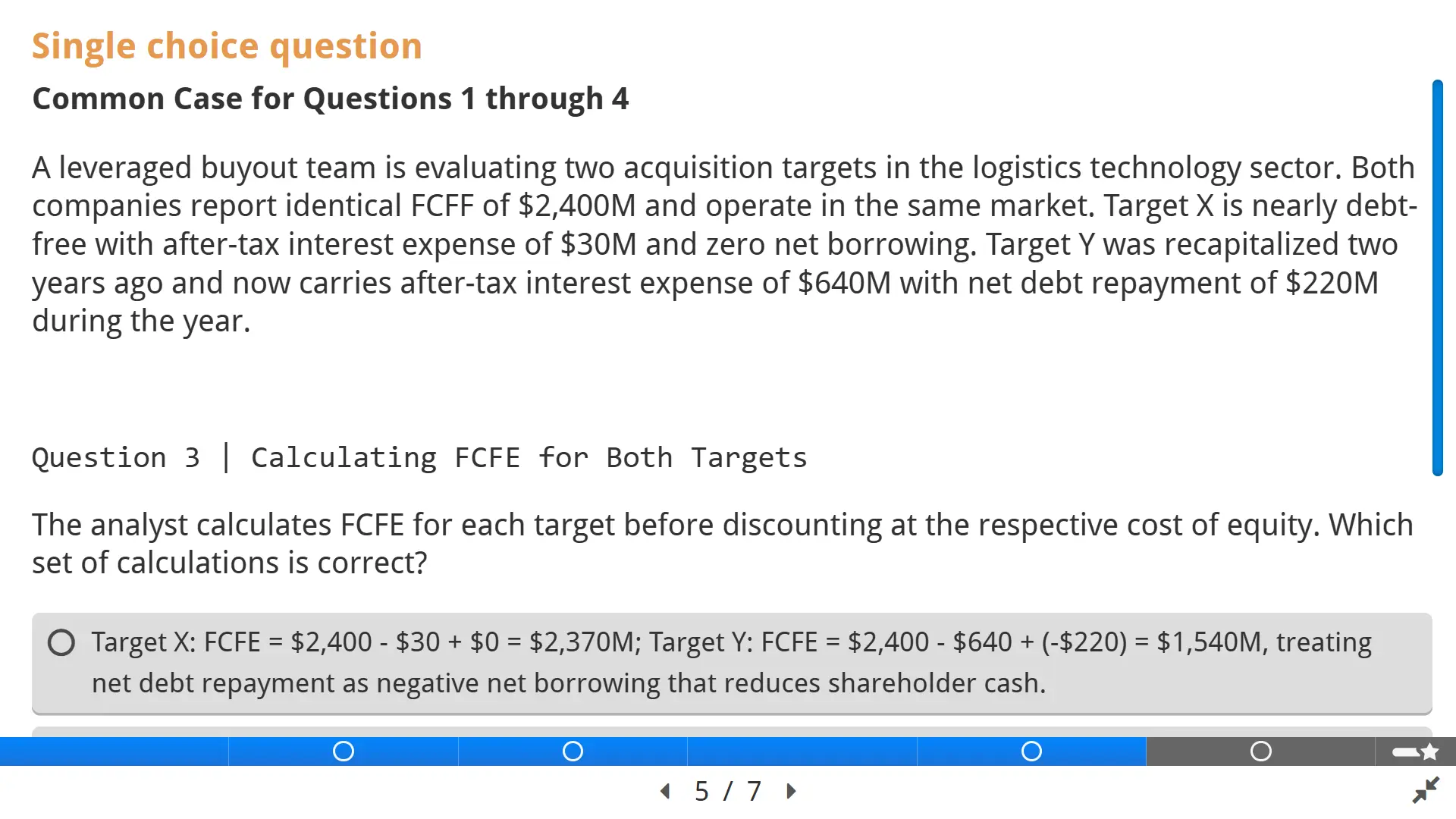

This is why FCFF vs FCFE becomes especially relevant when a company has material leverage, recurring refinancing needs, or a business model where debt is part of operating activity.

Shareholders vs. Creditors: What Each Receives

Creditors and shareholders do not own the same economic claim.

Creditors have a fixed contractual claim.

They receive interest on schedule and principal according to the debt agreement, regardless of whether shareholders ultimately earn a high or low return.

Shareholders own the residual claim.

They receive whatever remains after operating needs, tax obligations, reinvestment, and creditor claims have been handled.

This is why FCFF vs FCFE is fundamentally a claim-order issue.

FCFF sits before the financing layer.

It measures the total cash flow generated by the operating business for all capital providers.

FCFE sits after the financing layer.

It measures the shareholder portion of that cash flow after after-tax interest and net borrowing effects are included.

Consider a simple business with $100 million of FCFF before debt service.

If the company has no debt, free cash flow to equity may be close to $100 million.

If the company has after-tax interest of $20 million and no new borrowing, free cash flow to equity falls to $80 million.

If the same company then repays $30 million of debt principal, equity holders have only $50 million of available cash.

If instead the company raises $30 million of new debt, FCFE increases in that period because net borrowing adds cash available to equity.

The operating business has not changed in these scenarios.

What changed is the split of cash flow between creditors and shareholders.

That is why FCFF is cleaner for analyzing operations, while FCFE is more direct for analyzing equity distributions.

The FCFE Formula in Two Practical Steps

The FCFE formula used in this lesson starts from FCFF and then adjusts for creditor payments and net borrowing.

The formula is:

FCFE = FCFF – Interest x (1 – tax rate) + Net Borrowing

In spreadsheet models, analysts usually write this as after-tax interest because the tax shield reduces the true cash cost of debt.

The logic is more important than the notation.

Free cash flow to equity starts with total firm cash flow and removes the cash that belongs to creditors.

Then it adds the net cash effect of borrowing or repaying debt.

Step 1: Subtract after-tax interest

Interest expense belongs to creditors.

It is not cash available to shareholders.

Because interest is tax deductible in many corporate tax systems, the relevant deduction from FCFF is after-tax interest rather than pre-tax interest.

This adjustment removes the creditor portion of the cash flow from the shareholder cash flow measure.

In FCFF vs FCFE terms, this is the point where the model moves from the total capital-provider view to the equity-holder view.

Step 2: Add net borrowing

Net borrowing is debt issued minus debt repaid during the period.

New debt raised increases cash available to shareholders because it brings new financing into the company.

Debt repayment reduces cash available to shareholders because cash leaves the business to repay creditors.

This is why the FCFE calculation is sensitive to financing policy.

A company can increase free cash flow to equity in the short term by borrowing more, even if the operating business has not improved.

That does not mean the company has created operating value.

It means financing has changed the shareholder cash flow for that period.

How to Calculate FCFE from FCFF

The cleanest way to learn how to calculate FCFE is to start with FCFF and then walk down the financing layer.

The process has two calculation lines, but each line requires judgment.

- Confirm the FCFF figure and make sure it reflects operating cash flow before interest.

- Calculate after-tax interest using the company-specific effective tax rate or an appropriate normalized tax rate.

- Identify net borrowing by comparing debt issued with debt repaid during the period.

- Subtract after-tax interest and add net borrowing to arrive at FCFE.

- Check whether the result makes economic sense relative to dividends, share repurchases, leverage, and the company life cycle.

The fifth check prevents mechanical modeling errors.

If FCFE is strongly positive while the company is borrowing heavily, the analyst must separate operating cash generation from financing-driven cash availability.

If FCFE is negative for a growing company, the result may reflect heavy reinvestment, large debt repayment, or both.

If FCFE is persistently negative while the company is still paying dividends or repurchasing shares, the analyst should question the sustainability of those distributions.

That is where FCFE meaning becomes practical.

It is not just a formula.

It is a test of whether equity holders are receiving cash from operating strength or from financing choices.

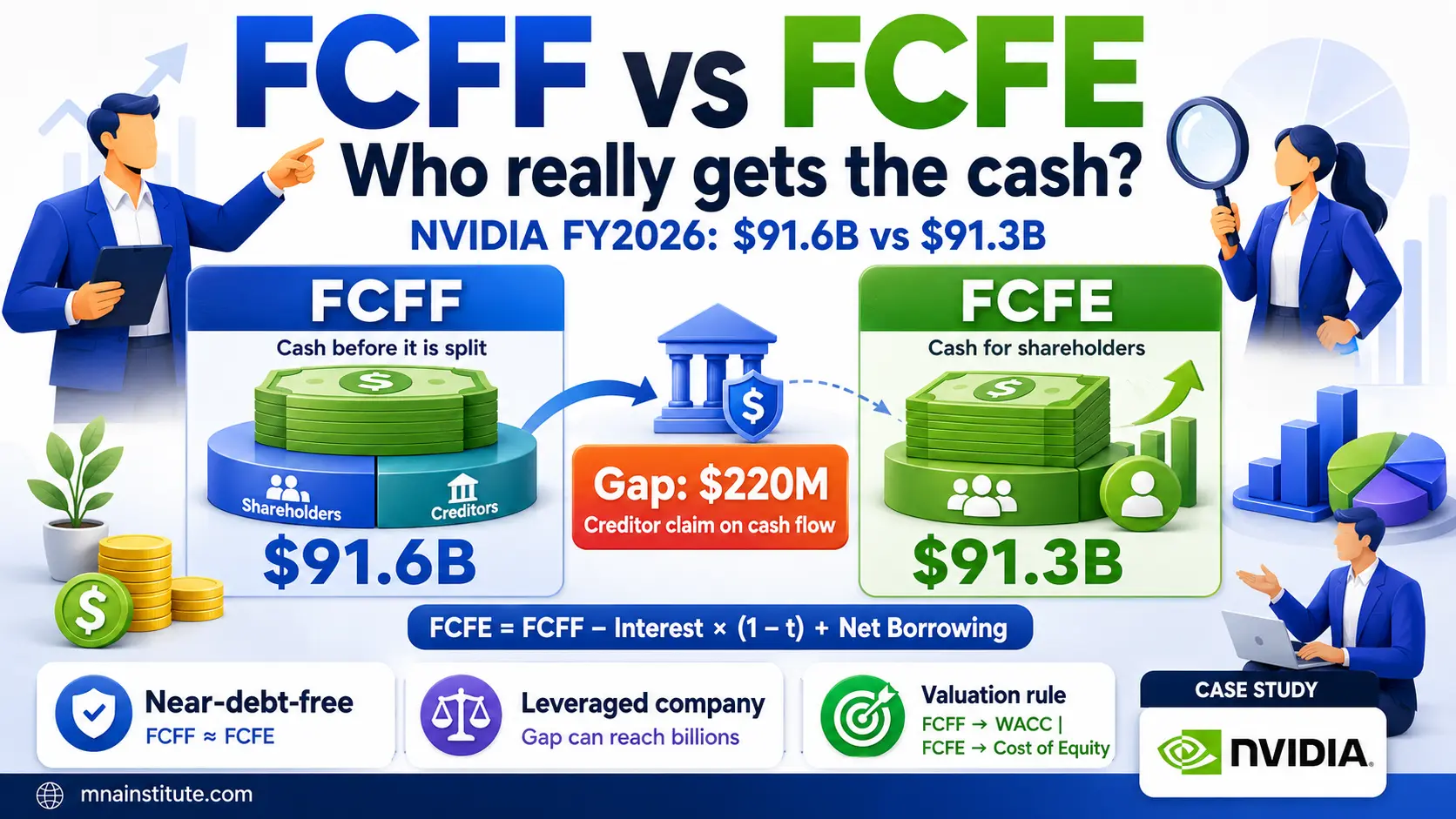

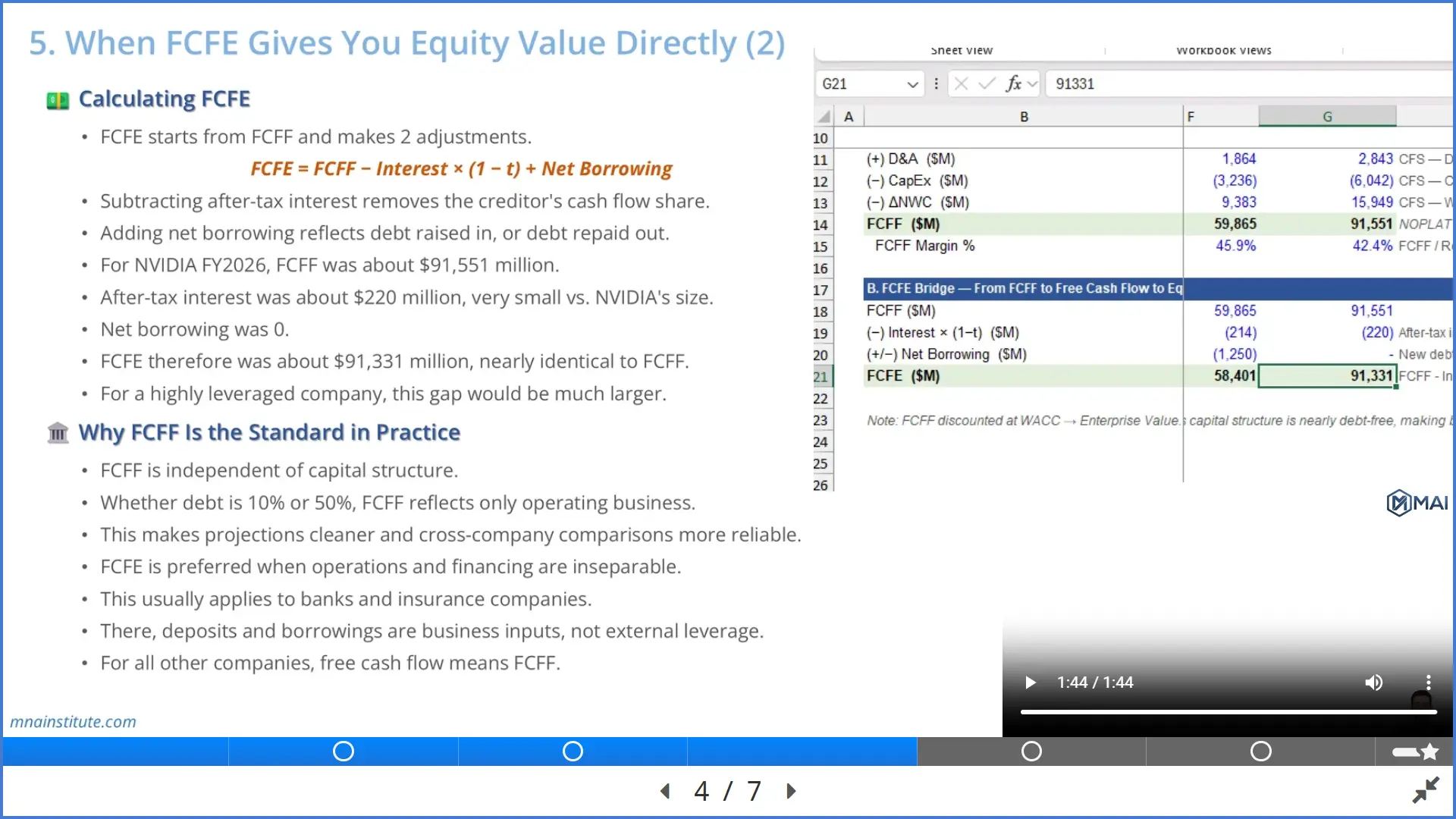

FCFE Calculation Example Using NVIDIA FY2026

The NVIDIA FY2026 example shows why FCFF vs FCFE can be almost identical for a low-debt company.

In this case, FCFF was approximately $91,551 million.

After-tax interest expense was approximately $220 million.

Net borrowing was zero.

The FCFE calculation is therefore straightforward.

FCFE = $91,551 million – $220 million + $0 million

FCFE = approximately $91,331 million

The result is almost identical to FCFF because NVIDIA carried minimal debt relative to the size of its operating cash generation.

For this kind of company, FCFF vs FCFE may not create a large numerical difference in the base year.

That does not make the distinction irrelevant.

It means the capital structure does not materially absorb operating cash flow before it reaches shareholders.

For a heavily leveraged company, the same formula would tell a very different story.

Assume another company also has $91,551 million of FCFF but has after-tax interest of $8,000 million and repays $12,000 million of debt during the year.

Its FCFE would fall to $71,551 million.

The operating cash pool would be the same, but shareholders would receive much less because creditors absorb a larger share.

That is the central practical insight in FCFF vs FCFE.

Capital structure changes the cash flow available to equity even when operating performance does not change.

Why FCFE Gives Equity Value Directly

Free cash flow to equity is already after creditor claims.

That is why discounting FCFE at the cost of equity gives Equity Value directly.

There is no need to calculate Enterprise Value first and then subtract net debt.

The valuation path is direct because the cash flow and the discount rate both belong to the same claimant.

Equity holders receive FCFE, and equity holders require the cost of equity as compensation for risk.

This matching principle is essential in valuation.

A common modeling error is to mix the wrong cash flow with the wrong discount rate.

Discounting FCFE at WACC would understate the equity risk because WACC includes cheaper debt financing.

Discounting FCFF at the cost of equity would overstate the discount rate for a firm-level cash flow because FCFF belongs to both debt and equity providers.

Correct valuation requires consistency.

This is the discipline behind FCFF vs FCFE in every serious cash flow model.

FCFF pairs with WACC and produces Enterprise Value.

FCFE pairs with the cost of equity and produces Equity Value.

The same FCFF vs FCFE logic also explains why FCFE valuation can be attractive for dividend analysis.

Dividends show what management actually paid out.

FCFE shows what the company could potentially pay out to shareholders after reinvestment and financing obligations.

When dividends are much lower than FCFE, the company may be retaining cash for growth, buybacks, debt reduction, or balance sheet flexibility.

When dividends exceed FCFE for an extended period, the payout may depend on cash reserves, new debt, or asset sales.

Why FCFF Is Still the Standard in Practice

FCFE is direct, but FCFF is often more practical for corporate valuation.

The reason is capital structure independence.

FCFF reflects the operating business before financing choices distort the cash flow.

Whether a company uses 10 percent debt or 50 percent debt, FCFF focuses on the cash generated by operations after taxes and reinvestment.

That makes FCFF easier to compare across companies with different financing policies.

It also makes FCFF cleaner when forecasting a company whose leverage may change over time.

If the analyst uses FCFE, the model must forecast not only operating performance but also future borrowing, repayment, interest expense, and equity financing decisions.

That can introduce circularity and unnecessary complexity when the business itself is the main valuation target.

This is why investment banking, corporate finance, and private equity analysis commonly start with FCFF for non-financial companies.

FCFE is preferred in specific cases where financing is deeply connected to the business model.

Banks and insurance companies are the clearest examples.

For financial institutions, deposits, borrowings, regulatory capital, and interest-bearing assets are not merely financing choices.

They are part of the operating model.

In that setting, separating operating cash flow from financing cash flow is less meaningful.

For most industrial, technology, consumer, healthcare, and software companies, FCFF usually provides the cleaner operating valuation base.

That is why this course treats free cash flow as FCFF unless the context specifically requires FCFE.

Common Mistakes When Comparing FCFF vs FCFE

A strong FCFF vs FCFE analysis is not about choosing one formula forever.

It is about matching the cash flow to the question the valuation is asking.

That is why FCFF vs FCFE should be reviewed before building the DCF model rather than after the model is already complete.

The first mistake is assuming FCFE is always better because it gives Equity Value directly.

Direct does not always mean more reliable.

If the company has unstable leverage, volatile interest expense, or large refinancing needs, FCFE can be harder to forecast than FCFF.

The second mistake is treating new borrowing as value creation.

Net borrowing increases FCFE in the period it occurs, but debt also creates future repayment obligations and interest cost.

A higher FCFE figure caused by borrowing should be interpreted differently from higher FCFE caused by stronger operating cash conversion.

The third mistake is ignoring debt repayment.

A company may report strong FCFF but weak free cash flow to equity because it is using cash to deleverage.

That may be good for long-term risk reduction, but it reduces near-term shareholder cash availability.

The fourth mistake is using inconsistent discount rates.

FCFF belongs to all capital providers and should be discounted at WACC.

FCFE belongs to shareholders and should be discounted at the cost of equity.

The fifth mistake is forgetting that FCFE can be negative even when the company is valuable.

A growth company can have negative FCFE because it reinvests heavily or repays debt while still building long-term value.

The analyst must read the reason for the negative number before drawing a conclusion.

A Practical Checklist for Analysts

Analysts should use a simple decision checklist before choosing between FCFF and FCFE.

- Use FCFF when the goal is to value the operating business independent of financing policy.

- Use FCFF when capital structure is changing or difficult to forecast.

- Use FCFF when comparing companies with materially different leverage.

- Use FCFE when valuing equity directly and financing policy is stable.

- Use FCFE when shareholder cash availability, dividends, or buybacks are the analytical focus.

- Use FCFE cautiously when net borrowing is driving the result more than operating cash generation.

- Use FCFE more naturally for financial institutions where financing is part of the operating model.

This FCFF vs FCFE checklist keeps the distinction from becoming a memorized rule.

It turns the choice into an analytical decision based on capital structure, business model, valuation objective, and forecast reliability.

For NVIDIA FY2026, the lesson is clear.

Because debt was minimal, free cash flow to equity was almost the same as FCFF.

For a leveraged acquisition target, the lesson would be different.

The analyst would need to study whether shareholders actually receive cash after debt service, refinancing, and repayment obligations.

That is why FCFE meaning is most useful when it is connected to the capital structure of the company being valued.

A disciplined FCFF vs FCFE comparison protects the analyst from mixing enterprise-level operating cash flow with shareholder-level cash flow and from applying the wrong discount rate to the wrong claim.

Related Courses

The following courses connect naturally to the valuation and cash flow concepts discussed in this article.

- Financial Modeling and Valuation Course with AI and Excel

- Financial Statement Analysis Course with AI for Equity Research

- 3-Statement Financial Modeling Course with AI

- Mergers and Acquisitions Online Course

- M&A Due Diligence Course

- Post Merger Integration Course

Sources

- CFA Institute: Free Cash Flow Valuation

- Investopedia: Free Cash Flow to Equity

- Aswath Damodaran: Earnings, Cash Flows and Free Cash Flows

- NVIDIA: Fiscal 2026 Financial Results